No, my crystal ball is not what we will be looking at. Much better than that, at the end of this blog post I will be sharing the forecast from Jordan Levine, C.A.R’s chief economist. Who better knows the ins and outs of the most populous state in our nation? When you can hear the thoughts of one of our foremost housing economists, no sense me telling you my wild guess. The same goes for what you tell your clients. Better to reference C.A.R.

I was able to attend two presentations by Jordan in the last two weeks. Similar information, same forecast, but I really enjoy his low-key humor, it helps keep your attention, entertaining while learning.

I will share a couple of his slides that I found most interesting..

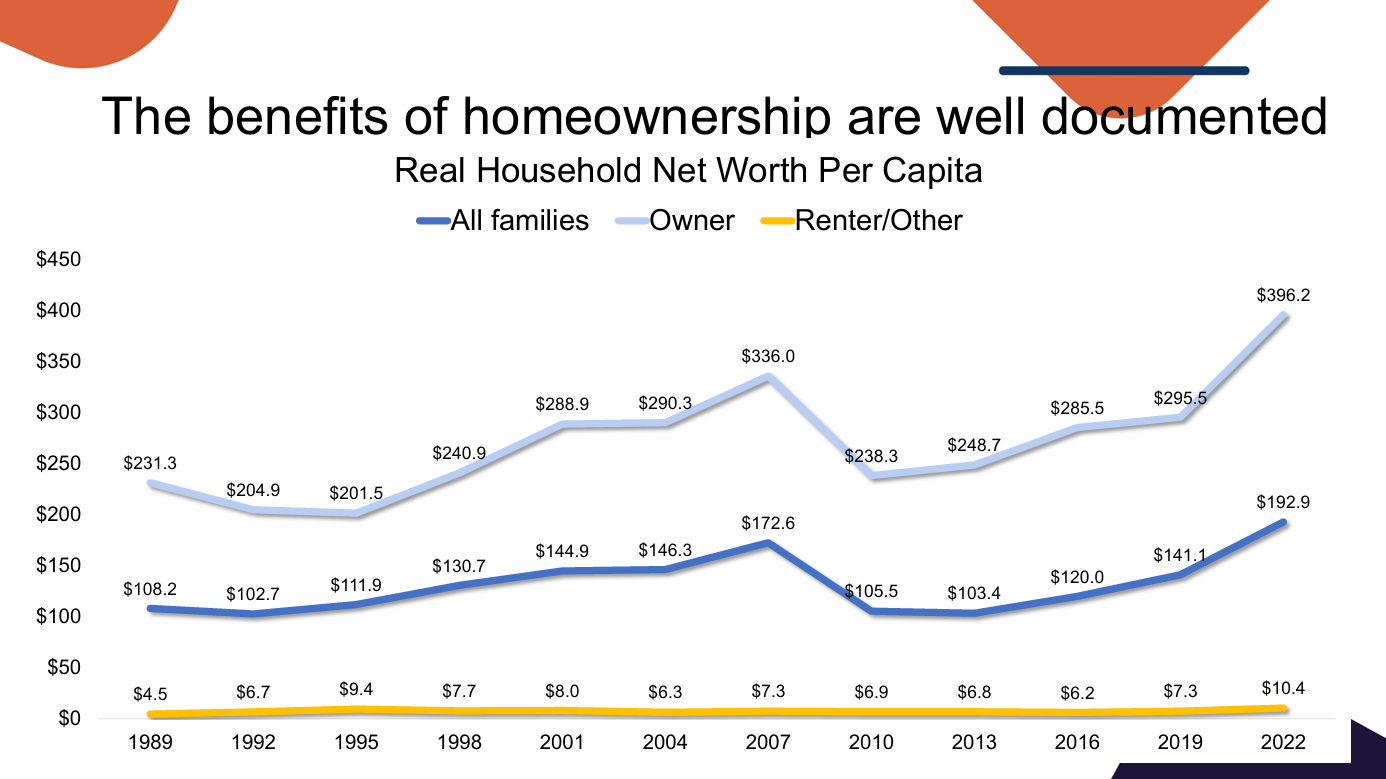

First, home ownership has proven to be the best wealth creator for the average American. I have interesting conversations with my grandson about the value of homeownership. Can you make more money in the stock market? Starting your own company? Investing in futures? Some have benefited from those, but the vast majority of the populace looks to homeownership as the smartest investment they have made. Instead of just arguing the point, let’s back it up with real statistics. This chart should convince you homeownership is more prosperous than renting.

This information on Net Worth Per Capita clearly shows the direct relationship between home ownership and Net Worth.

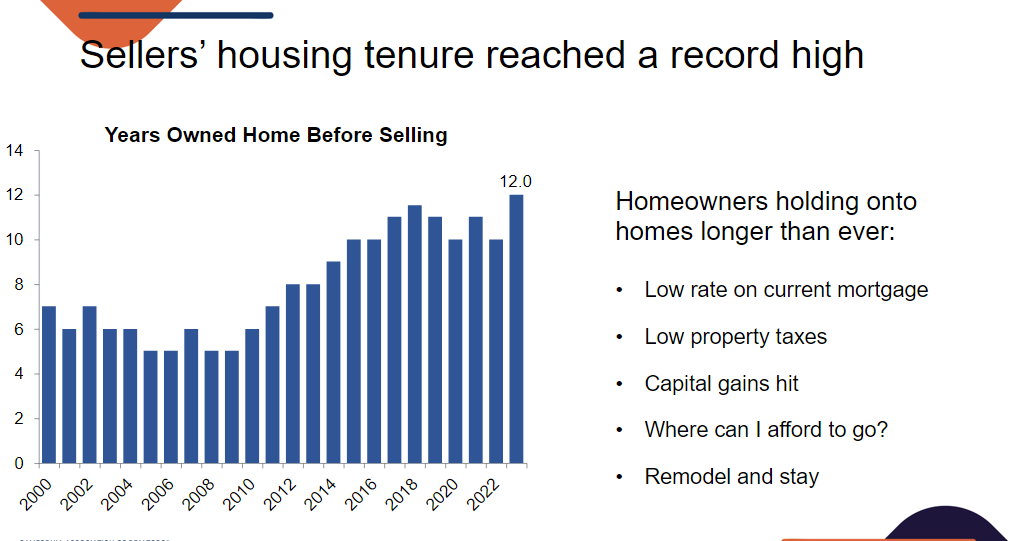

The next slide explains how times have changed regarding how long our homeowners remain in the same home before moving. A speech by Mayor Al Adam of Thousand Oaks discussed the maturing of our local society. In the 70s, most everyone moving to our area was young with a couple of school age kids. Combining the age of young parents with the age of their children, the average age in our area in 1970 was 21. Today that average is 44. Younger kids are no longer a predominant element in lowering the average age, and many of us that raised those kids are now enjoying our grandchildren. Both factors raise the average age. Due to family creation, the 70s and 80s, even the 90s, saw homes change hands every six years on average. Today that figure is double.

Lower turnover partially explains why inventory is low. Another factor is mortgage rates. Homeowners are hesitant to give up their 3% mortgages for mortgages with twice that payment. There remain many reasons why homeowners decide to move, but that young family segment looking for a bigger home, with a larger mortgage paid for by a promotion at work, has become less of a factor. And for the older set, fixed incomes do not foster upscaling.

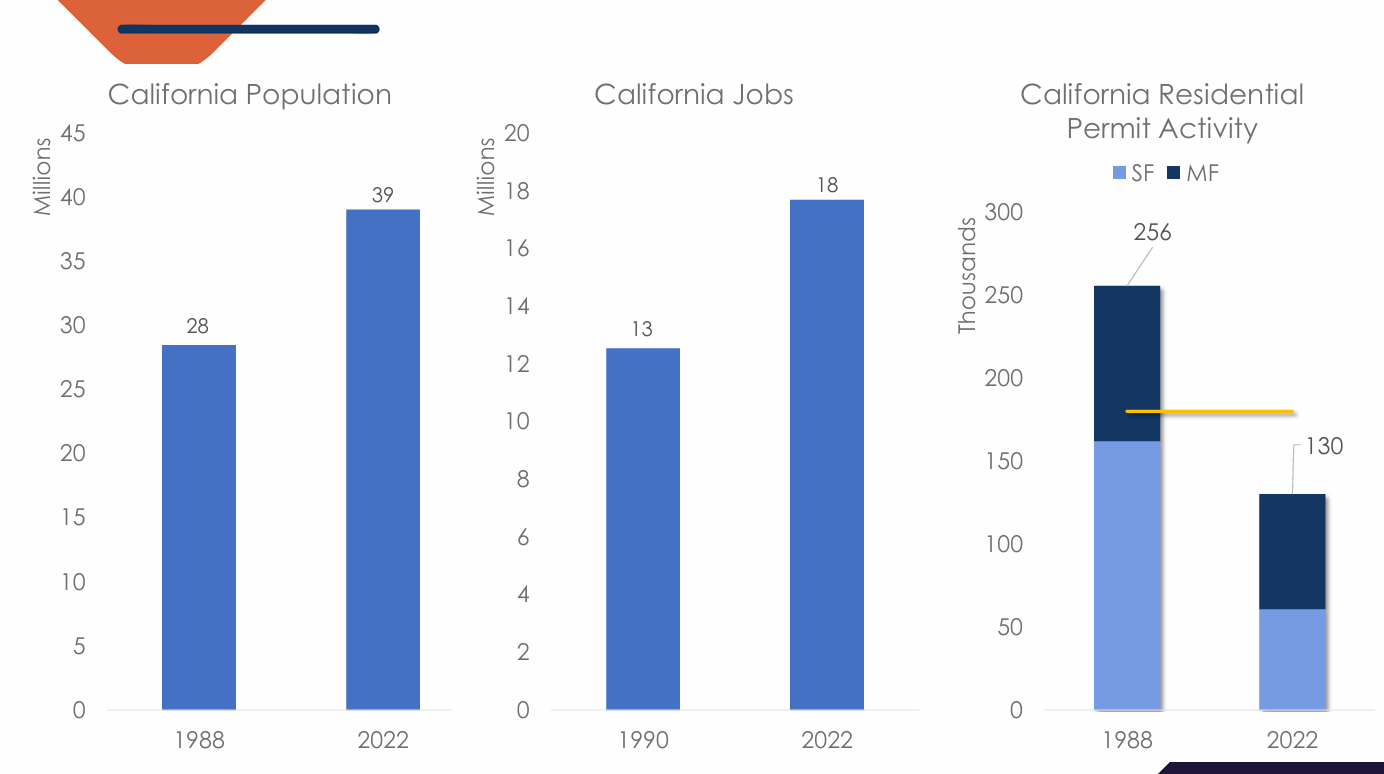

Another factor to consider is the shortage of housing units. In 1988, the population in California was 28 million. In 2022, populaton increased by almost 40% to 39 million. During the same time frame, annual residential building permits declined from 256,000 per year in 1988 to only 130,000 in 2022, a drop of almost 50%. As the population was increasing, the number of new homes was not keeping pace.

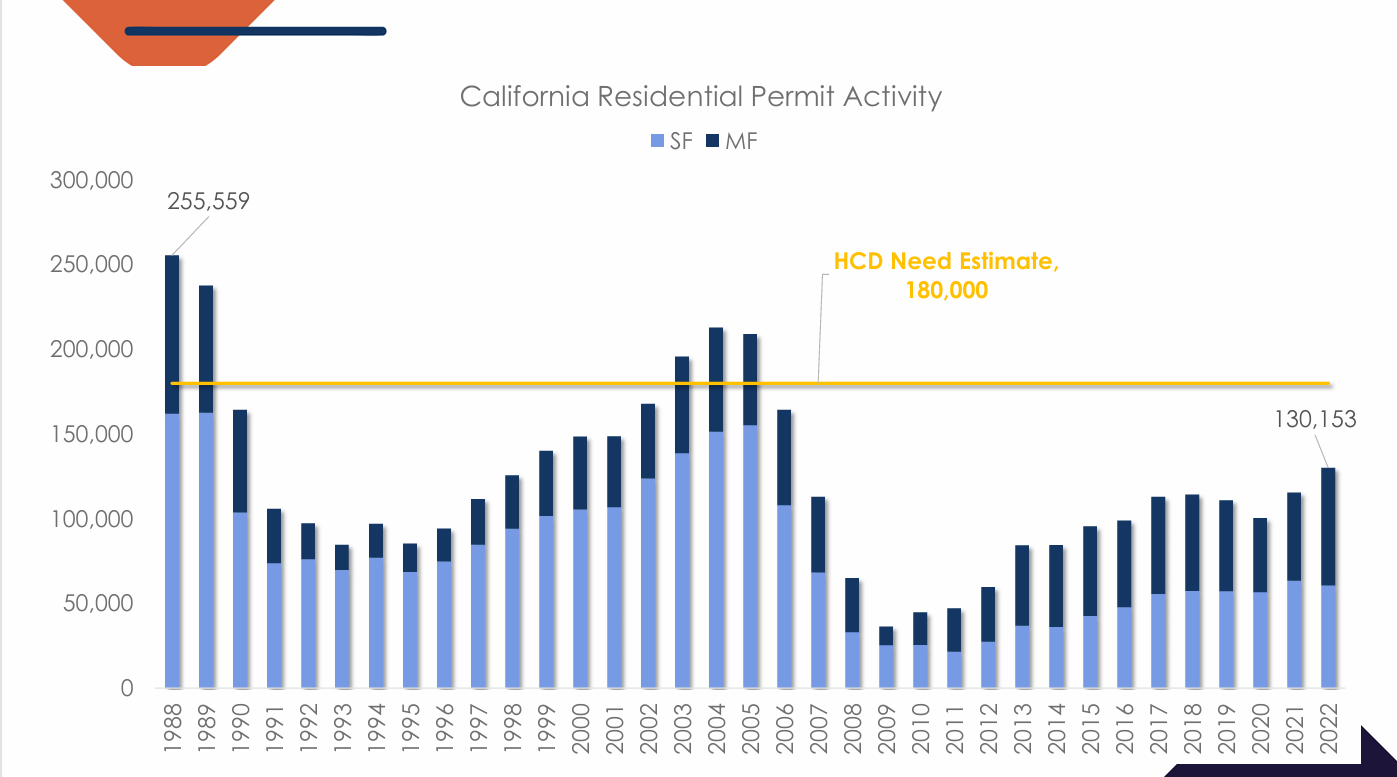

To picture what the lack of residential permits looks like more clearly, the graph below describes how housing creation has been declining. Our annual housing needs compute to 180,000. We have exceeded that number only five times since 1988. All the remaining years have contributed to the housing shortage.

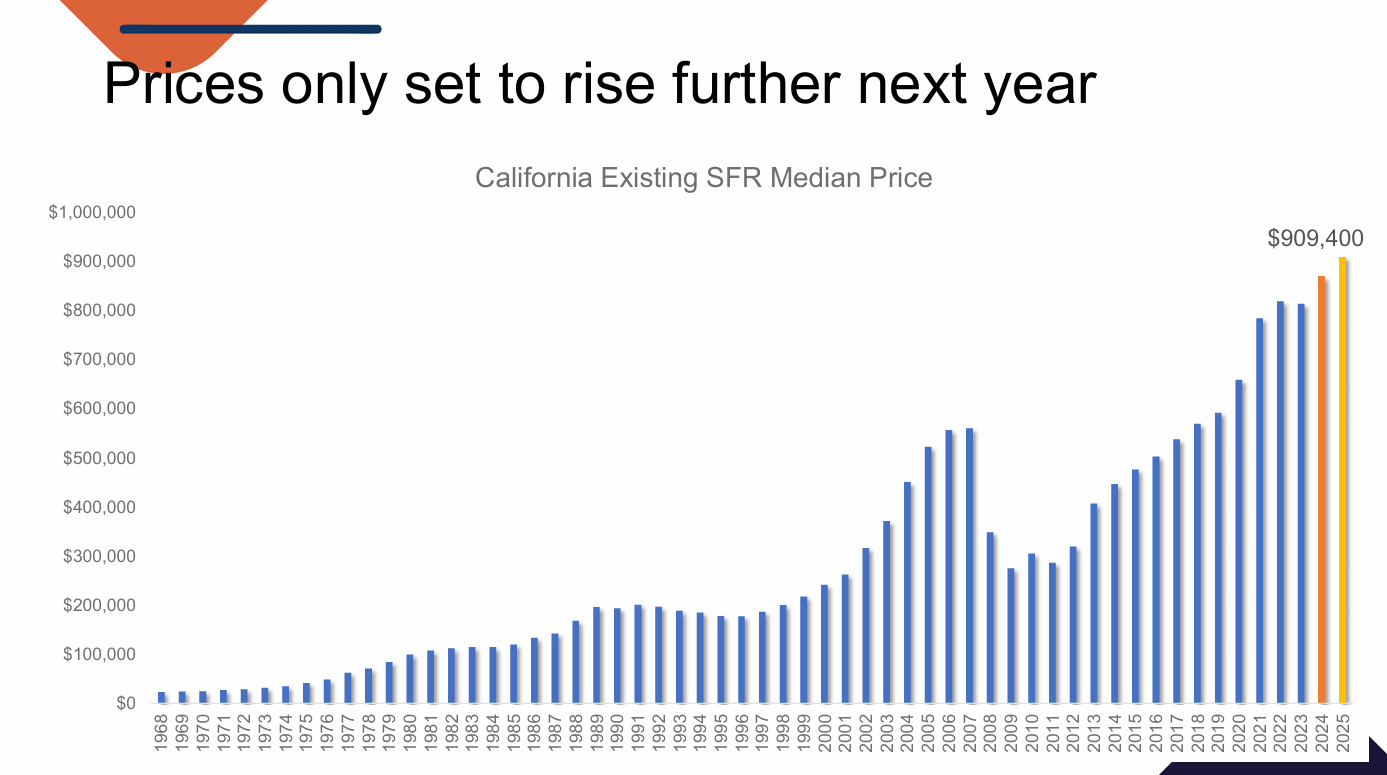

What happens when housing production does not fill the need for housing? The Law of Supply and Demand says that when supply does not meet demand, prices go up. SInce these statistics deal with all of California, we next take a look at the history of housing prices state-wide.

Prices continue to climb even though population growth has leveled out, or slightly declined. Selling a home is more a decision guided by individual needs and life happenings rather than a pure financial decision. However, tax considerations have entered the picture, with taxes on capital gains becoming a major concern, one which Realtors are strongly lobbying to change. Hopefully next year will see the capital gain exemption amount move from the current $500,000 per couple to double that, and indexed for future years. It is one of NAR’s most important lobbying efforts.

There are many reasons why people move: births increasing family size (and deaths), marriages creating new family units (and divorces), new jobs and transfers (and job losses), improvements in monthly income (versus fixed incomes). Lots of reasons to list and to sell.

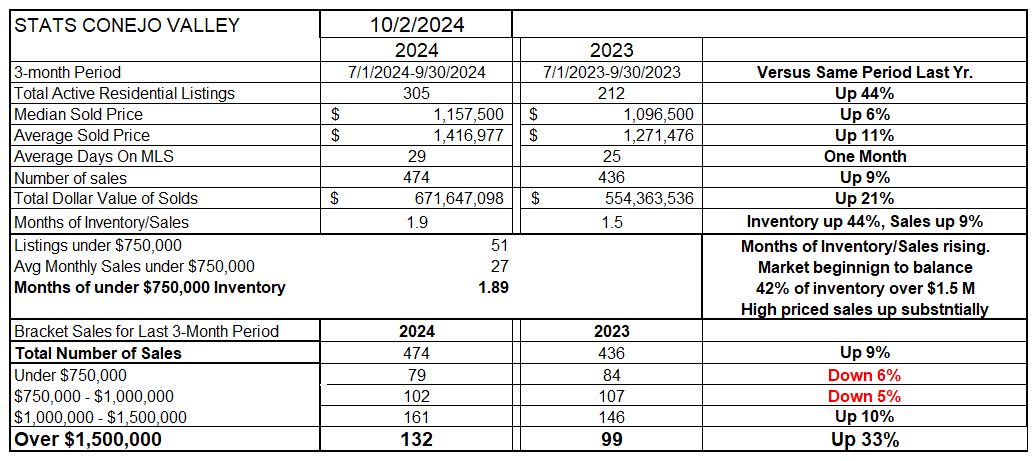

Now on to the statistics for our local areas. First, the tables giving the overall changes in our marketplace. Our marketplaces are beginning to diverge. For the Conejo Valley, inentory is 44% higher than last yer. Prices are an interesting topic, with Median Prices up 6% year over year, actually quite understandable and reasonable. But the Average Price is up a whopping 11%, almost double the Median price increase.

Median prices represent a midpoint, the price at which the number of homes sold for a higher price is equal to the number of homes sold at a lower price. But the average is the computation of the total value of all the homes sold divided by the total number of homes sold. For Conejo, there has been a dramatic increase in the highest end of the market (see bottom of this table). That affects the average price much more than the median. A very large percentage, 42% of homes listed, are priced over $1..5 million. And for Conejo, the number of homes sold the past three months are up 9% over the number of homes sold in the same period a year ago. This part of the market is very strong, and is a precursor of what the rest of the market may see.

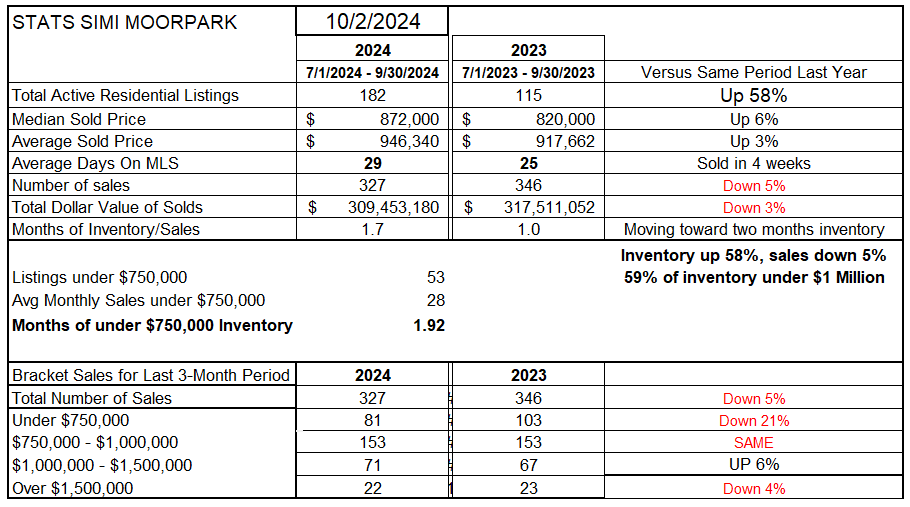

SImi Valley/Moorpark is a different market. High priced homes exist, but are less of a factor versus Conejo. Inventory has increased 58% versus a year ago. Their Median Price is also up 6%, but their Average Price is up only 3%. The number of sales is lower than last year by 5%. Homes priced below $1 million represent a large 59% of the inventory. A marketing person would describe that as “product mix”.

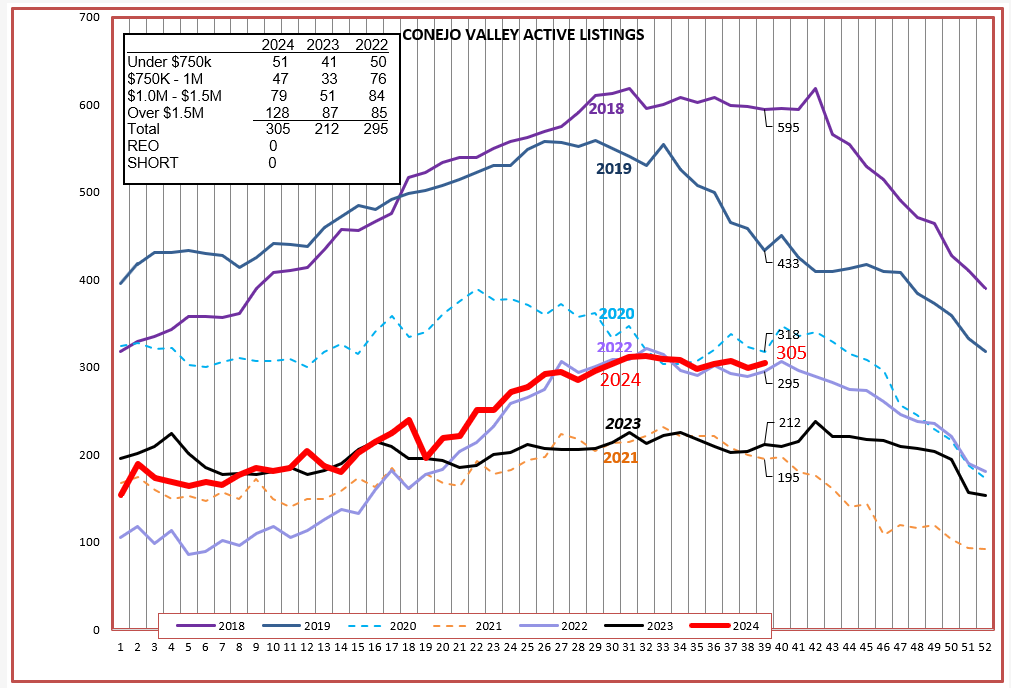

Going through the individual charts, next is inventory. For Conejo, the 2024 graph is following the pattern of historic trends, particularly those not influenced by Covid. The current number of listings is far lower, 212 in 2024 as compared to almost 600 in 2018. But the shape of the graph is the same, just lower.

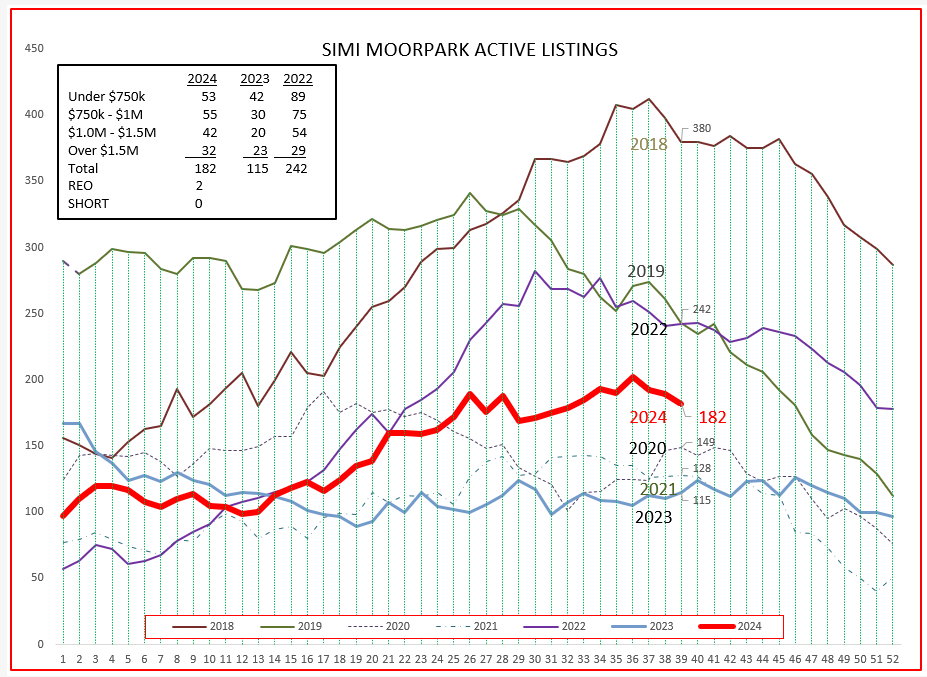

For Simi/Moorpark, current listings are about half of listings in 2018, 182 in 2024 versus almost 400 in 2018. The 2024 pattern is following the normally expected pattern as the year progresses.

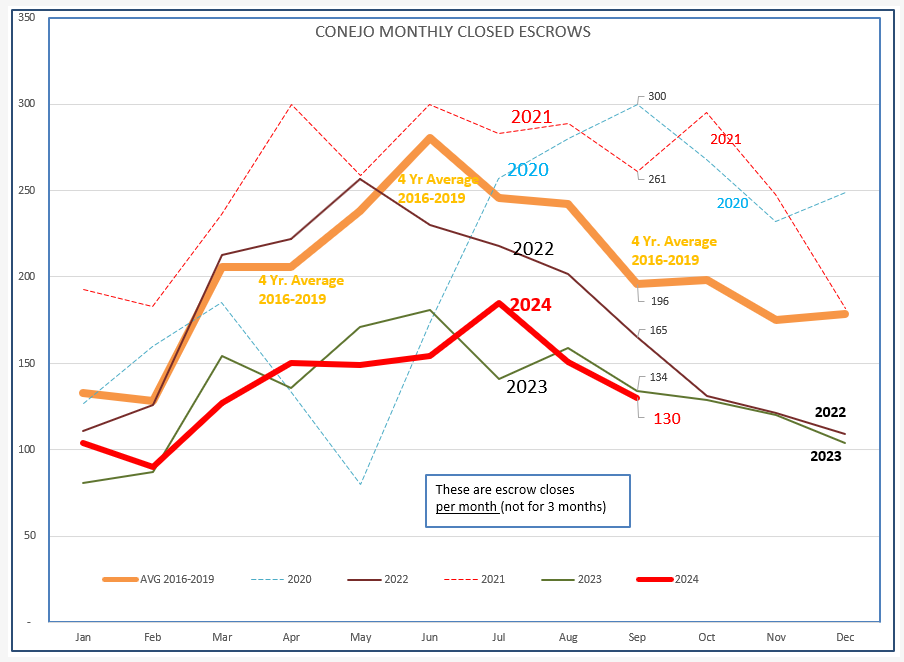

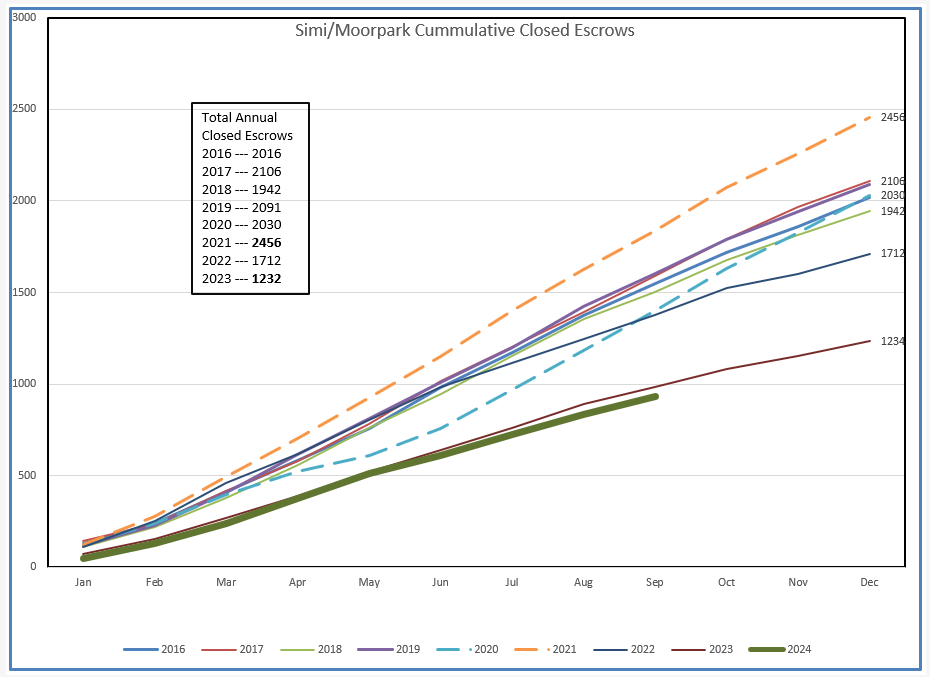

Next we have closings (solds). There is a pattern here also, and if you compare the 4-year average (heavy orange line), 2024 is progressing as expected. but at a much lower level.

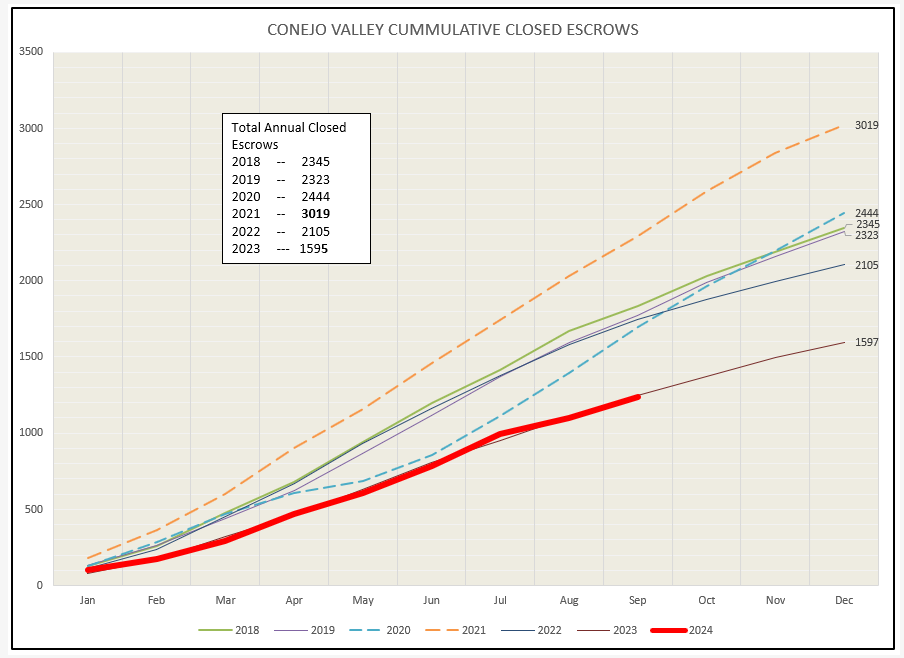

How much lower closings are can be better seen in the chart below. The cummulative number of closings is progressing very similar to 2023, one of our lowest sales years on record.

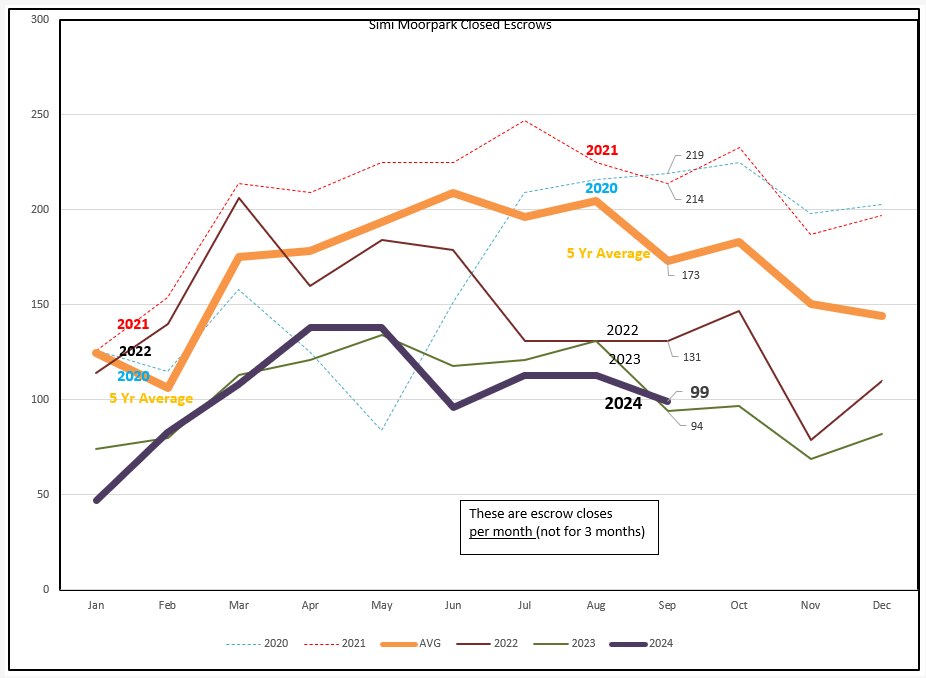

For Simi/Moorpark, the same comparison can be made, with current 2024 closings of 99 units comparing to the 5-year average of 173.

Again, this level of sales is very similar to 2023. Unfortunately.

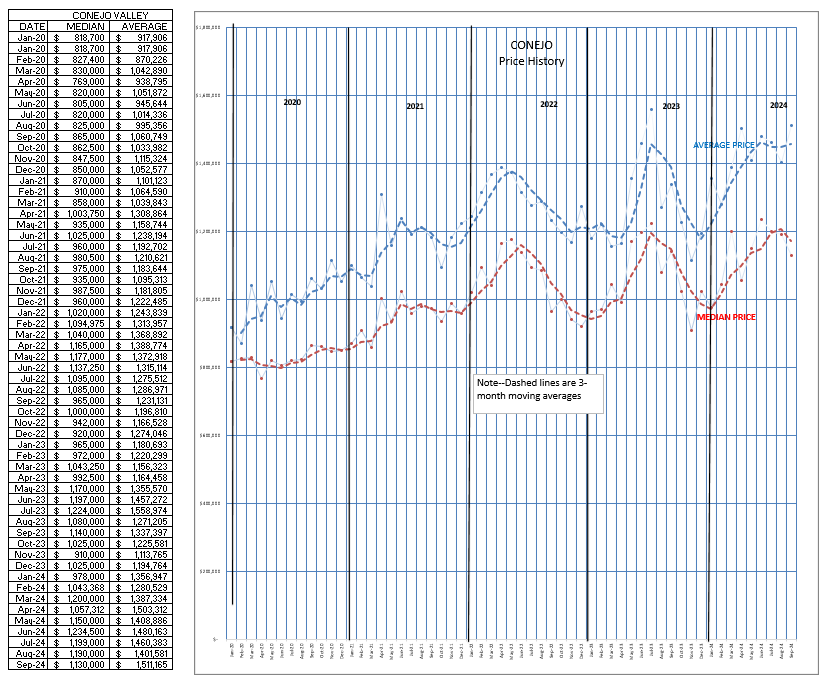

Finally, prices, starting with Conejo. The Average Price has hit $1.5 million for the second time in 2024. As we head into the end of the year, prices have historically been going down after peaking during the summer months. The Median Price is following the usual pattern, but the Average Price is showing unusual strentgh.

For Simi/Moorpark, the price chart represents a very different pattern. 2022 showed a similar pattern to Conejo, higher in the summer and decreasing as we head into the end of the year. But 2023 and 2024 did not follow that pattern. This one is difficult to explain. Ideas, anyone?

So that is what happened. What will the market look like in the future?

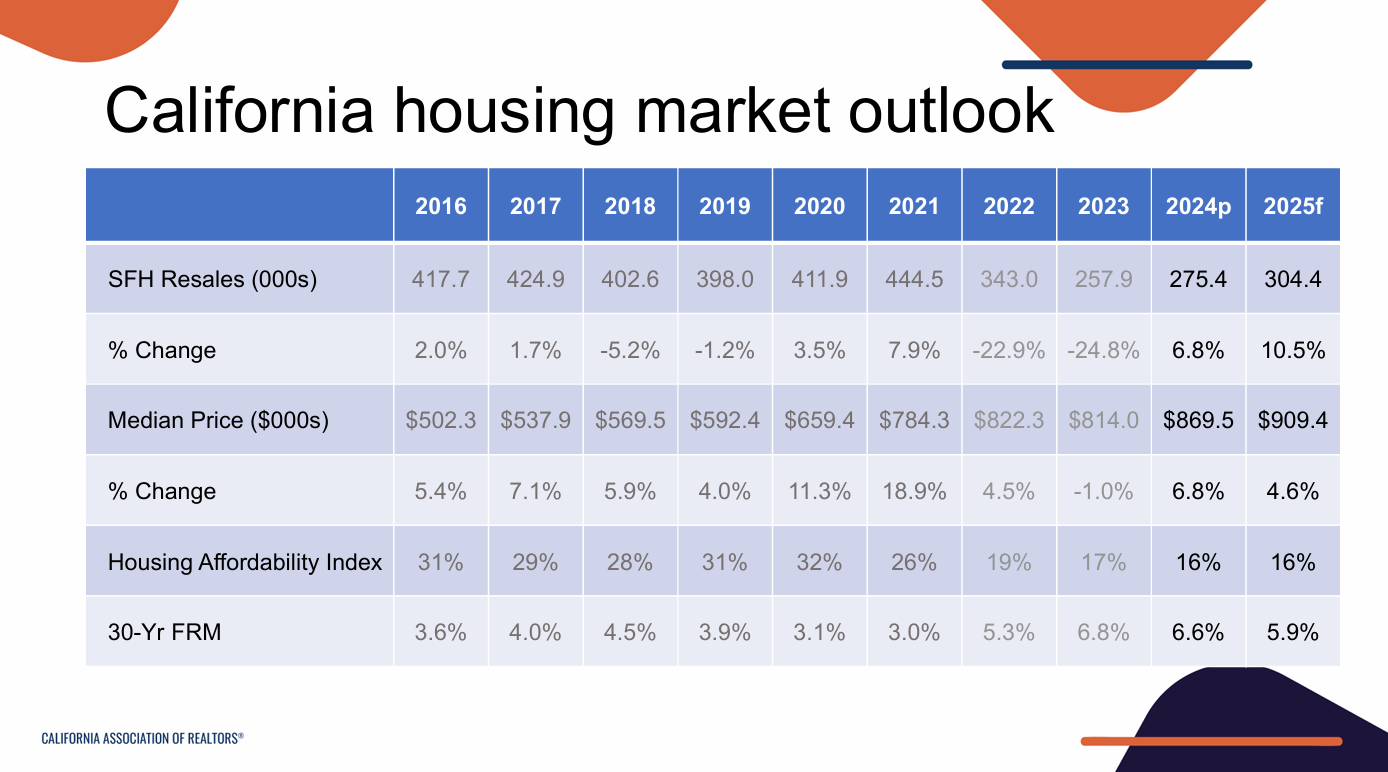

Thanks to Jordan, here is the C.A.R. forecast for next year. The number of sales in 2022 and 2023 dropped 23% and 22% from the previous year. C.A.R. is suggesting we will gain part of that back (up 6.8%) by the end of this year, and up another 10% in 2025. Good news in prices is bad news for affordability, with only 16% of buyers now able to buy an average price home.

Jordan is forecasting mortgage rates to be 6.6% by year end and down to 5.9% by the end of next year. That’s not bad. Over the past 50 years, mortgage rates have averaged around 6%.

So that’s where we stand. That’s the professional outlook. But whatever happens, as long as you have knowledge about what is occurring, that makes you valuable to your clients. Share this important forecast. Your clients will have questions like “How’s the market” and “What is my house worth”. Use this information and let your clients know it is the authoritative C.A.R. forecast, brought to them by you, their agent. It gives you great credibility.

Next year our associations will be having important discussions with Congress, as our country gets a new President and Congress has to deal with the expiration of the tax bills, passed in 2017 and expiring in 2025. Next year will be very consequential for housing.

“May you live in interesting times” is an English expression that is claimed to be a translation of a traditional Chinese curse.

We sure are living in interesting times.

Chuck