There are many ways to tell when things slow down.

On a plane, you feel your body move forward in your seat. In a car, the same thing happens, but you can look at the speedometer to accurately measure the slowing.

In the real estate marketplace, you can look at three “speedometers”. The inventory begins to climb. Sales volume slows down. And prices reflect the change both by either declining or slowing their annual increase.

Let’s see if any of those things are happening.

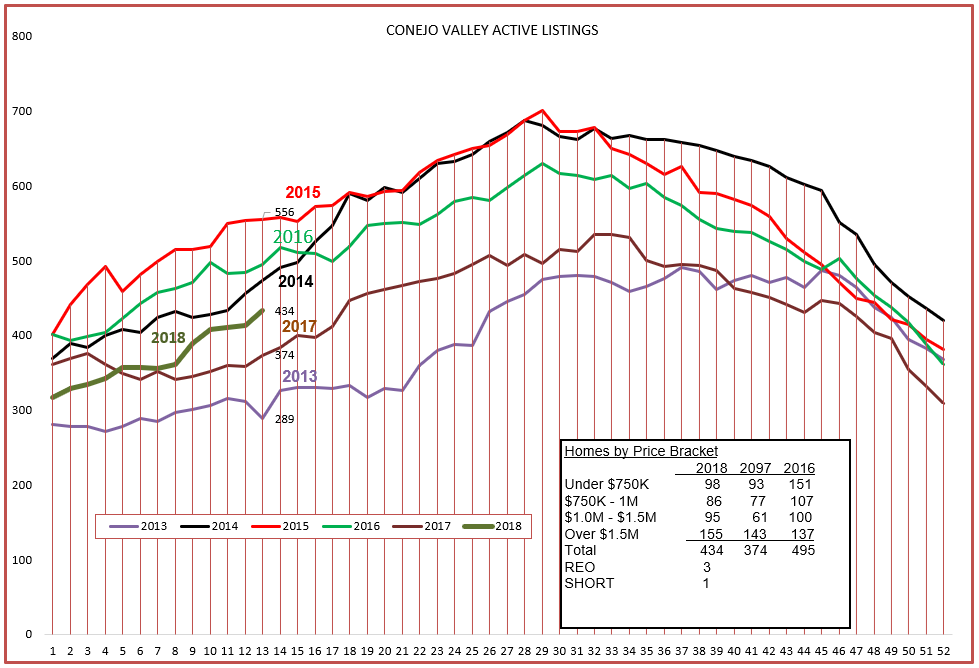

First, the inventory. The inventory always climbs at this time of year, and this year is no exception. This year the increase is strong, stronger than 2017.

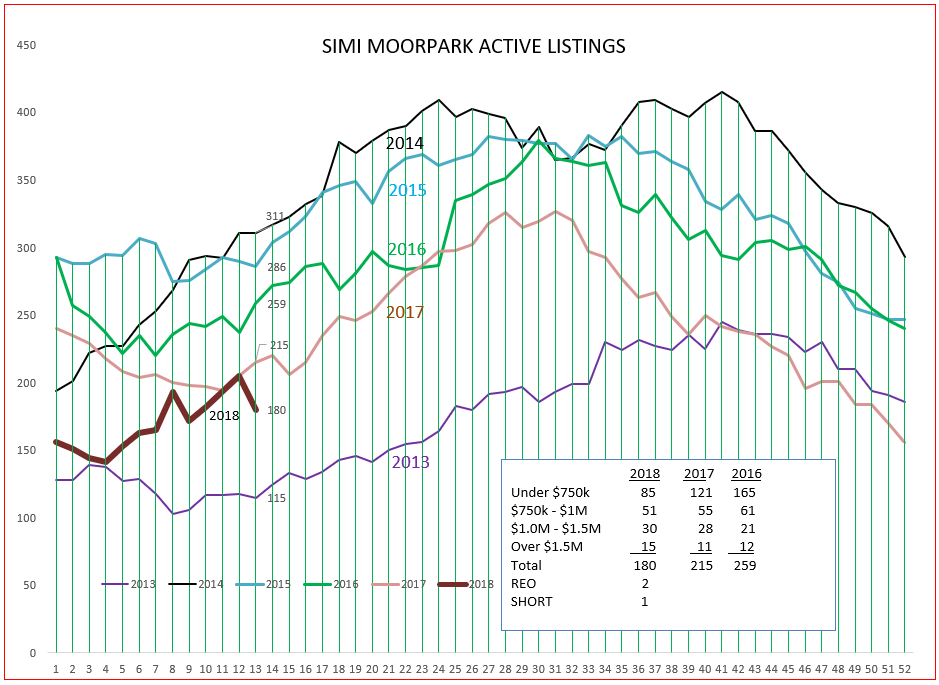

For Simi Valley and Moorpark, it can’t seem to make up its mind. The inventory in Simi/Moorpark remains extremely low, so any changes make a big difference.

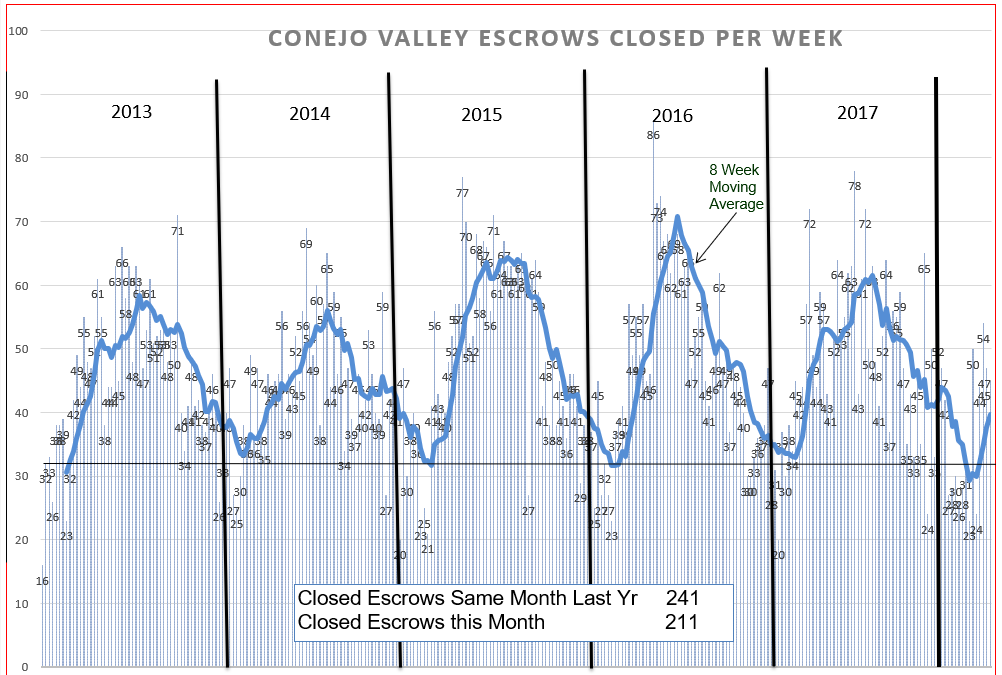

Inventory growth is only one part of the equation. It is like getting a sports score of “Dodgers 6”. We need to know what is going on with “the other side”. With the real estate market, the other side is the number of sales taking place. Sales in the Conejo began the year low (look at all the white space below the 8-week moving average line). The sales level dropped below 30 sales per week, lower than the past five years. But, as happens this time of the year, sales are bouncing back, strongly.

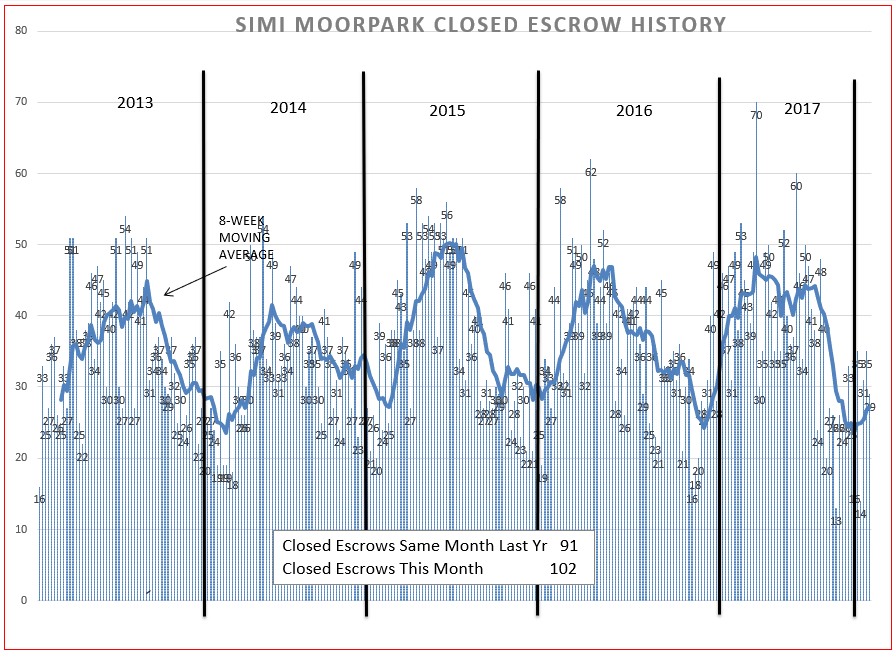

For Simi/Moorpark, sales in the recent few months of 2017 remained at a very high level, but then dropped precipitously for the last two months of the year. 2017 was a very strong sales year for Simi/Moorpark. It might have been even stronger if there was more inventory available to sell. If that is true, this year may be worse, since the inventory at this point is 16% lower than the inventory in 2017.

Let’s continue on to the last charts before we go to the numbers. The numbers give us a better view of what is occurring at this moment, but they usually lack the historical perspective that we can see in the charts.

First, average and median prices in the Conejo Valley. Lots of ups and downs for the Average Price, much smoother for the Median Price. The difference, represented by the change in spacing between the two lines, is the quantity of high priced homes being sold. The more space, the more high priced homes being sold. Both lines show a leveling of prices, also usual as we go into the end of a year, but usually increasing at this time of the year. Prices are not climbing. Remember, the dash line represents the average of the previous 4 points, thereby smoothing out the information.

The same for Simi Moorpark. Properties here predominantly in the $550,000 to $650,000 range, and are not as affected by the fewer number of high priced properties. However, the price lines are both reasonably flat. A very low inventory usually leads to price appreciation. The lid seems to be on this pot.

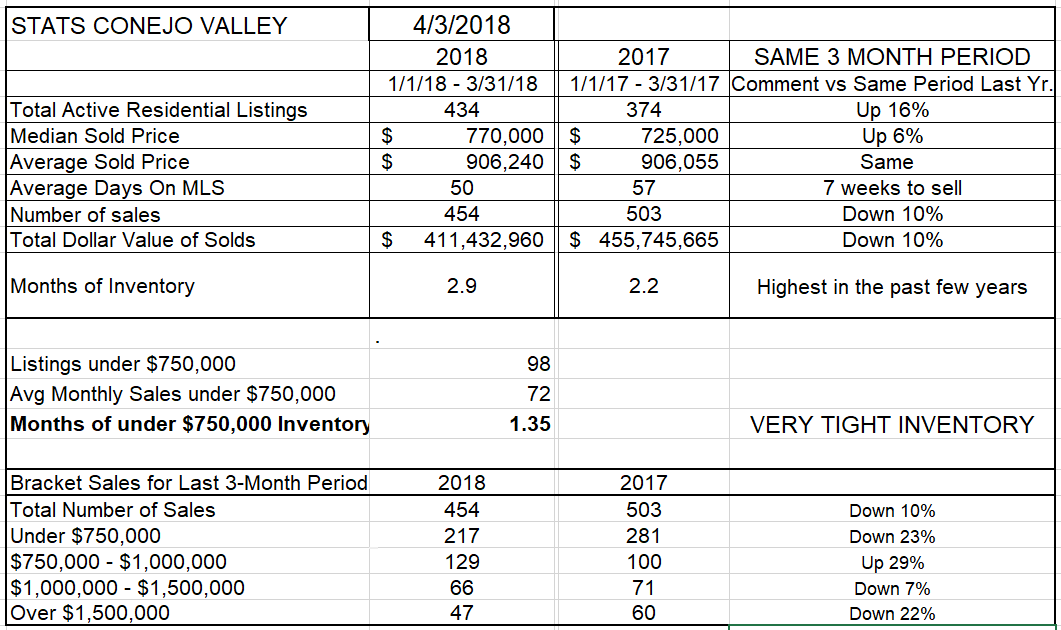

Finally, let’s take a look at the actual numbers. As you read through these, remember to check back on the charts above, as they display the trends. First, the Conejo Valley.

Inventories have increased, on a very low base last year. The inventory today is 16% higher than it was on this day last year.

The number of sales for the first three months of this year, compared to the first three months of last year, is down 10%. Previously we explained that the lack of sales was due to the lack of available inventory. With inventory climbing and sales figures dropping, that no longer appears to be a valid conclusion.

Median prices are up 6% versus the same time last year, while Average prices are the same. This is consistent with the chart above, showing the narrowing of the Average and Median price differential. A lower number of higher priced homes is the reason for the difference.

Are prices lower for all homes in all areas? No. ALL REAL ESTATE IS LOCAL. There are areas that are slower, areas that sales are red hot, areas where prices have slipped, areas where prices are strong. This is where a competent real estate agent needs to research and give someone specific information. The information displayed here represents averages, as does the state CAR information and just like the country-wide NAR information. But our smaller areas make our statistics more important to us, and to our clients. And more useful.

In Conejo, the number of sales is down 10% for the first three months of 2018 as compared to the first three months of 2017. 10% is a lot, and is displayed by that white space under the 8-week-average line in the closed escrows chart. According to the chart, things are picking up, an indication that this temporary decrease is over and sales activity is getting healthier.

Finally, the most important figure in this chart is Months of Inventory, which compares the number of sales to the amount of inventory. This number has regularly been in the 2.0 – 2.2 months-worth-of-inventory for the last few years. It has recently been climbing, and now represents almost 3 months worth of inventory. Last year, the first three months of inventory represented 2.2 months of sales. One could describe this number as the amount of time it would take to sell off the entire inventory. A year ago, that number was 2.2 months. Now it would take 3 months. That number is the measurement, the speedometer, of how much we are slowing down. Not stopping, not coasting, but slowing down. Looking at the bottom of this chart, you can see that all the price brackets are lower except for $750,000 – $1,000,000. This price range has 29% higher sales. That is the hot price range for the Conejo Valley. All other price ranges are significantly lower.

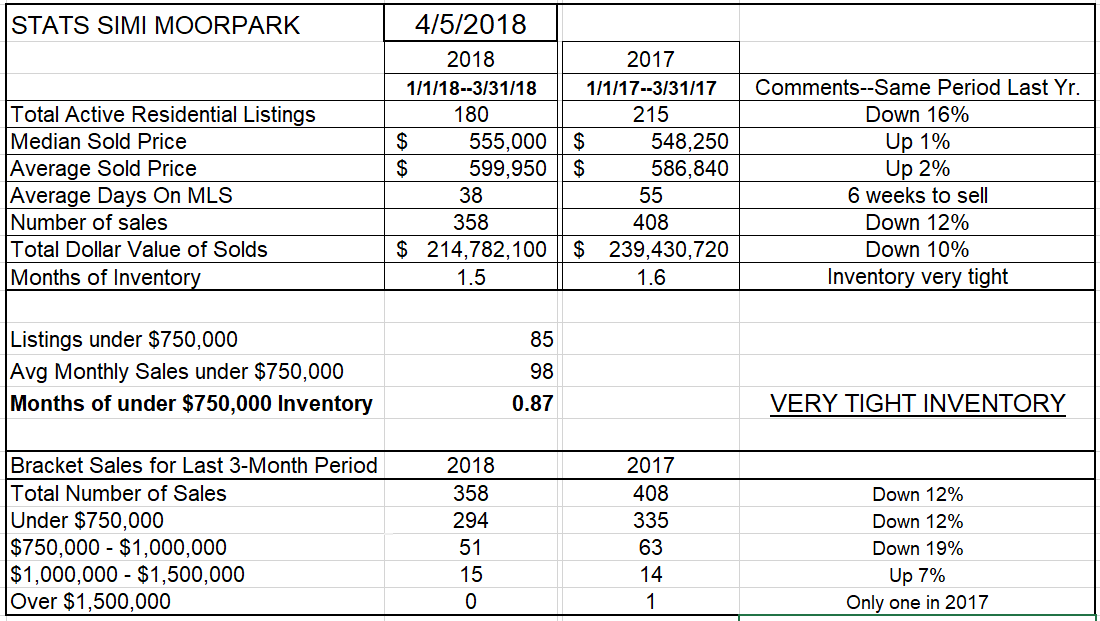

For Simi Valley/Moorpark, the figures do not yet reflect that slowdown. Inventory is down 16% versus last year. Prices are up, but only slightly, 1-2%. And sales are down, 12%. Is the inventory of available homes affecting sales? Most likely so. That speedometer figure for 2018 is at 1.5 months, lower than the 1.6 months in 2017. Look at the bottom of this chart to see that, except for the minimal sales in the highest price range, all price brackets are significantly lower compared to last year.

What does all this mean? Prices have not gone crazy (no bubble) and the inventory level is climbing for the Conejo Valley. Sales have slowed down, but now seem to returning to normal.

SImi Valley and Moorpark inventory is very low, and so are sales. And so is price appreciation. It is easier to find a home in the Conejo Valley because there is more inventory, more difficult to find a home in Simi/Moorpark because there are not as many to choose from. The price point has a lot to do with that. The median price in the Conejo is $770,000 versus $555,000 for SImi/Moorpark.

Unless we are surprised by some outside influences not currently visible on the horizon, the year is turning more normal, more like recent history. Maybe the market had the flu? But it appears to be getting healthier.

Have a wonderful month.

Chuck