The FED has been raising rates to fight inflation. Unfortunately, that means flirting with a recession. The FED rate increases should slow down the economy, and unfortunately increase unemployment.

So how is it going so far?

(From USA TODAY Feb 14, 2023)

Inflation eased for the seventh straight month in January, helped by lower costs for used vehicles and offering some relief to consumers struggling with high prices over the past year.

Consumer price index data released on Tuesday showed that prices for a range of goods and services rose by 6.4% over the past 12 months, down slightly from an annual rate of 6.5% in December and a 40-year high of 9.1% in June.

On a month-by-month basis, however, prices increased by 0.5% in January compared with a slower gain of 0.1% in December. The acceleration was driven by shelter costs.

Americans have been struggling with soaring prices since last year, resulting in a decline in the real value of their income despite historic wage increases. High inflation has also amplified the risk of a recession.

Everyone has been looking for the bad news, layoffs and unemployment.

The news for the January jobs report:

The U.S. added an astonishing 517,000 jobs in January, according to new data from the Labor Department.

Economists had been expecting a gain of roughly 185,000 jobs in January.

What about the unemployment rate?: It dipped to 3.4 percent. Economists had predicted an unemployment rate of around 3.6 percent. This is the lowest in 54 years.

The economy is much stronger than many had estimated.

However, the gloomy interest rate forecast has definitely affected the real estate market.

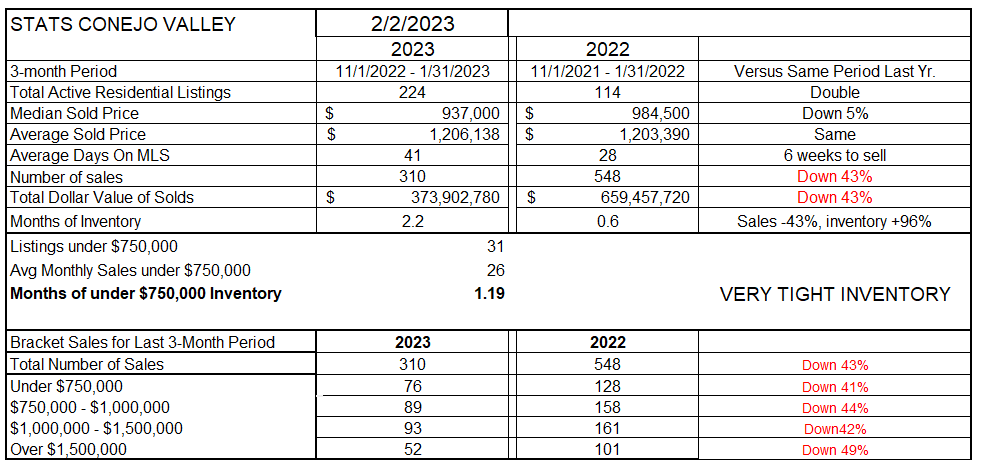

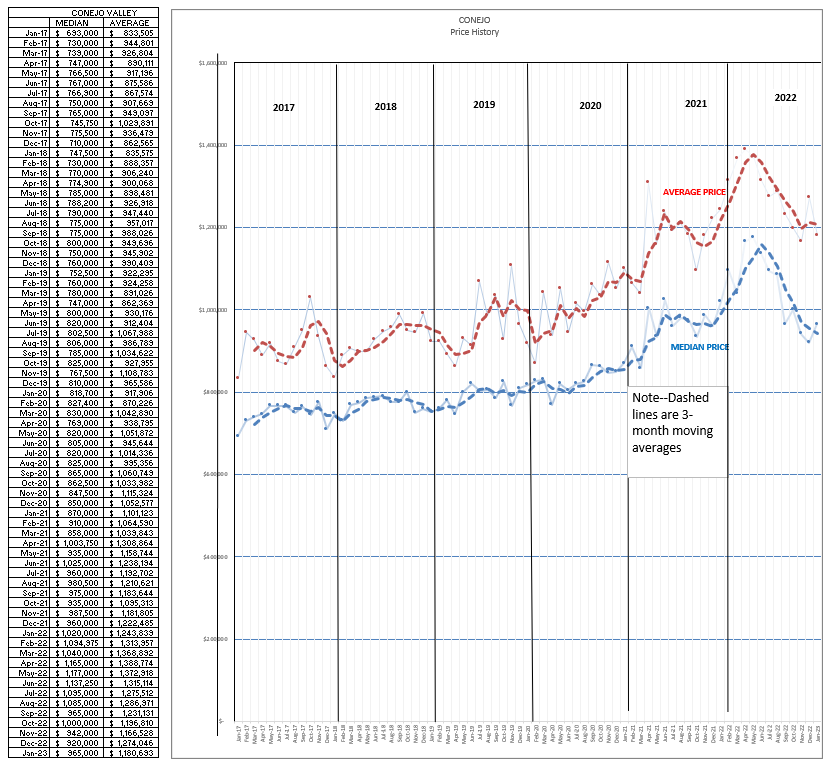

Let’s begin with the statistics table, reminding you that these figures are for three months of history, the most recent three months compared to those same three months last year.

In the Conejo valley, prices are down compared to last year. The median is down 5%, while the average is the same. However, when you look at the price chart later in this blog, remember that prices last year at this time were increasing, whereas prices this year are decreasing. That opposing effect will be prevalent for the next 4-5 months.

The inventory is double what it was last year, and it now takes 6 weeks to sell a home versus 4 weeks last year.

Prices are not crashing, but the level of business has significantly decreased, down 43%. We are only selling about half the number of homes in the last three months compared to the same three months last year. The inventory represents 2.2 months worth of sales at this level.

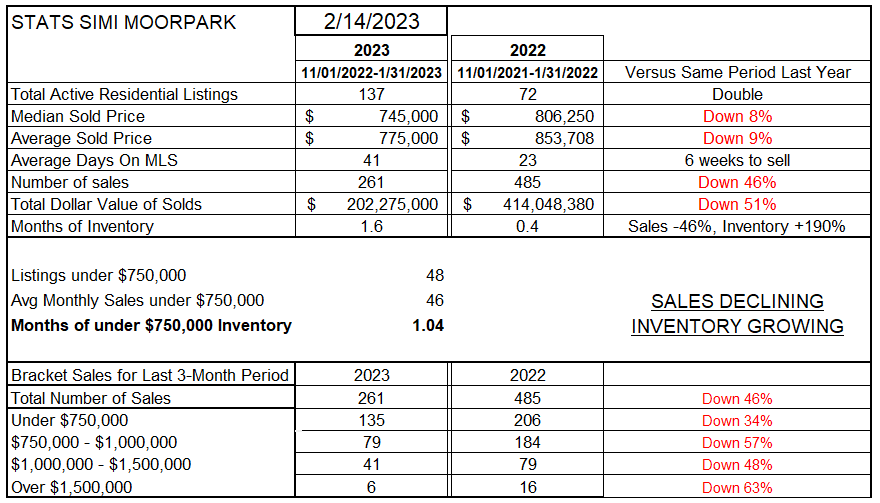

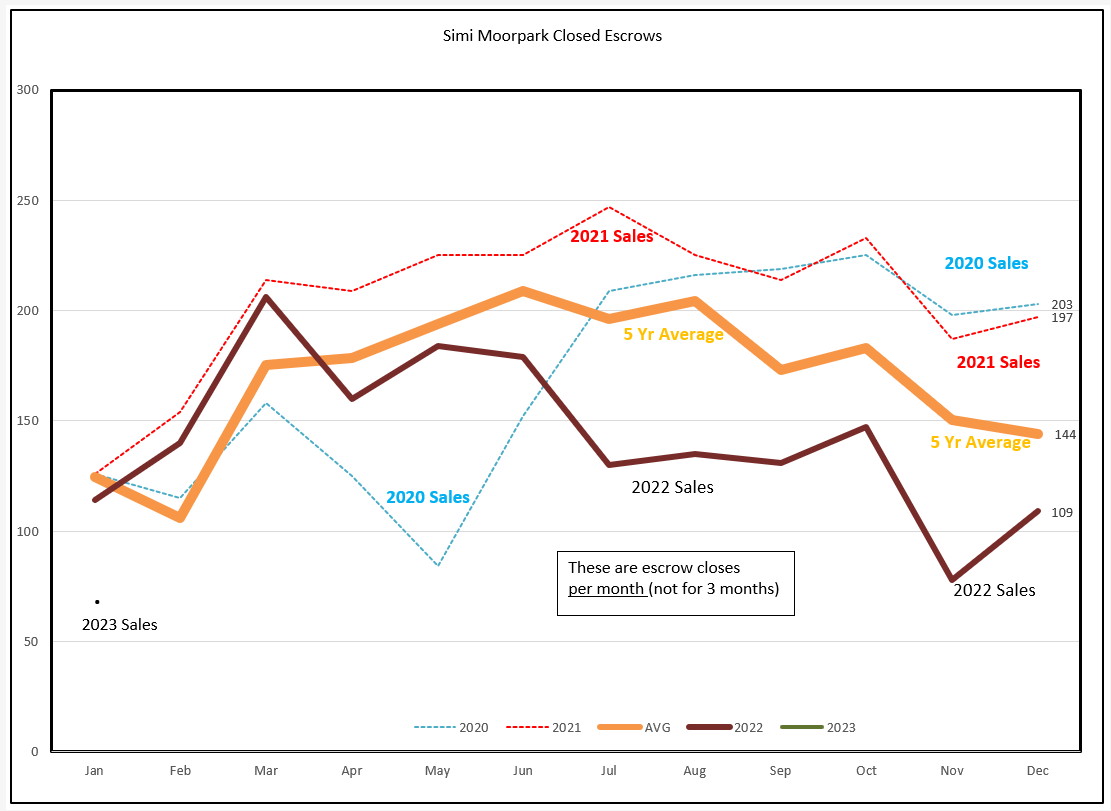

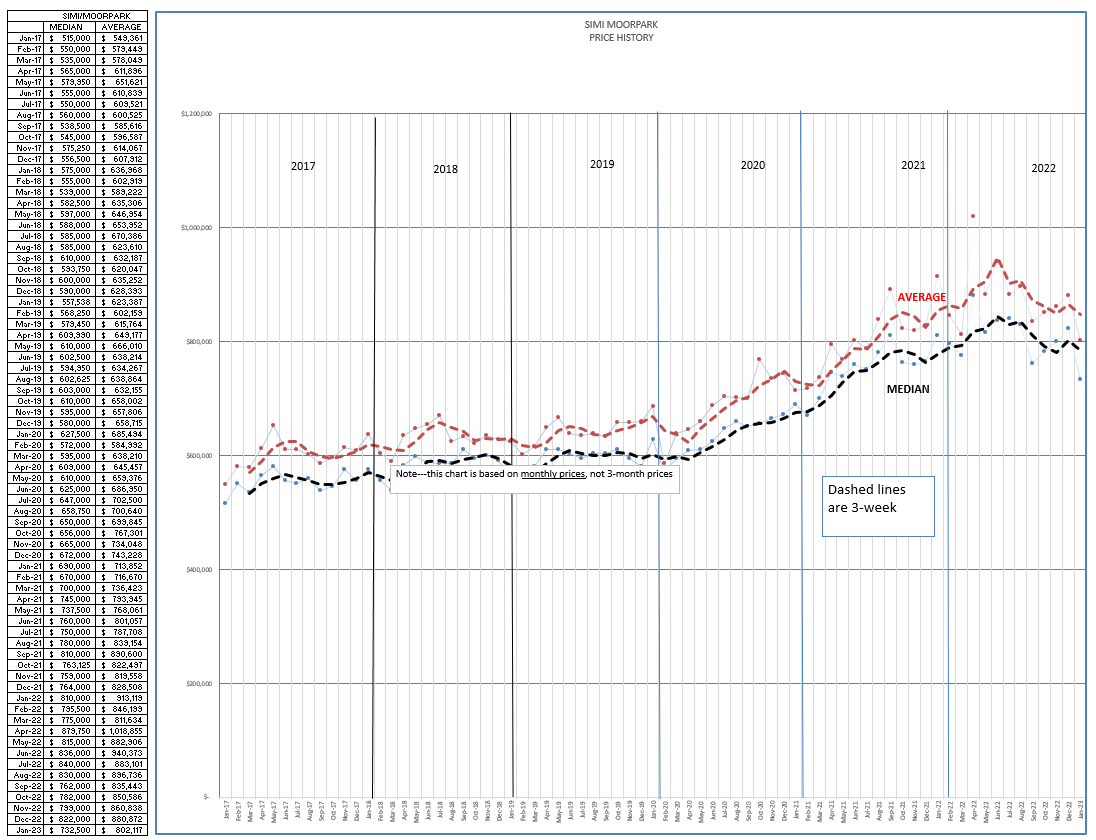

Those are the numbers for the Conejo valley. Let’s see how they compare to Simi Valley and Moorpark.

The inventory has also doubled. Both Median and Average prices have decreased, by 8-9%. It now takes 6 weeks to sell a home versus 3 weeks last year.

Perhaps the most important statistic is that the level of business has significantly decreased, down about 50%. We are only selling half the number of homes in the last three months compared to the same three months last year. The inventory represents 1.6 months worth of sales at this level.

Let’s next look at the inventory graph. The starting inventory for the year was lower in 2021 and 2022. The 2023 beginning inventory level, although double last year’s start, remains considerably below a normal year (between 300 and 400 active listings). We are not selling as many homes, but not that many homes are coming onto the market, keeping the inventory reasonably low. The biggest increase is in homes priced above $1.5 million.

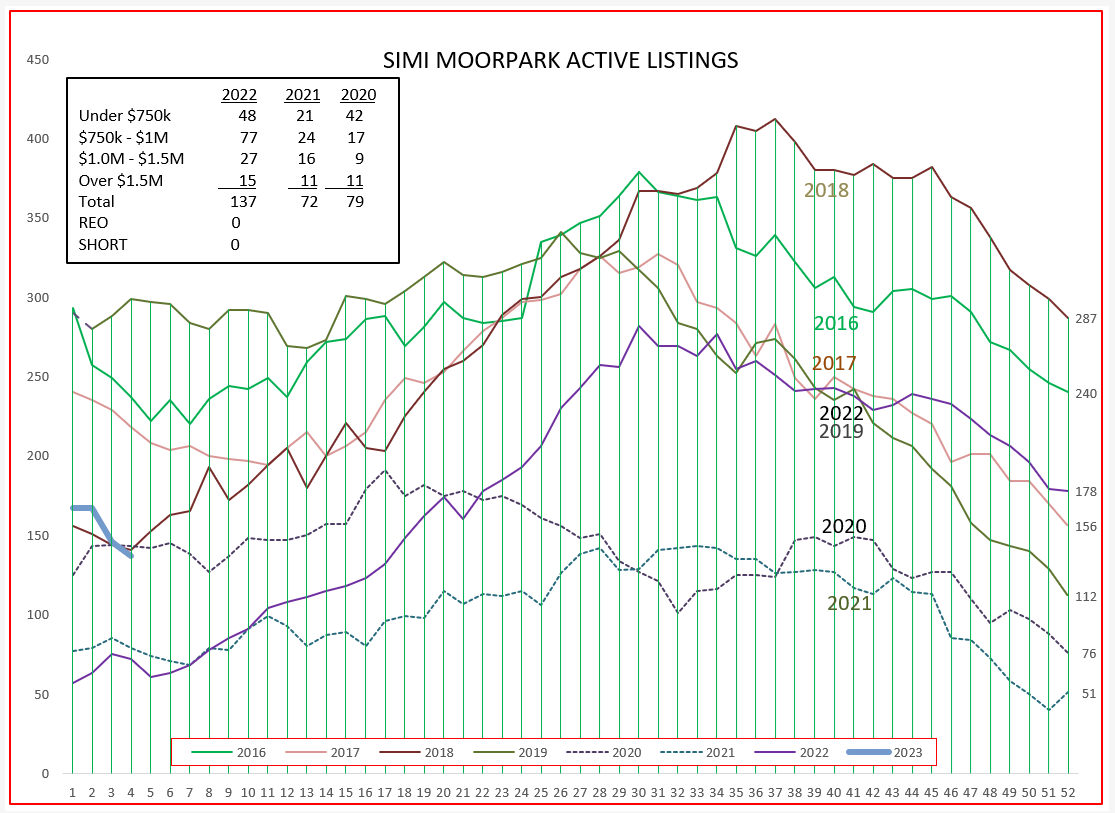

For Simi/Moorpark, the beginning inventory was also double the 2020 and 2021 beginning, but it seems to be shrinking, not growing.

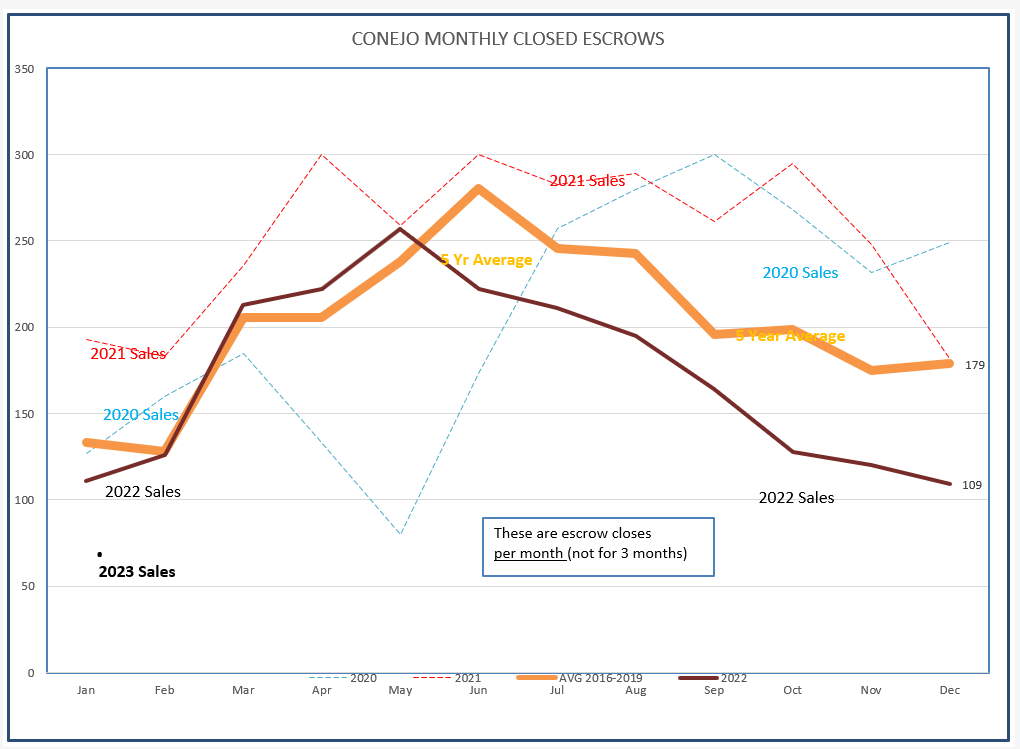

Let’s now look at closed sales. Remember, closed sales represent contracts that were written two months ago. Conejo sales began the year much lower than the preceding years.

For Simi/Moorpark, the same is true. Lots of upside potential, but for now a very quiet market.

How has all this affected prices? (Or how are prices affecting both inventory and sales?) Prices fell abruptly from midyear last year, but frankly look as they are now stabilizing. Remember, if you compare early 2022 (where prices were rising) and 2023, prices will look as if they are dropping because in 2022 prices were increasing. So even though prices in 2023 are stabilizing, if you compare them to 2022 you will be misled by the strongly increasing 2022 market.

For Simi/Moorpark, much the same comparison. Prices in 2023 are stabilizing, while prices in 2022 were strongly increasing.

So what do I make of all this? At Dilbeck’s business meeting last week, VP Merilee Iverson asked how the market seems to be doing. Our agents reported that there is a healthy quantity of buyers searching for available homes, open houses are attracting very large numbers of buyers and their agents, and multiple offers continue to be the standard for well-sought-after properties. And although the FED is increasing rates, mortgage rates are on the decline.

Immovable force meets unstoppable object. Market strength meets high mortgage rates. Fed increases meet strongest labor market ever.

Anybody out there think they know what is going to happen? Please let me know. Covid should have killed this market three years ago. The market refuses to lay down and die.

Chuck