Changes are taking place in our local real estate markets. And depending on the market, the changes are different.

Let’s look at the statistics tables to see what I mean.

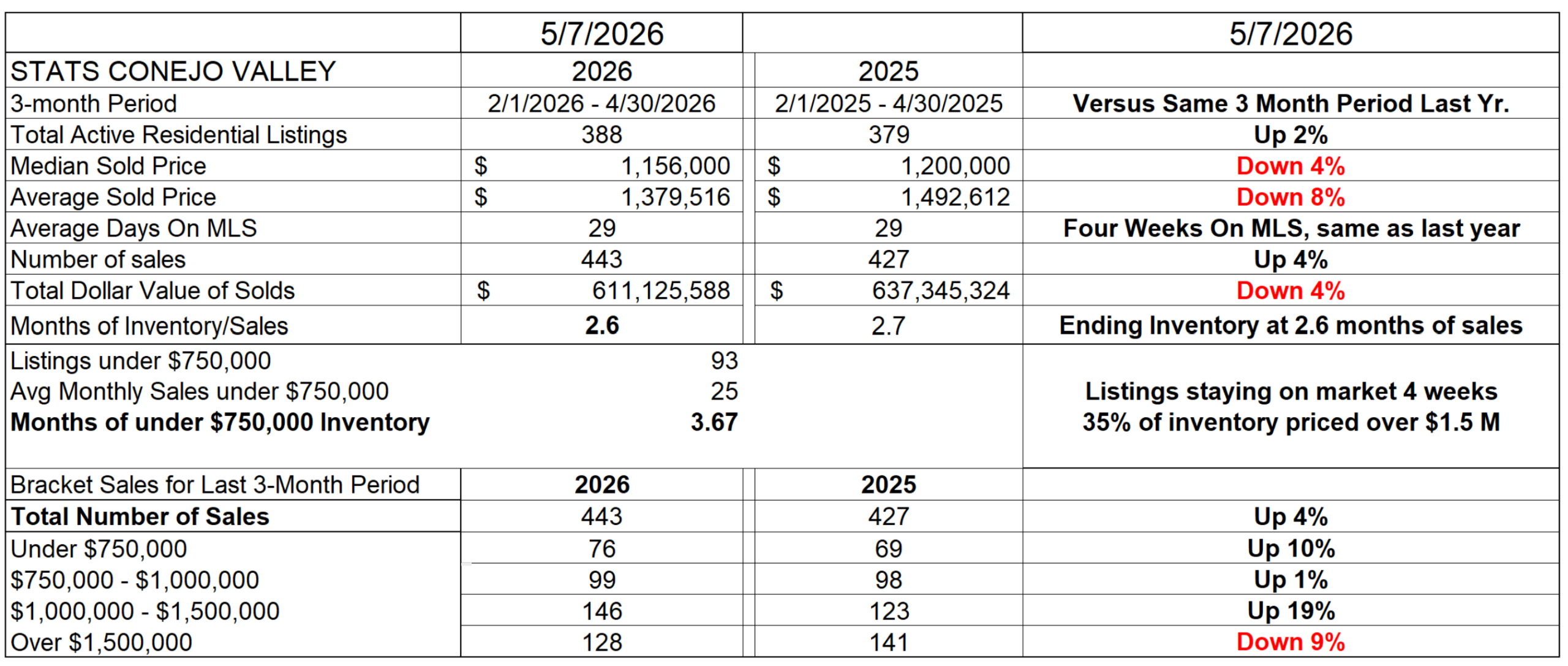

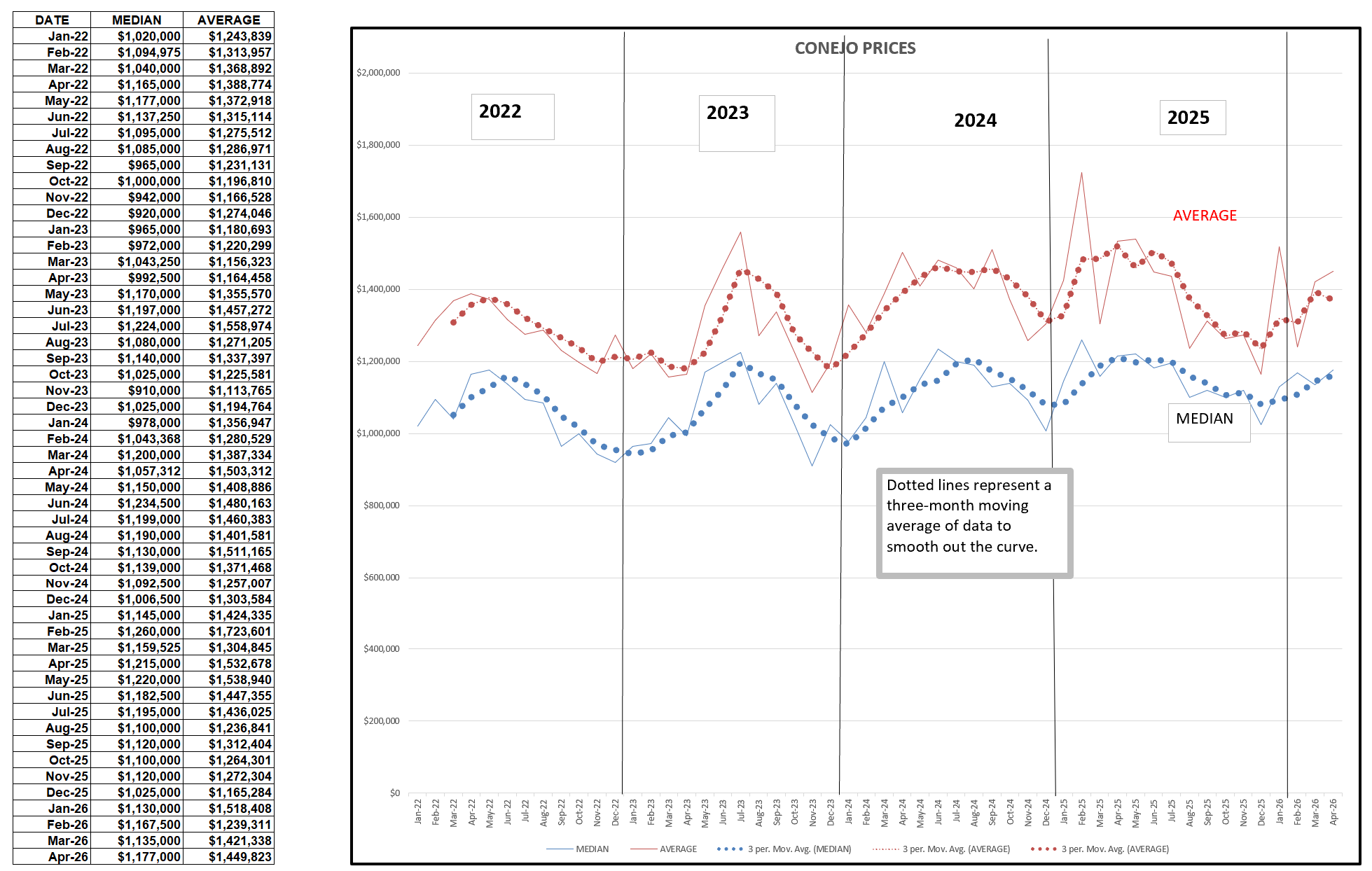

For the Conejo Valley, listings are at a reasonable level, up 2% from a year ago. But prices took a dive, Median down 4% and Average down 8%. It was nice to see sales climb 4% from a year ago, and the months of inventory based on sales slipped slightly to 2.6 months. The lower portion of the table shows that most sales were doing well, particularly in the $1 million to $1.5 million range, but homes priced above $1.5 million declined 9% from last year’s number. and 35% of the total active inventory is above $1.5 million.

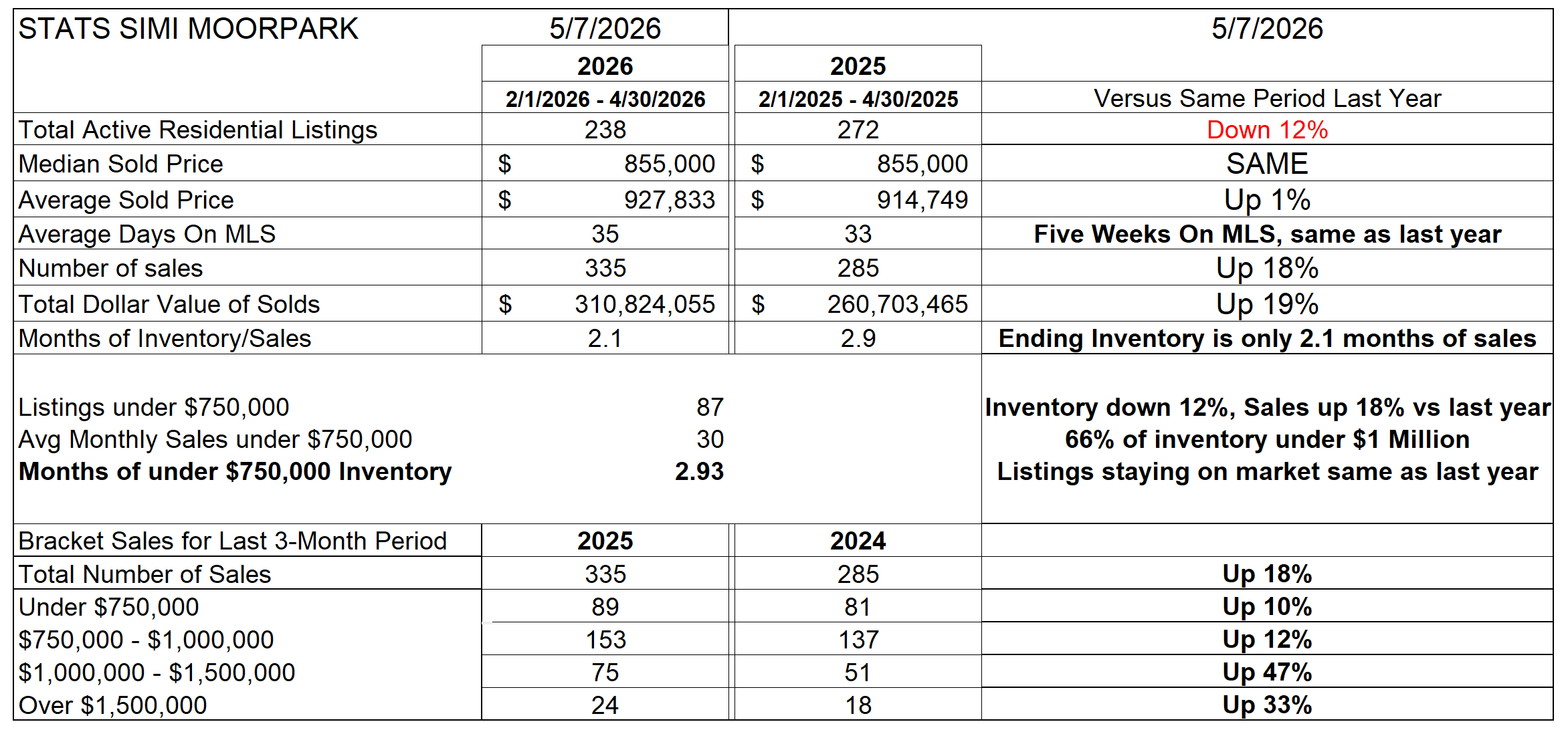

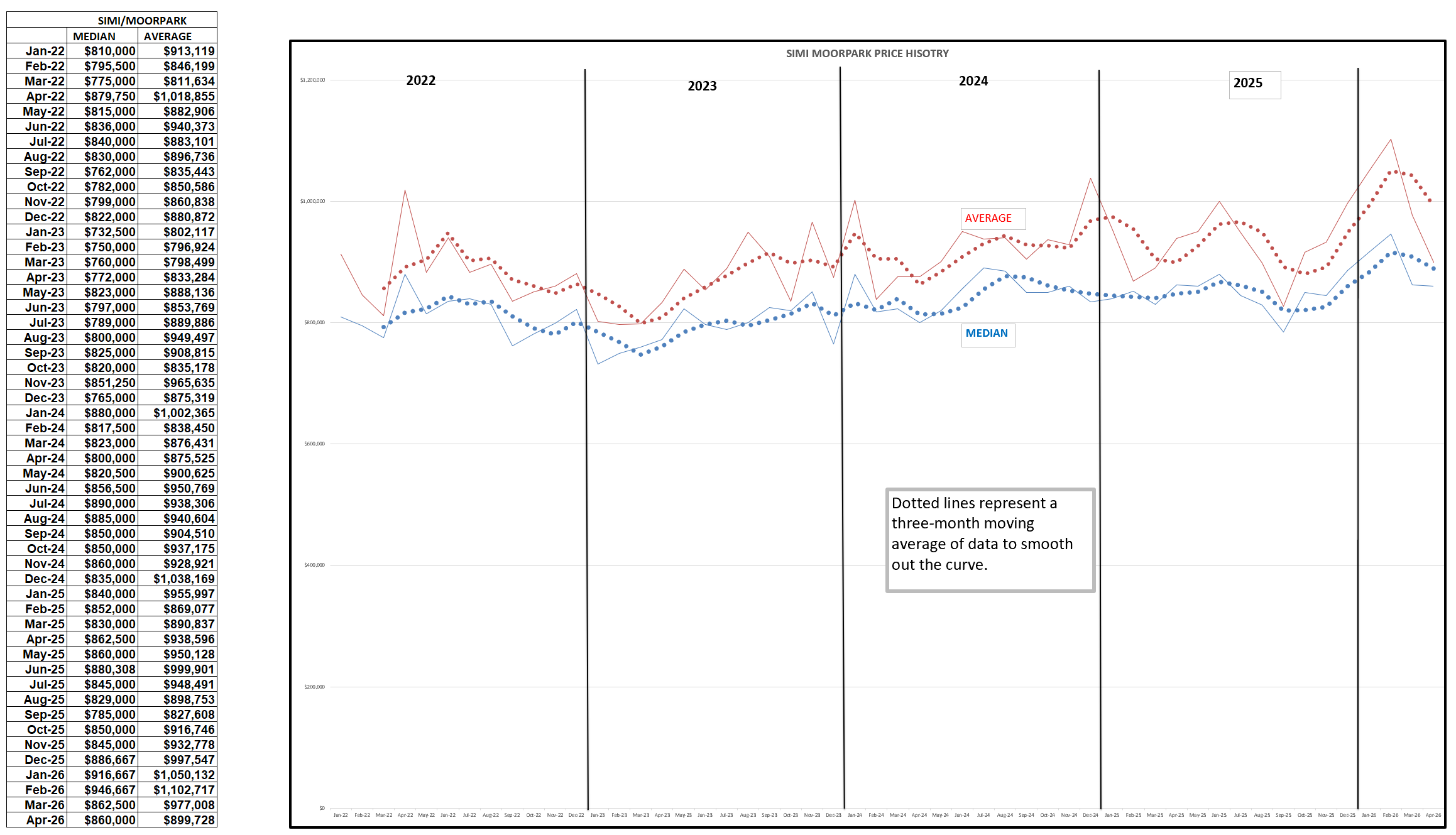

For Simi Valley and Moorpark, a different market result. Inventory is down 12%, logically due to the number of sales increasing 18% over last year’s experience. Median prices are the same, while Average prices are up slightly. The number of sales was up a whopping 18%, and the decrease in listings brings the months of inventory down to only 2.1 months. Hence the relative (to Conejo) strength in pricing. The bottom portion of the table shows that sales increased strongly in all price categories. With 2/3 of the inventory priced below $1 million, Simi/Moorpark is more affordable and the market is stronger.

More reasonable pricing has definitely brought about more activity. See the article on LA condo prices HERE.

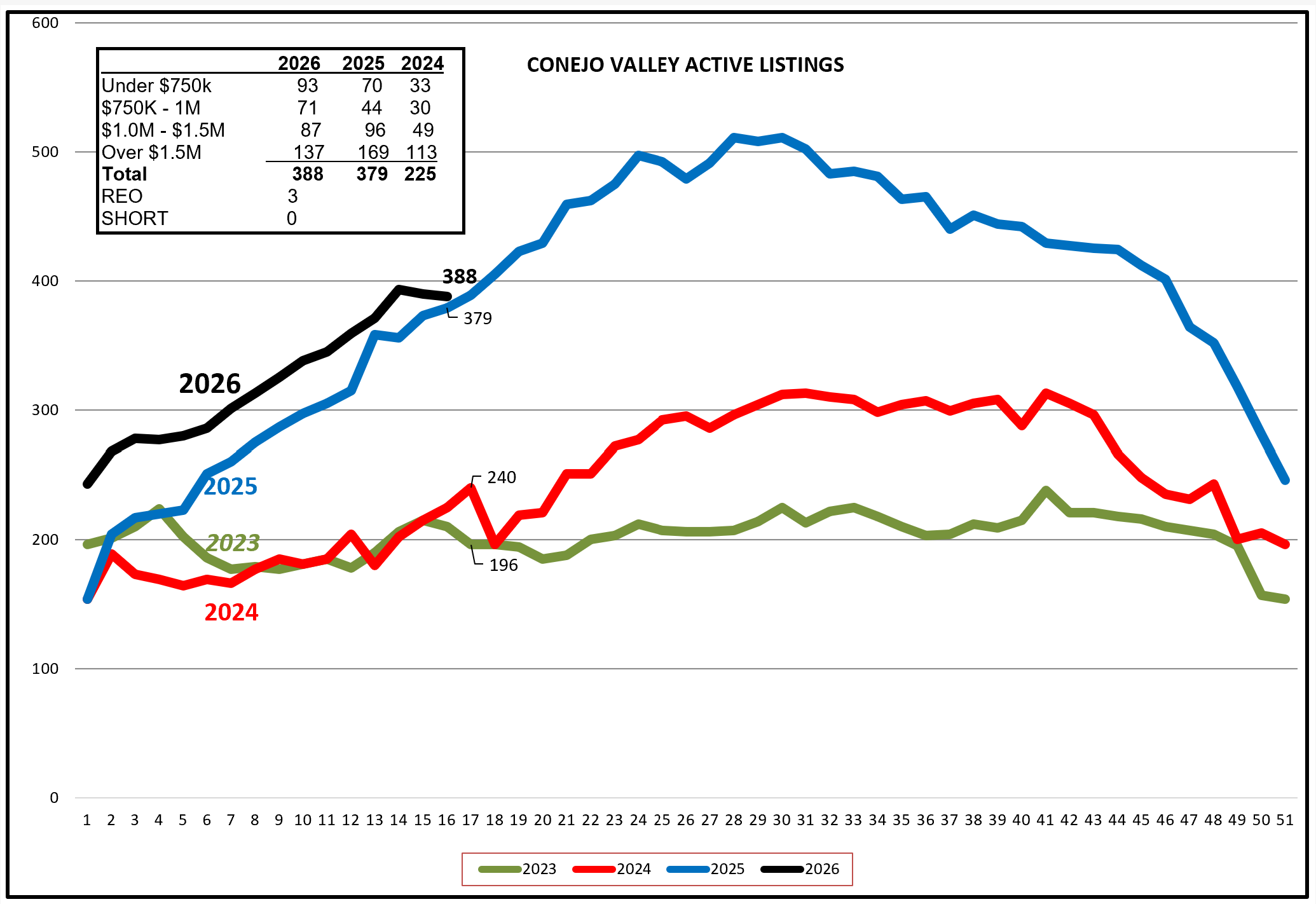

Active inventory for Conejo is following the same path as 2025. Also note the 3 REO listings. Previously we saw REO listings missing entirely. Having a few REO listins is perfectly normal. Life happens, and occasionally families have difficulty hanging onto their homes. The good news is there is adequate inventory from which buyers can choose.

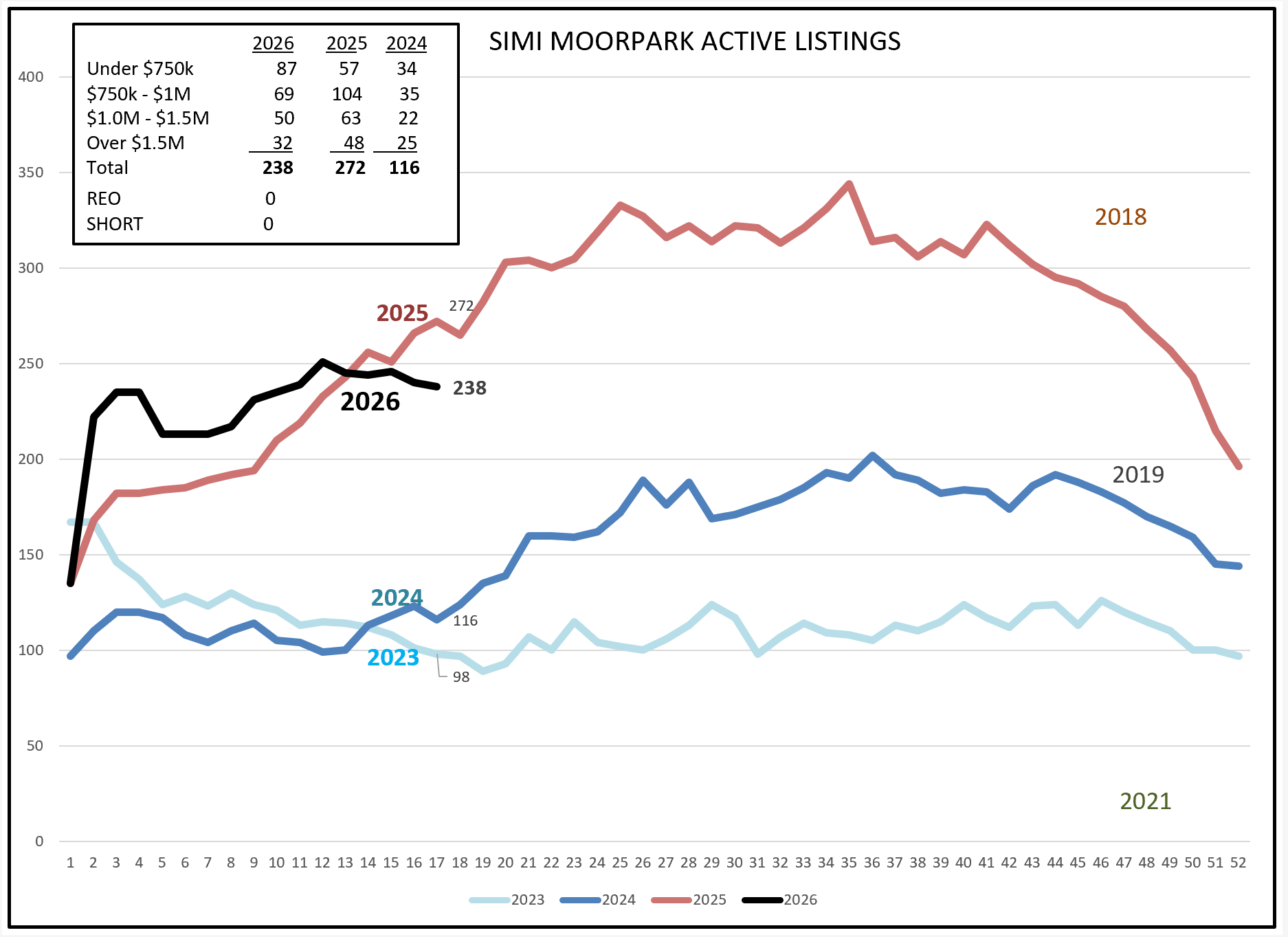

For Simi/Moorpark, the huge increase in sales has removed a lot of inventory from the market.

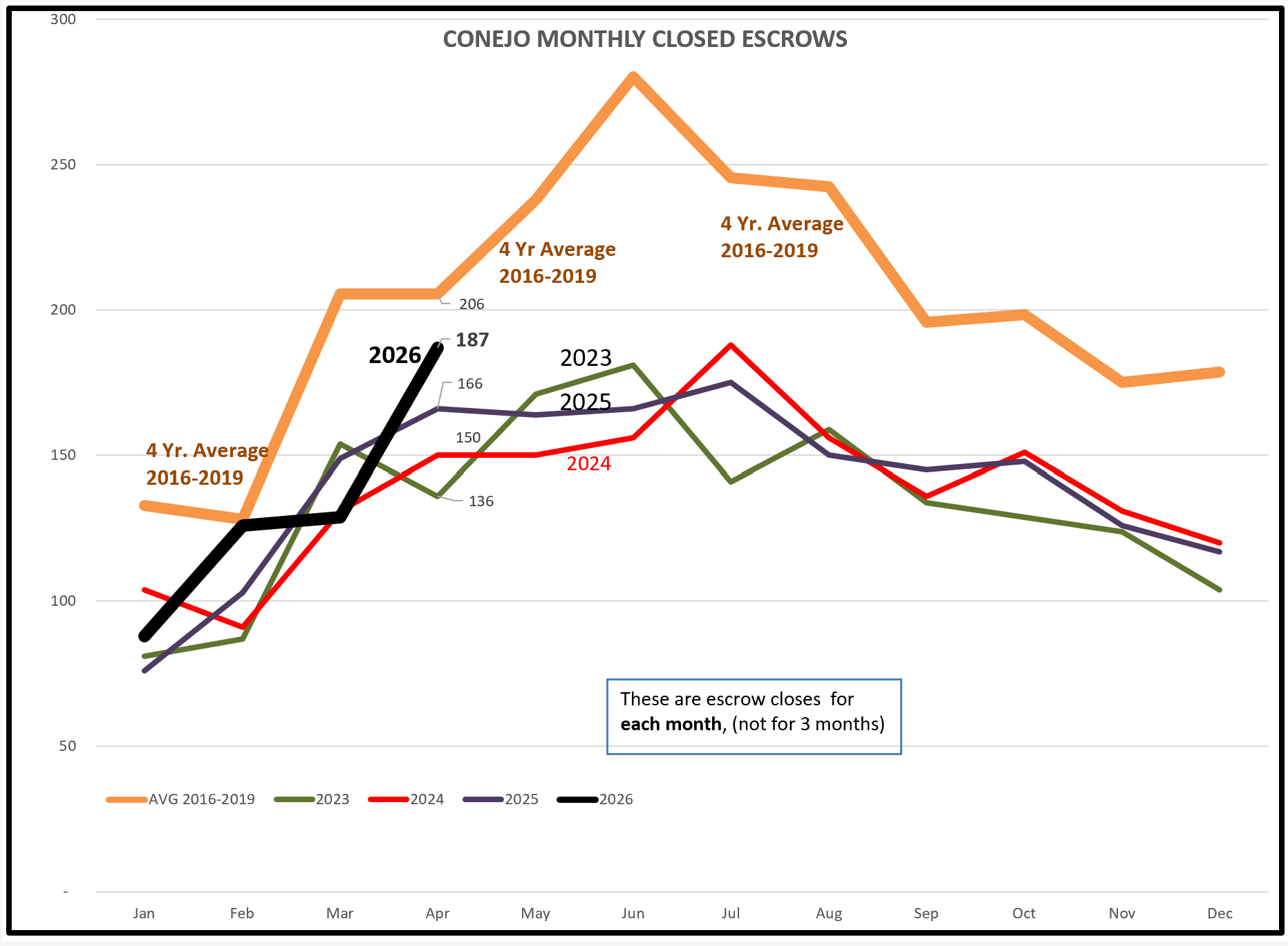

Conejo Sales figures are increasing. The table we began with shows sales increasing 4% compared to last year, but that is a 3-month moving average figure. The chart below shows that sales for the month of April appreciated strongly, correcting the weakness in March. Expect to see this chart look more like 2025 next month.

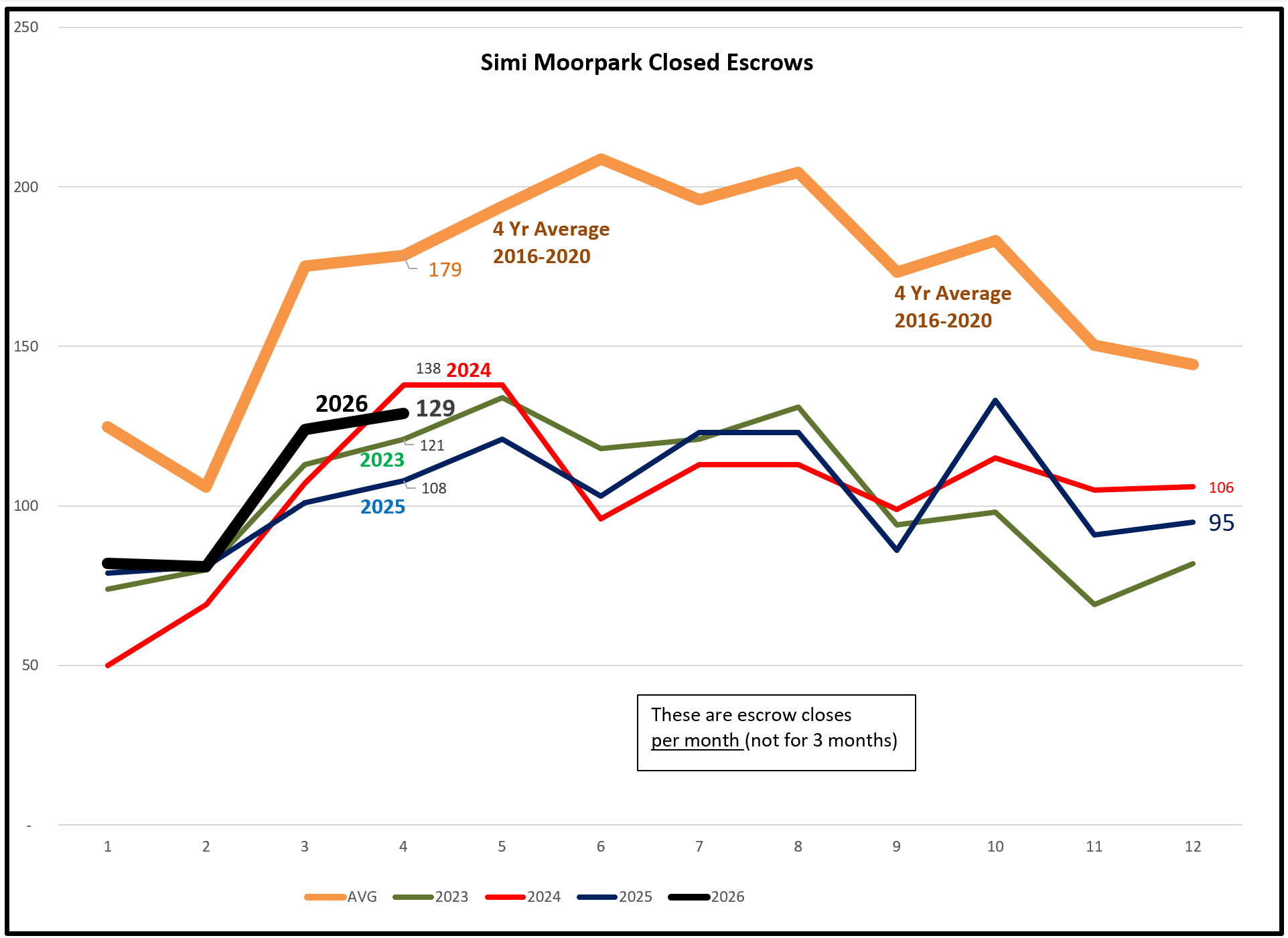

Closed sales for Simi/Moorpark were just the reverse. The table showed 3-month sales increasing 18%, but the month by month chart below shows that sales were comparable to the past few years, and have increased compared to 2025.

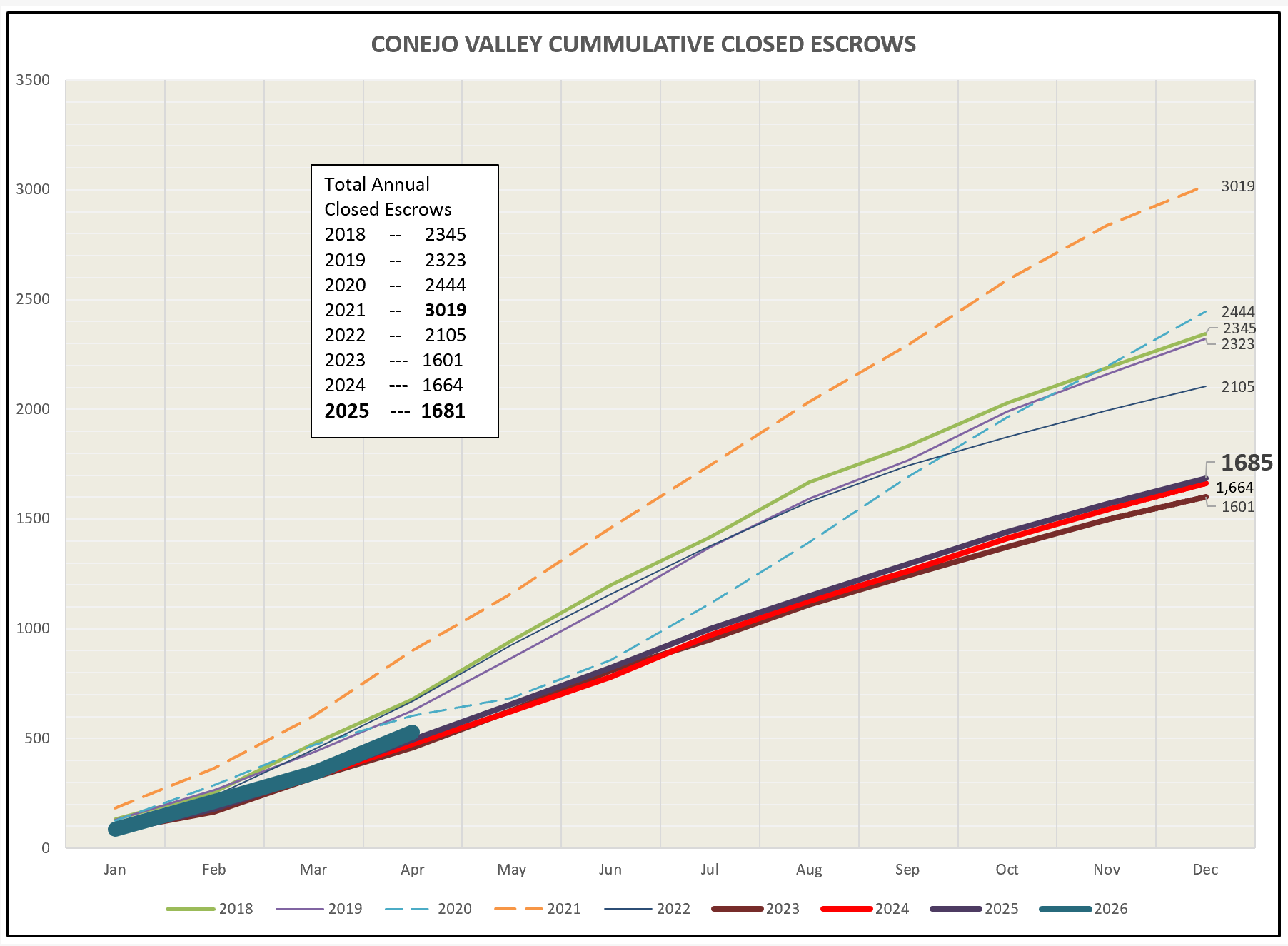

Looking at the progession of sales over time, Conejo is on a stronger path compared to the past three years. For the year, sales are up.

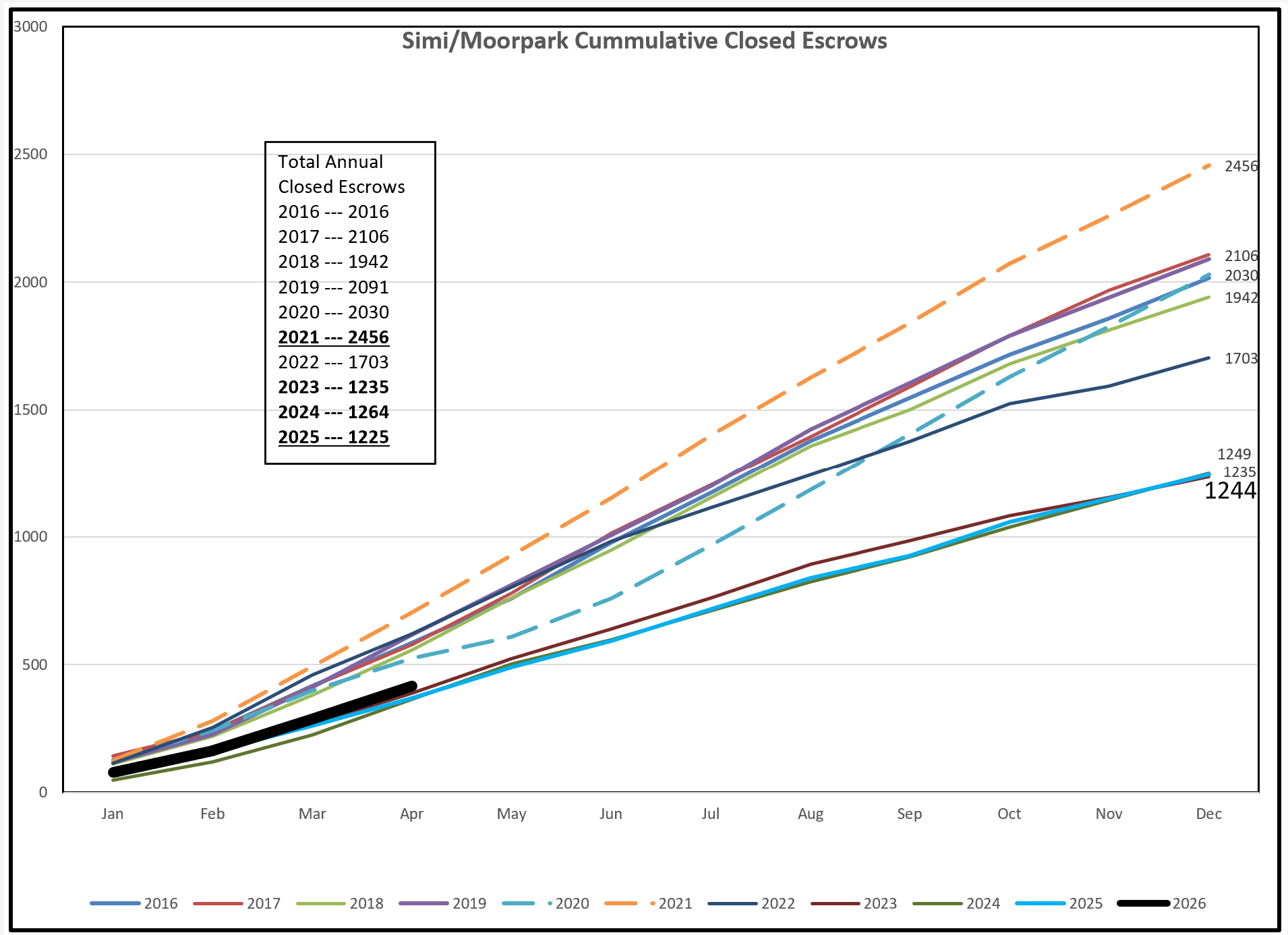

Simi/Moorpark also is showing improvement compared to the past three years as the seasons change.

Finally, prices in Conejo continue to follow the cyclical price growth experienced in past years as we approach summer. However, year to year prices have not been climbing and have reached a plateau. Prices today are similar to 2022, and lower than 2025. Over the long term, price growth is similar to overall inflation.

Simi/Moorpark has always exhibited a different result from year to year. The lastest results indicate similar price growth as Conejo. Average prices grew significantly to start the year, but are now pulling back, and much of this change is due to the blend of different price categories. Simi/Moorpark experienced strong growth in the higher price categories at the beginning of this year, whereas Conejo highest price home sales were decreasing.

Are we in a buyers or seller’s market yet?

You could say that Conejo is leaning buyer, whereas Simi/Moorpark is leaning seller. For Conejo, the highest price traunche of homes represent 1/3 of the active inventory and are moving slower compared to last year. Highest price homes are purchased not so much due to supply/demand pricing as they are as an investment compared to other investments available to people with wealth. These homes are not as much influenced by the real estate market itself as they are by other markets.

However, Simi/Moorpark is more of a stand-alone real estate market, more dependent on supply and demand for homes. Sales growth is agressive, prices are srtable and being negotiated,

Looking forward to what next month tells us. It would be nice to settle wars and get on to normal times.

Stay safe out there.

Chuck