2023 was a difficult year for many. My family had some serious health issues to deal with, the economy had to deal with runaway inflation and explosive interest rate growth, the housing market was good for homeowners (prices are up) but bad for agents (number of sales down). I have heard from many “I am glad to see 2023 come to an end”.

Let’s review 2023 and see how we should look forward to 2024.

The study of economics is interesting, particularly if, like me, you are a lover of numbers and graphs. Supply and Demand should be a two-dimensional graph, but the resulting component of Price makes it a challenge to draw. Particularly in California, we have another major factor to consider, at least as important as Supply and Demand and Price. The Government. It brings our graph into the multi-dimensional game of chess played on the Starship Enterprise. Hard to picture.

In past years, the FED bought up huge quantities of mortgage-backed securities to keep mortgage rates down. Then they started selling off those same securities while they were generally raising interest rates, regularly and constantly. California has tried to exacerbate the shortage of homes (2.5 million units) by requiring RHNA numbers of homes to be planned for, and pushed local governments to accept ADUs and even taking some cities to court. A combination of local and state requirements resulted in Impact Fees that approach six figures per unit. Yes, the government has been a major factor, both good and bad.

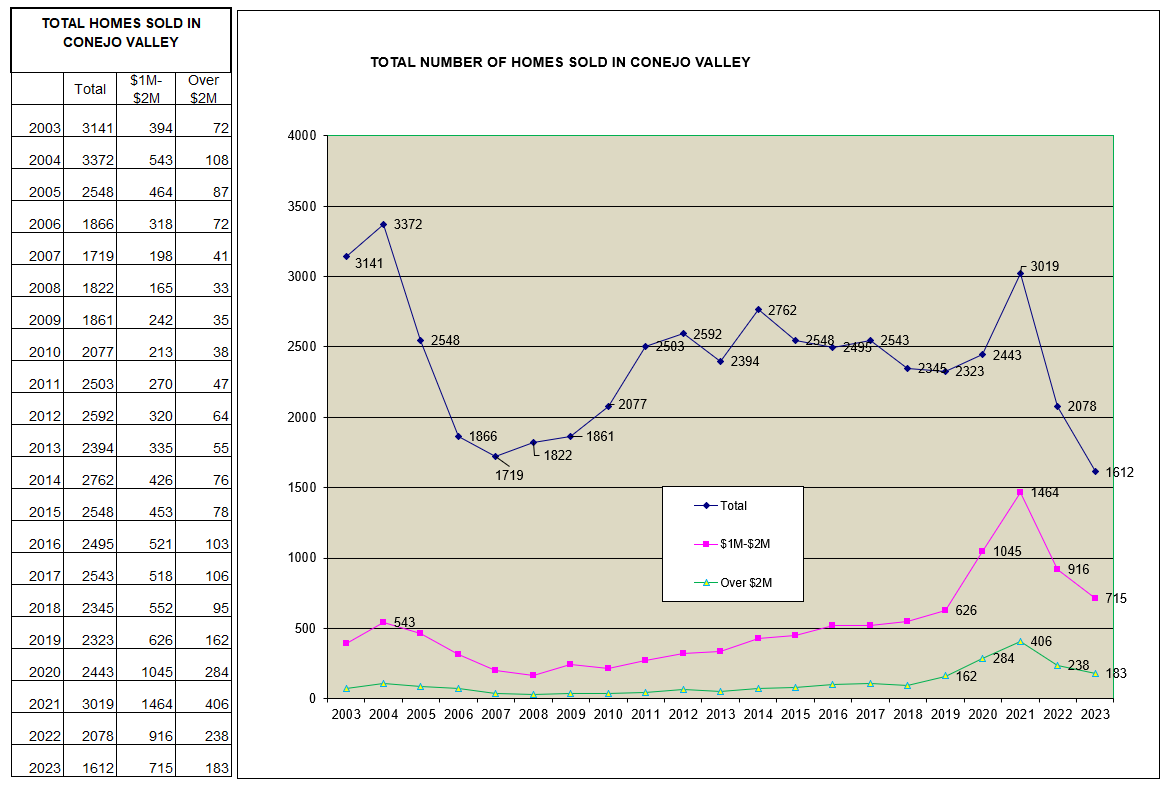

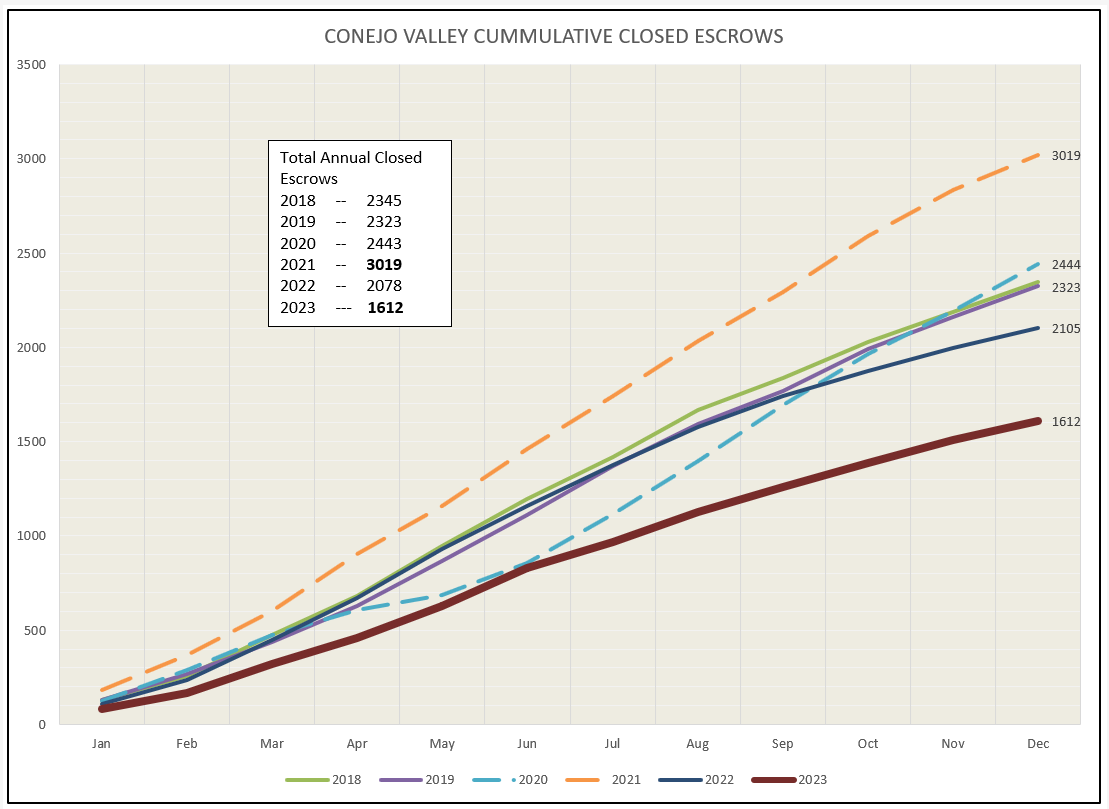

One of my favorite phrases is “All Real Estate Is Local”. Let’s see how our local market has done now that 2023 has ended. Let’s start with a chart of how the real estate market has performed as measured by the number of units sold. In the chart below, the top blue line represents the total number of units sold. It was a surprise, when looking back all the way to 2003 (when I started in Real Estate) that the number of units sold this year is the lowest since 2003, lower even than the 2007-2009 Great Recession. (I began keeping records in 2003)

The expected yearly average we would expect from this chart is in the neighborhood of 2400 units per year. The years 2003-2004 saw record sales due to mortgages available with stated earnings and teaser rates for the first five years. The shakeout resulted in what we now call The Great Recession. The predominant sellers became the banks, who became homeowners after foreclosures. By 2012 the banks switched to short sales, bringing the market back towards balance. The phenominal year of 2021, the Covid home-buying panic, was 3,019, close to a record high. Two yeares later, 2023 recorded only half of that number. These past few years have indeed been a roller coaster.

Price increases must also be taken into account. The two lines at the bottom of this chart shows the growth of homes priced between $1-2 million and those over $2 million. Similar to the total of homes sold, the number of homes in these tranches peaked quickly and then dipped precipitously.

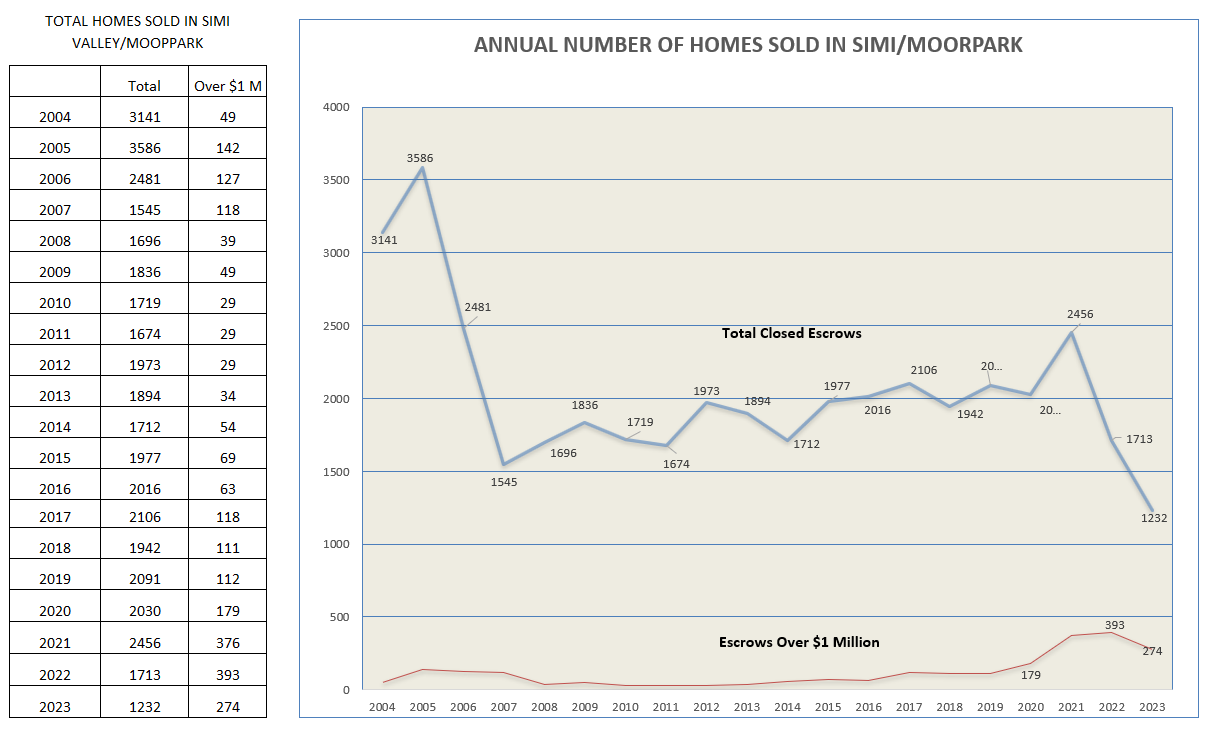

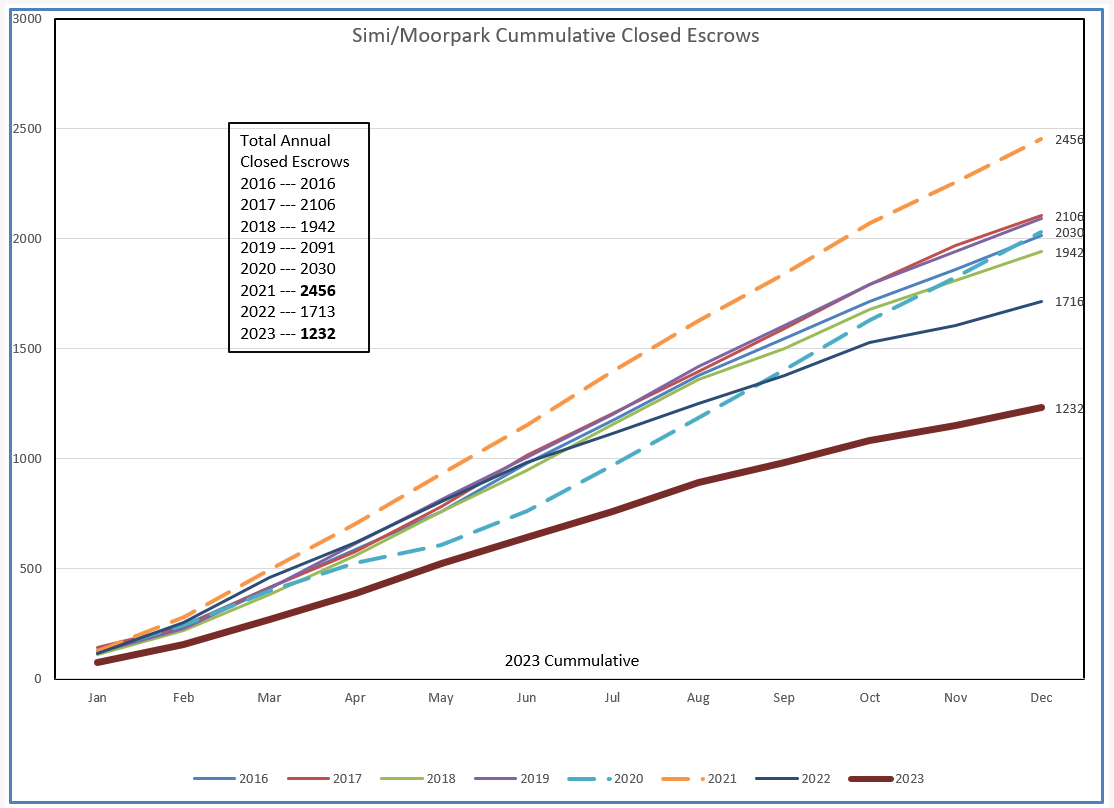

Looking at Simi Valley and Moorpark, we see much the same history. The 2003-2004 surge resulted in Simi/Moorpark exceeding the number of homes sold in the Conejo, and the resulting few years saw an even steeper drop in sales. The average during the years following this big drop is in the neighborhood of 2,000 units per year. The phenominal year of 2021, the Covid home-buying surge, was 2,456 units. This year 2023 ended at roughly half of that number, 1,232. These past few years have indeed been a roller coaster.

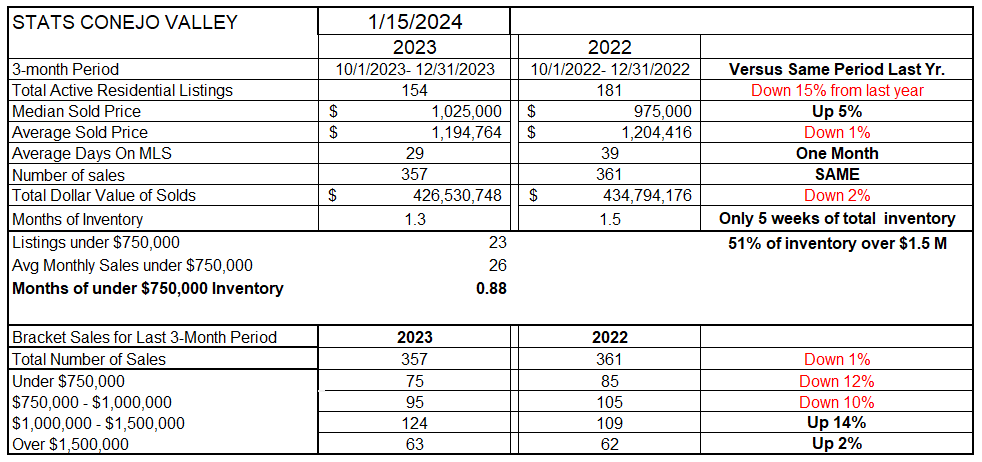

Let’s next look at the statistics in a shorter time frame, the last three months compared to those same months last year. Median prices increased by 5%, but the Average price actually decreased, mainly due to the influence of the very top end of the market. We will discuss inventory at length, but note that half of our minimal inventory is currently made up of homes priced in the highest tier of prices (over $1.5 million). The very bottom of this table indicates that higher priced homes are showing some strength, particularly since the median price in the Conejo has now exceeded $1 million.

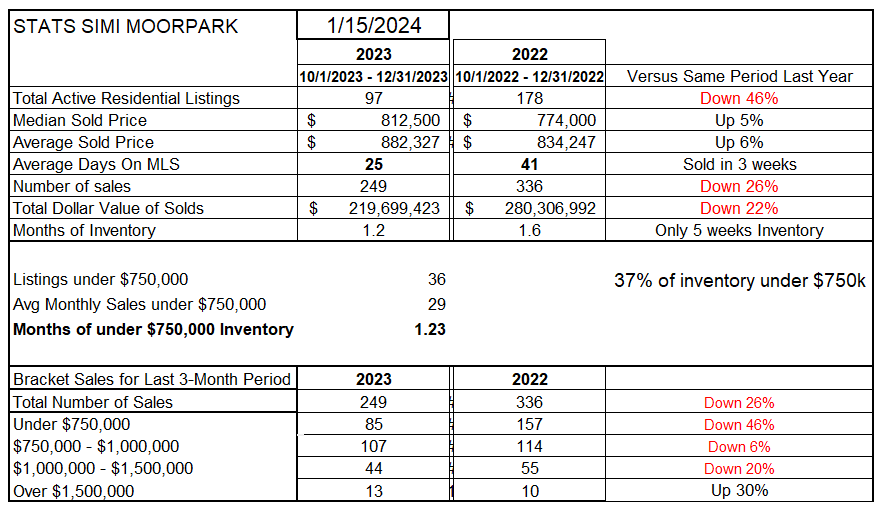

For Simi/Moorpark, there is a smaller percentage of higher priced homes. This table shows prices currently are 5-6% higher than they were a year ago. 37% of the active inventory is priced below $750,000. Total inventory is down 46% from a year ago and in single digits as the year ends. The lack of inventory resulted in 26% fewer homes being sold during this three month comparison with last year. But that may be an improvement when you consider the annualized figures in the top two charts above. The bottom of this table shows a huge percentage jump for homes priced over $1.5 million, but this is a very small sample and is the result of only 3 additional sales.

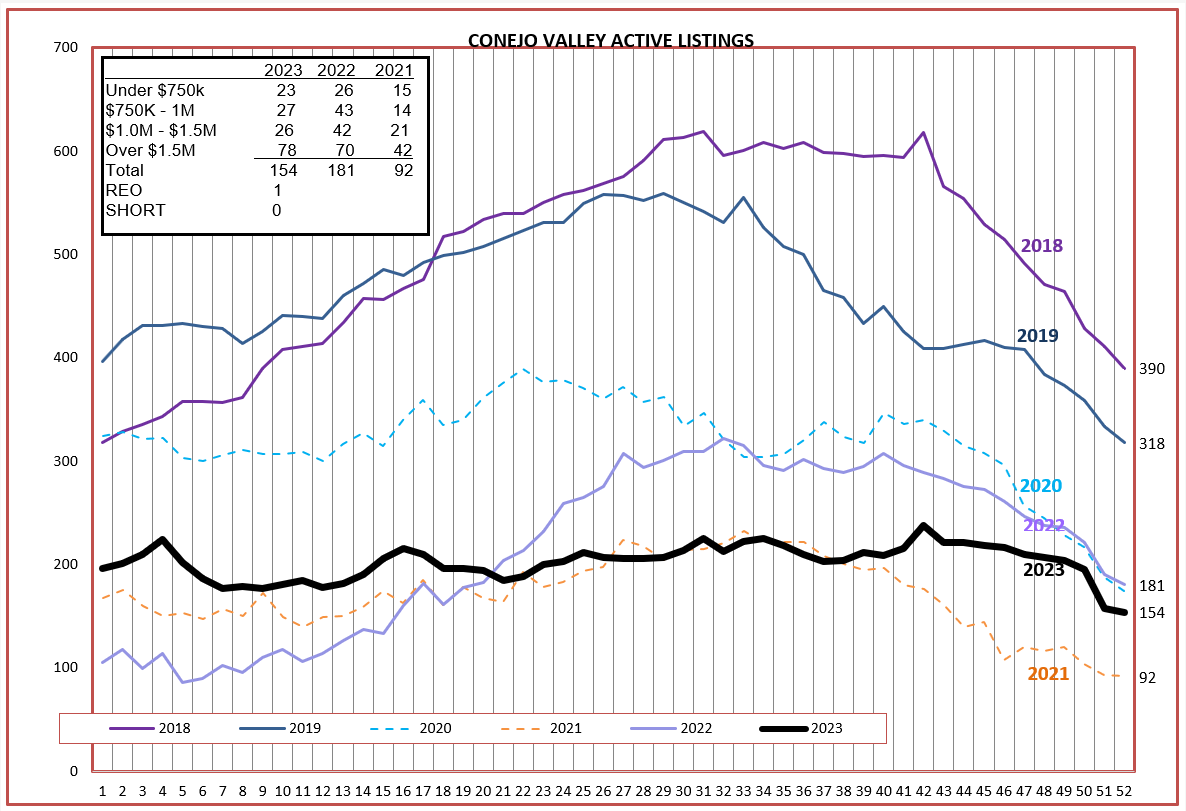

We know inventory is a major constraint facing our market. Our inventory gradually grows as the year progresses, peaking in the summer and then dipping toward year end. Obviously 2023 did not follow that usual pattern, ending up as basically a flat line as the year progressed. Any homes coming onto the market were immediately sold, resulting in this flat line. A lack of inventory generally provides upward price pressure .

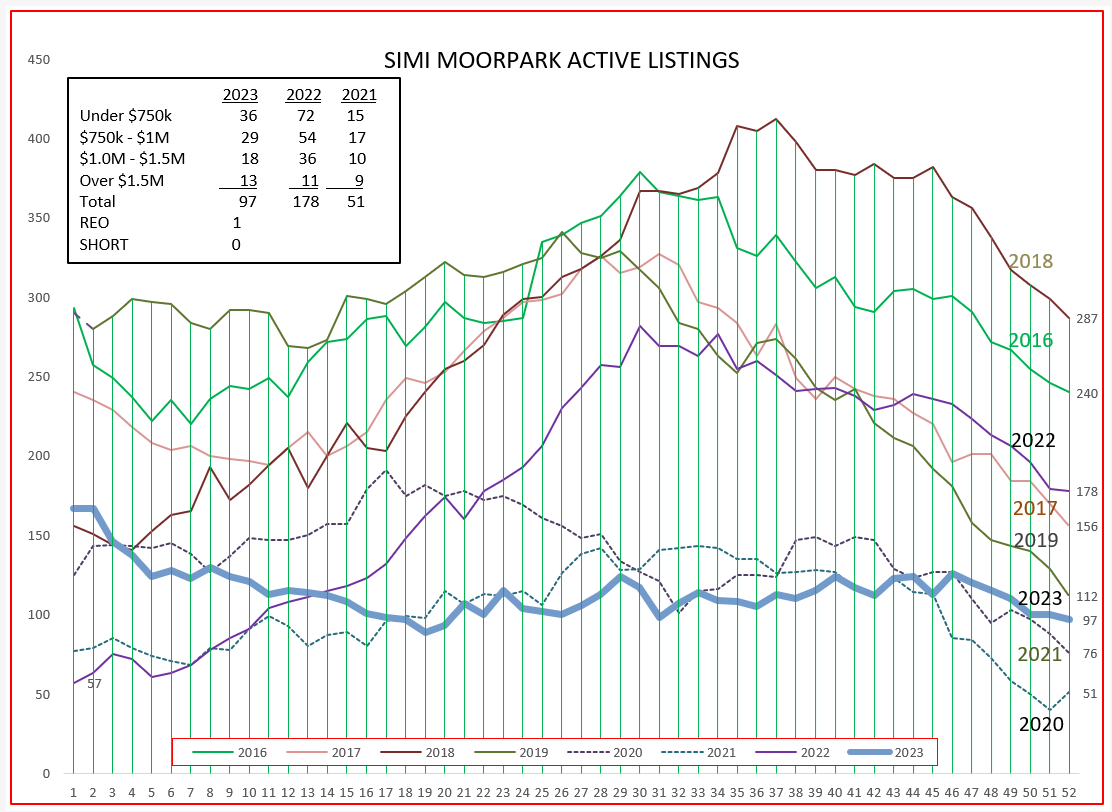

Simi/Moorpark experienced the same pressures, only worse. The years 2019 – 2023 all ended with around 100 units available, a terribly low inventory. 2020 ended with only 51 units. The dotted lines represent the anomaly Covid-years. For a non-Covid year, the 2023 flat-line means that the inventory never grew as the year progressed, indicating again that whatever hit the market sold, under rising price pressure.

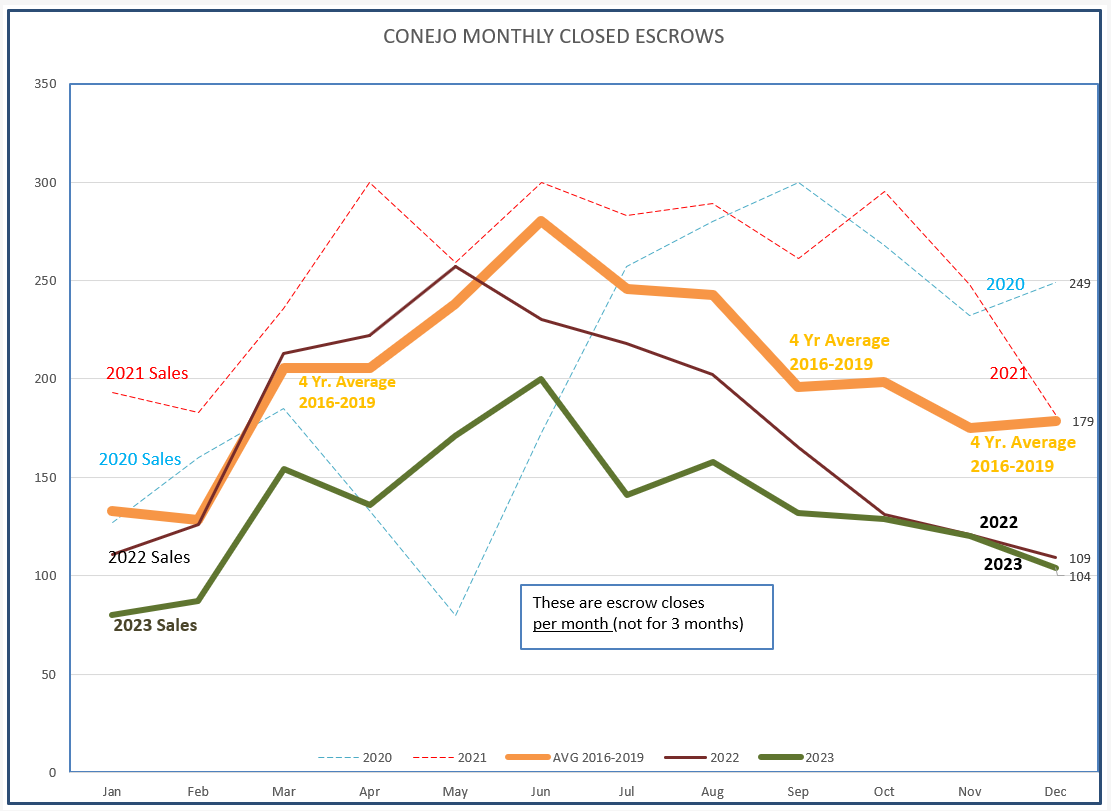

This is how sales progressed as the year progressed. 2023 showed a normal pattern of sales, rising as the year begins and dropping off as the year ended. Buyers were out buying, resulting in this normal curve, although with much lower numbers because there was not enough inventory to sell. Compare the normal average (orange line) to the 2023 (heavy green) line, and you can see the similarity.

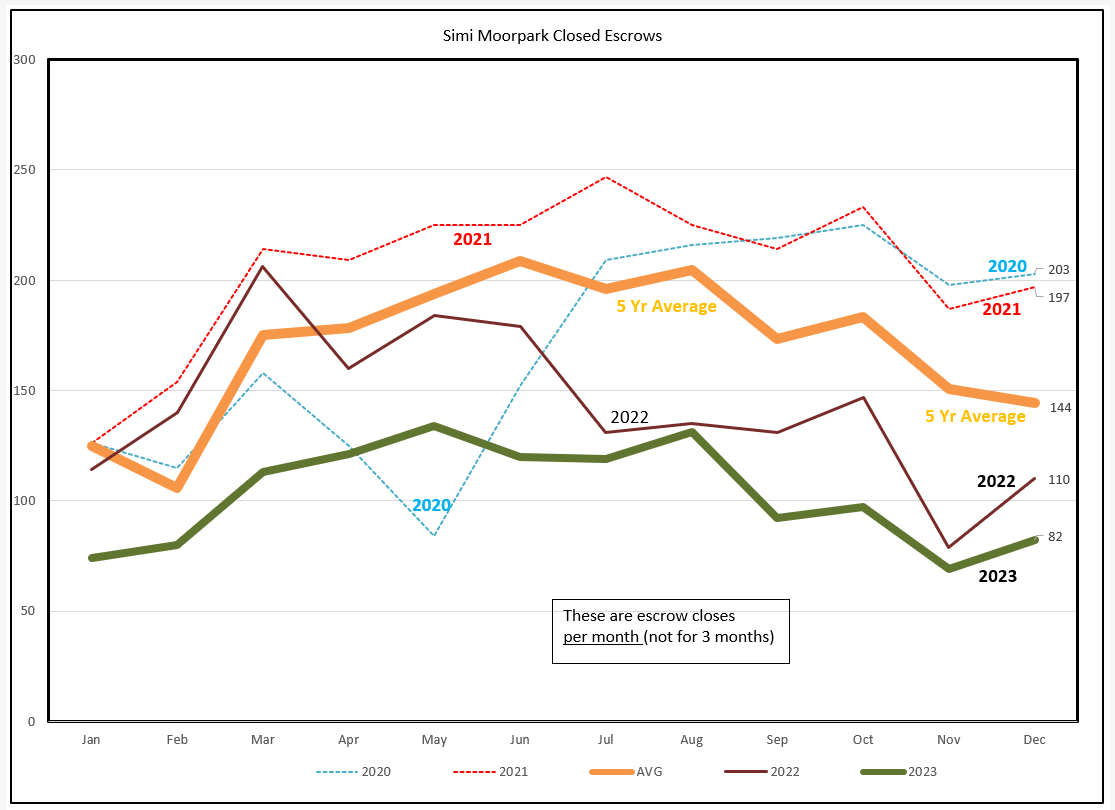

Simi/Moorpark expressed the same picture between the normal, average sales (orange line) and 2023 (heavy green line.) The green line is shaped normally but lower, again due to a lack of inventory.

That sales progressed normally as the year progressed can be seen in this chart. In this chart, each point represents the total sales as the year progresses. Notice that in the inserted box, the 2021 total homes sold was 3,019, while the 2023 total was only 1,612. We can call 2023 a correction year, due to the abnormally high total in 2021.

SImi/Moorpark progressed the same way. Note in the box insert, the year 2021 was the highest in recent history, and the year 2023 ended up only half as many homes sold.

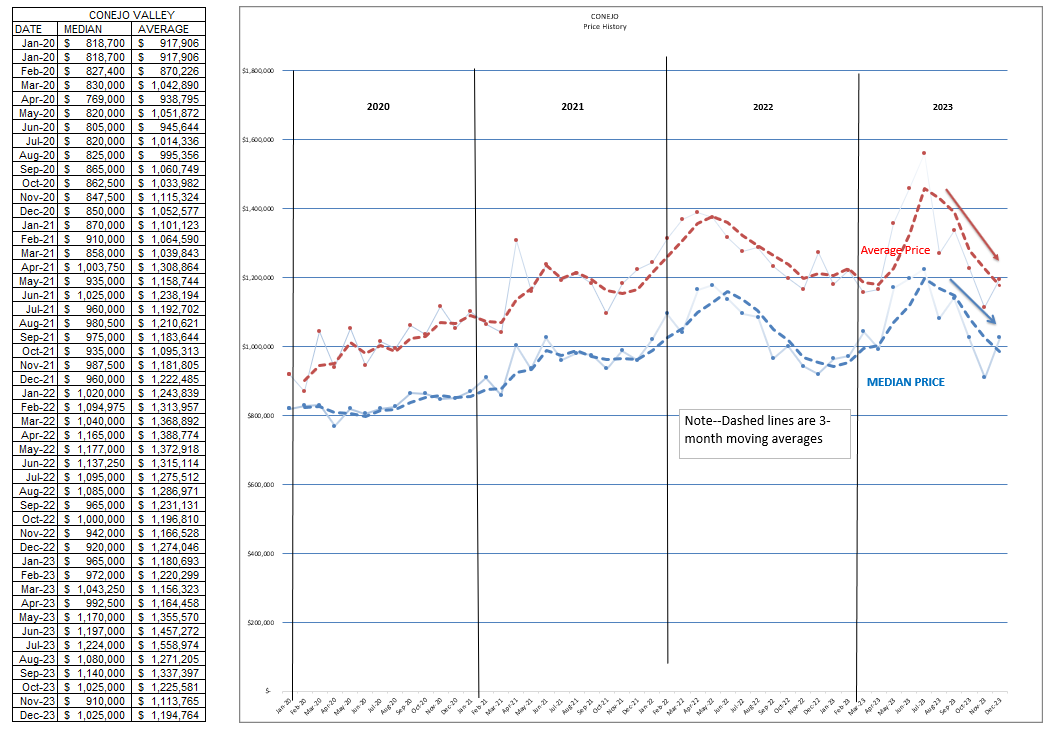

Finally, let’s look at what prices have been doing. Conejo prices rocketed as the year began, and then dipped as the reality of higher mortgage rates convinced buyers to pull back. As fewer buyers were able to afford to buy, both Median and Average prices dropped.

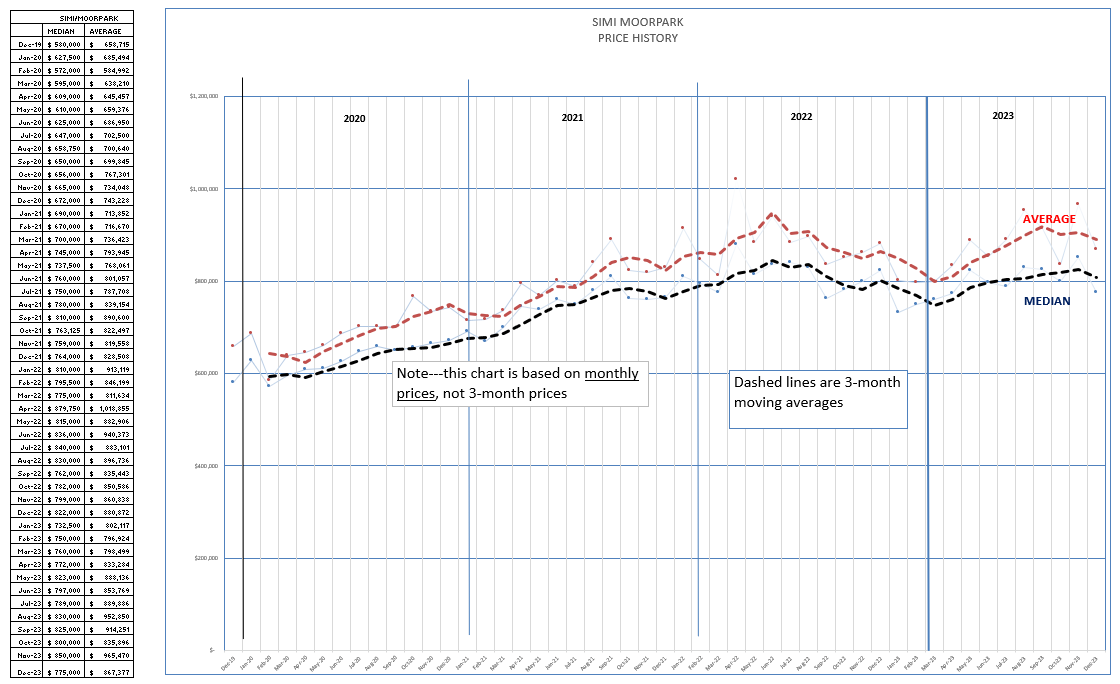

For Simi/Moorpark, the decrease was also felt, but since prices did not rise as much as Conejo, they did not fall as much as Conejo.

A final word on why I report on Simi Valley and Moorpark together. It is personal. I live in the Conejo, but our association includes both Moorpark and Simi Valley. Moorpark is the smallest in area and in number of homes, so way back in 2003 I bundled those two together, and have continued that decision until today.

What is my New Years resolution?

Maybe more interesting, what is my New Years Forecast?

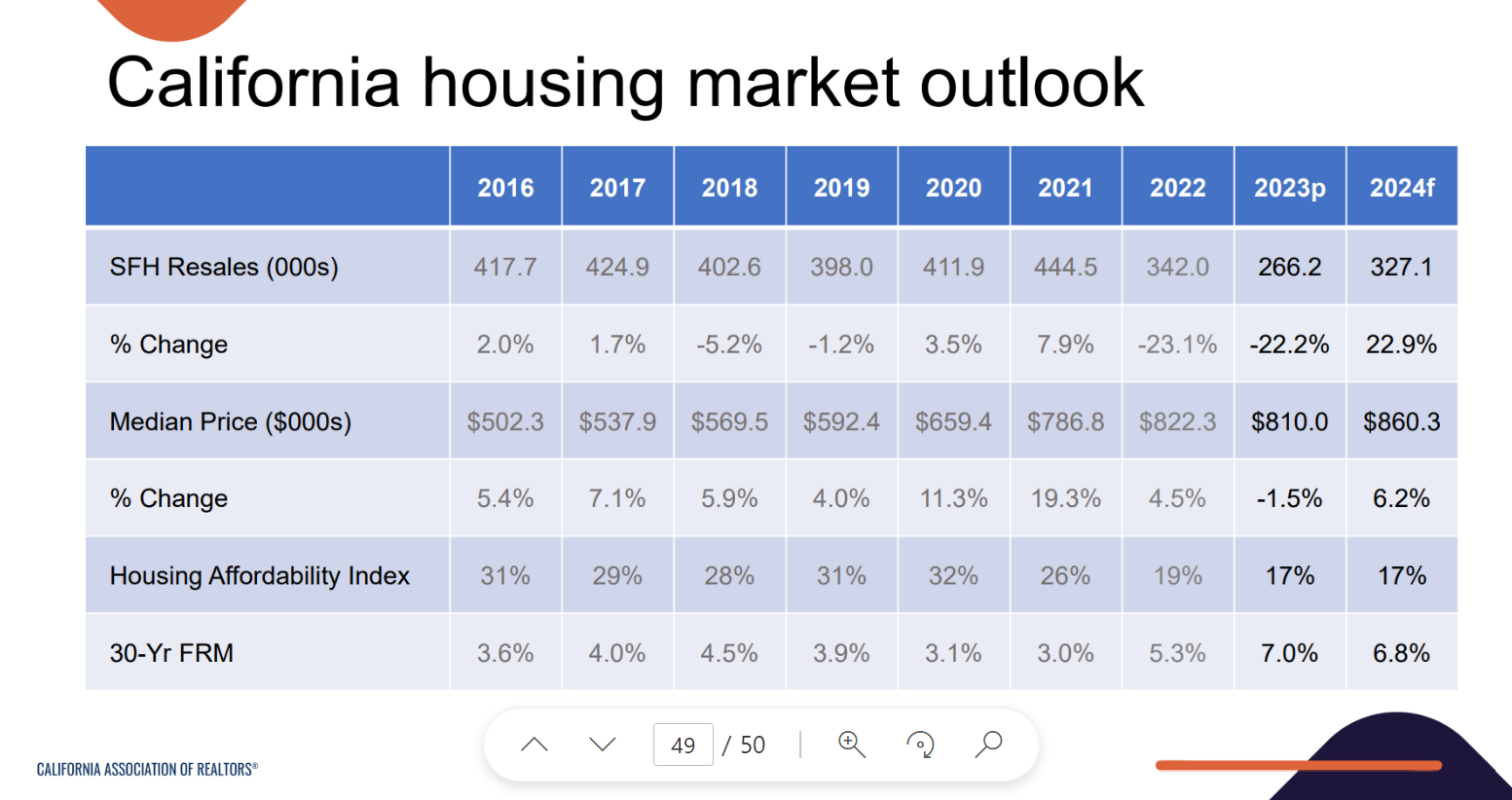

This blog is a little late because I was fortunate to be able to attend the Center for California Real Estate meeting last week, featuring four of our most respected real estate economists. Their opinions are much better than I could ever opine, as is the C.A.R. forecast done by Jordan Levine and Oscar Wei. These four economists all agreed with the forecast issued by C.A.R., and with their permission I have reproduced it below. Better that you quote these highly respected economists than me.

2024 sales units should increase 23% compared to 2023. Although that is a large percentage number, the actual number of sales remains low at 327,000 units, still below the normal average sales total of 400,000.

Median prices will continue to climb, up 6%. Why? Lack of inventory. But that will not help housing affordability, at a very low 17%.

What could change this? Mortgage rates, which in this forecast is said to be 6.8% on average for 2024. Many have been forecasting FED declines in their interest rates, but the current expression describing rates is “remaining higher for longer”.

We could use some help from Washington. If they were to change the SALT tax, reduce the long term gain on the sale of a home, and reduce mortgage interest rates, the market could change appreciably for the better. Santa, I know you are back at the North Pole, but that is what we want.

The end result is to look for the market to improve, but that may occur by the second half of this year.

Happy New Year.

Chuck