Apologies that my blog is late this month. The good news is that I got a new computer. The old one was misbehaving. The bad news is that I tried to work with Dell and Microsoft for over three weeks to no avail to get my printers hooked up properly. I hope Dell makes better computer than they do customer service.

Thank goodness for my tech wizard Chris Elbert. evolvinggeek@gmail.com (805) 338-6464. Brilliant, timely help, very reasonable prices, and can fix most problems remotely. He was able to get everything organized and working again. If you need a personal or work computer guru, I cannot recommend him more highly.

Now on to the statistics. First Conejo, comparing the last three months averages to the same three months a year ago. Listings are up 31% (a great realtor gift for under the tree). Median Prices were up 5% while Average prices were up 8%, the disparity a function of the comparatively larger amount of high priced homes being sold this year versus last year (up 28%). The total number of homes of all prices were up 4%. Inventory now represents a full two months worth of sales, which for our market I consider a balanced market, even pressure between buyers and sellers.

SImi Valley and Moorpark are a little different, mainly due to the concentration of Median priced homes in Simi/Moorpark and the comparatively fewer highest price category homes. Inventory was up 31% versus last year, and both Median and Average prices were up 4%. The number of home sales increased dramatically, by 21%, a function of the extremely low inventory a year ago. The low number of listings in 2023 kept sales numbers down. Happily the inventory increase in 2024 provided for more sales.

The Active Listings graph is follows the normal annual trend of increasing toward the summer and decreasing toward the winter, but at a much lower level than the non-Covid years of 2018 and 2019. While 2022 and 2024 total listing numbers were comparable, notice the increased inventory of highest price homes in the inserted box. This is both a function of price increases, moving more homes into that highest price category, and the fact that these highest price home sales do not rely as much on mortgage availability than the lower priced levels. Buyers for these homes can either pay all cash or can get short term mortgages which will be refinanced when rates go down.

For Simi Valley/Moorpark, the available inventory is staying high, which is keeping price increases reasonable (4%) while allowing sales numbers to be much stronger.

Conejo Closed Escrows very closely mirror the 4-year non-Covid average, but at a lower level. The lower level is mainly due to mortgage rates stubbornly at 7%. If prices were lower and mortgage rates were lower these closed escrows would be approaching the November average of 175 instead of the actual of 130.

For Simi/Moorpark, a similar pattern exists, with the 5-year average of 151 compared to the November 2024 actual of 101.

Looking at Conejo sales that accumulate as the year progresses, we can see that 2024 will end up similar to 2023, not exactly a banner year. Normal should be about 2400 sales, with both 2023 and 2024 only 2/3 of that number.

Simi/Moorpark is similar, with 2,000 sales in a normal year versus the 2023 and 2024 coming in around 1,200. Homeowners can be happy about their prices, but Realtors are sad about the volume.

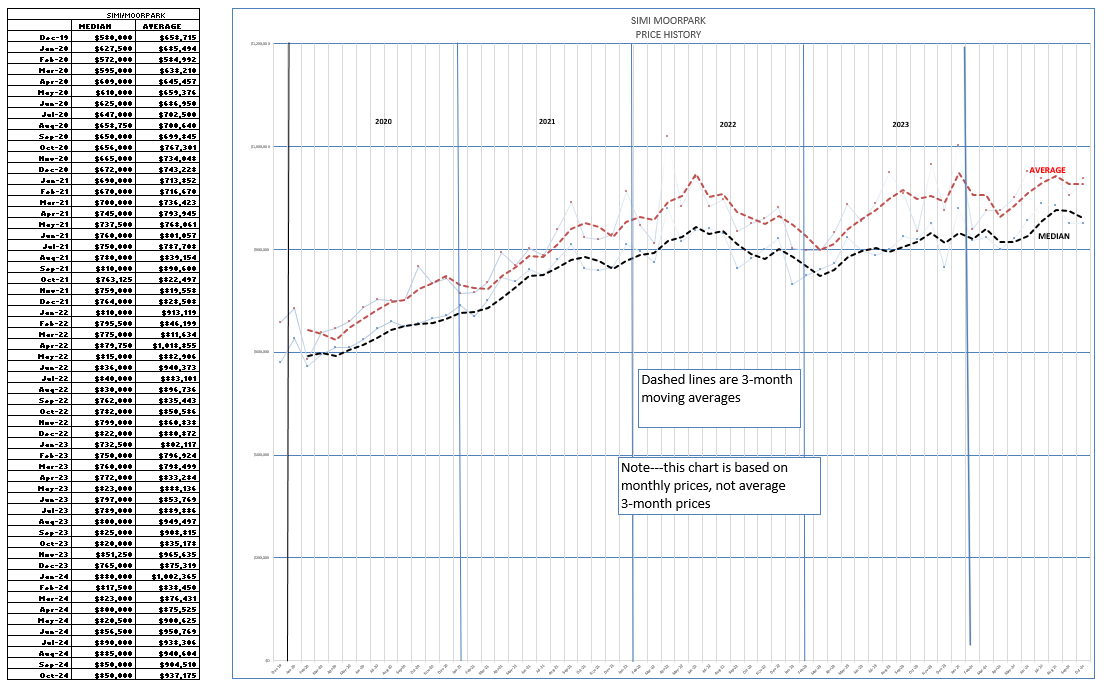

Lets finally look at how prices have been reacting to these inventory and closed escrow numbers. This chart is a little different from the prices in the statistics chart, as they represent the median and average for each particular month, not a three-month average. It is interesting how prices are following the same annual pattern as inventory and sales, increasing going into the summer months and decreasing as we head into winter.

Simi/Moorpark has had similar history, but 2023 showed a rise at the end of the year as mortgage interest rates declined in expectation of the FED reducing rates. Outside of that anomaly, prices are also following the annual trend.

So there we have the November results. I have spared you my comments about how poitics and the election influenced what is happening. Frankly, it is because I really have no idea. And it would be difficult to compete with what the various “news” channels are saying.

The future will be interesting, as in the saying “May You Live in Interesting Times”.

All I can pass on are sayings that are based in history.

As ye sow, so shall ye reap.

You have to chop the wood for the fire before you can feel the heat.

In other words, work hard, contact your past clients, develop new clients every day, treat your clients like family, and you will do well.

Be the real estate expert everyone goes to for information.

Happy holidays.

Chuck