A picture is worth a thousand words. But sometimes pictures need some additional words to better understand what is happening.

PRICE

Pricing will be THE hot topic in the coming year. Prices will show a decline. But how much of a decline needs further investigation and explanation. This will probably need more than one reading to understand my message. It may at first be confusing.

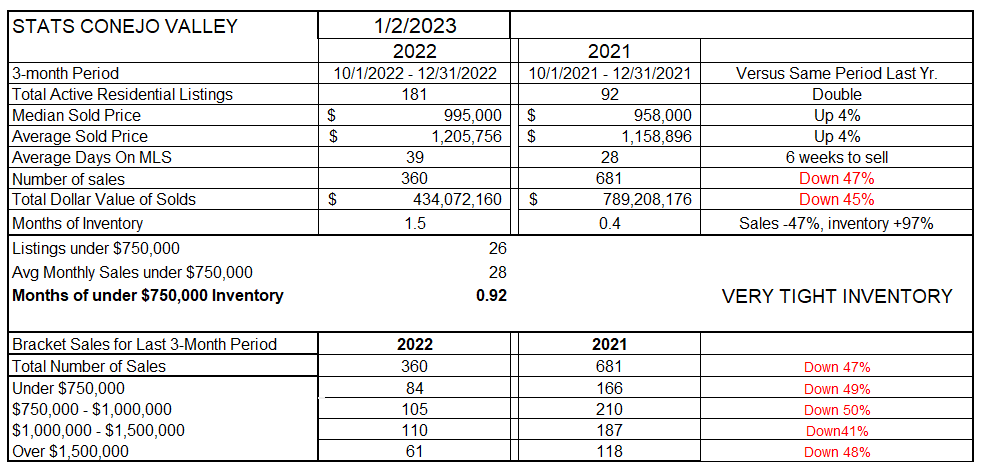

Let’s start with the statistics table to show you what I mean. For the year, prices are up 4%. More fully explained, prices for the last three months of 2022 are up 4% over the same three months in 2021. (The 3-month average in this table tends to smooth out changes). All this while the number of sales in those periods is down 47% and active inventory doubled. Something seems out of whack. Logically, prices should be going down, not up. In reality, prices have been decreasing, but not according to the year-to-year comparison used in this table.

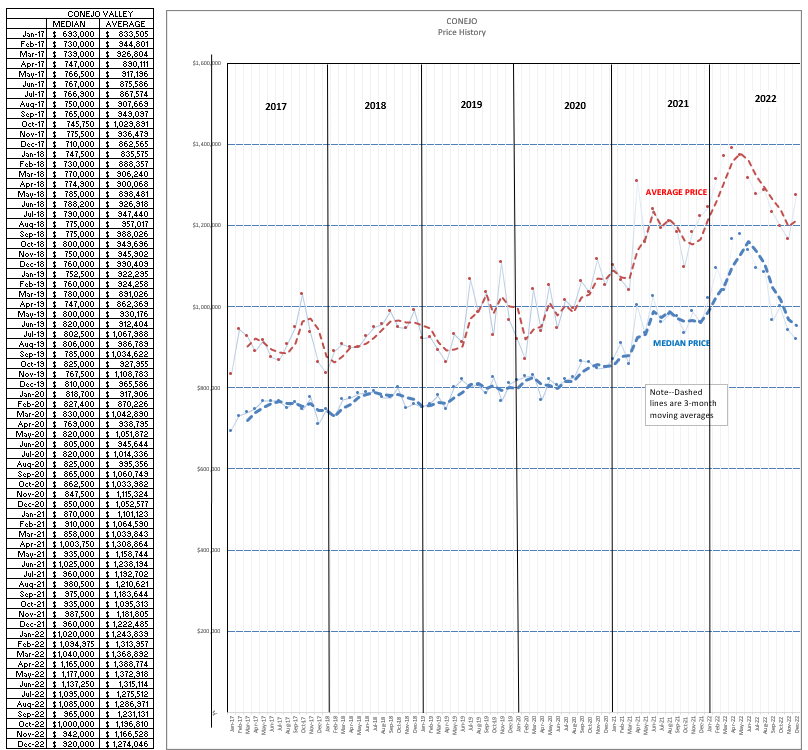

Let’s see how prices have been doing by analyzing the pricing graph below. In particular, look at the pricing curve for 2022. We ended this year at pretty much the same price we began the year at, although prices peaked mid-year. According to the monthly numbers in the chart below, we could say prices actually declined year to year. Compare the Median December 2021 price ($1,020,000) to the Median December 2022 price ($920,000), down 10%, not up 4%, as shown in the table. The table above utilizes a 3-month average figure, while with the chart below we can compare a single month versus the same individual month last year. It all depends on which numbers you use.

Which one is right? They are both right. Statistics lets you choose how you look at the numbers. (I remember a book titled “How to Lie with Statistics”). People often choose the numbers that support the story they want to tell.

We need to look into how prices reacted while 2022 was progressing. If all we do is compare December2021 to December 2022, we do not really see what is happening. This will be important to remember as this 2023 year progresses.

I predict 2023 will start off showing prices declining compared to 2022. That is because in early 2022 monthly prices were increasing, while prices currently are not. A year-to-year comparison will look as if prices are falling dramatically, a decline much worse than reality. This overview needs to be kept in mind as we move forward. According to the statistics table, prices appear to be up 4% when comparing December 2021 to December 2022.

However, if you compare the highest price recorded in 2022 to the price at the end of the year, you could argue that prices have already declined by 10%.

Confused? It all depends on which numbers you use.

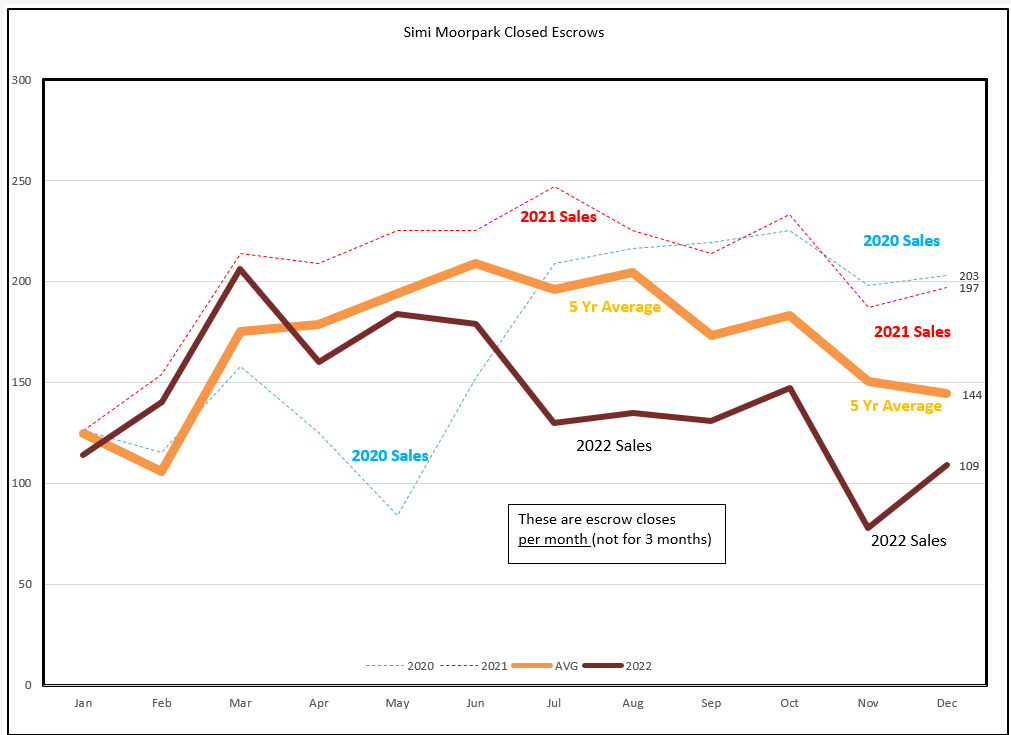

Let’s look at the same information for Simi Valley and Moorpark.

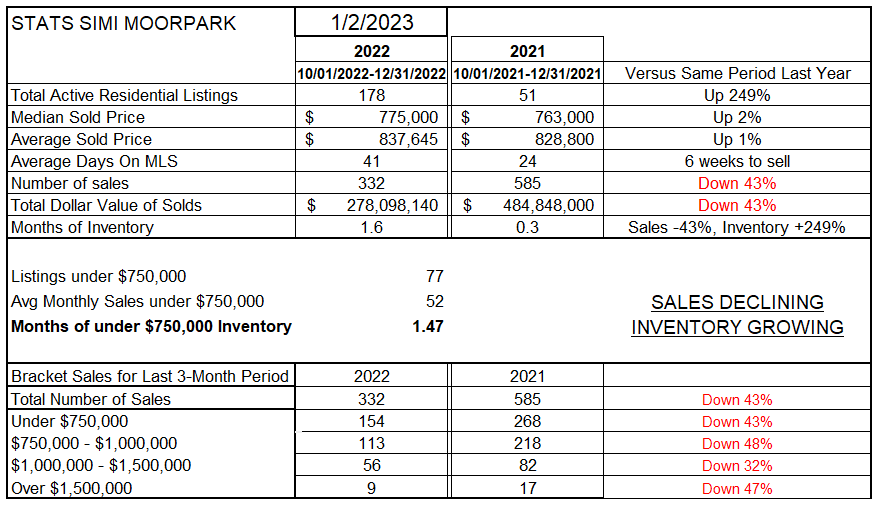

For the year, the table shows prices up 1-2%. More accurately, prices for the last three months of 2022 are up 1-2% over the same three months in 2021. (The 3-month average in this table tends to smooth out changes). All this while the number of sales in those periods is down 43% and active inventory has increased an enormous 249%. The numbers don’t jive. Prices should logically have fallen. Right?

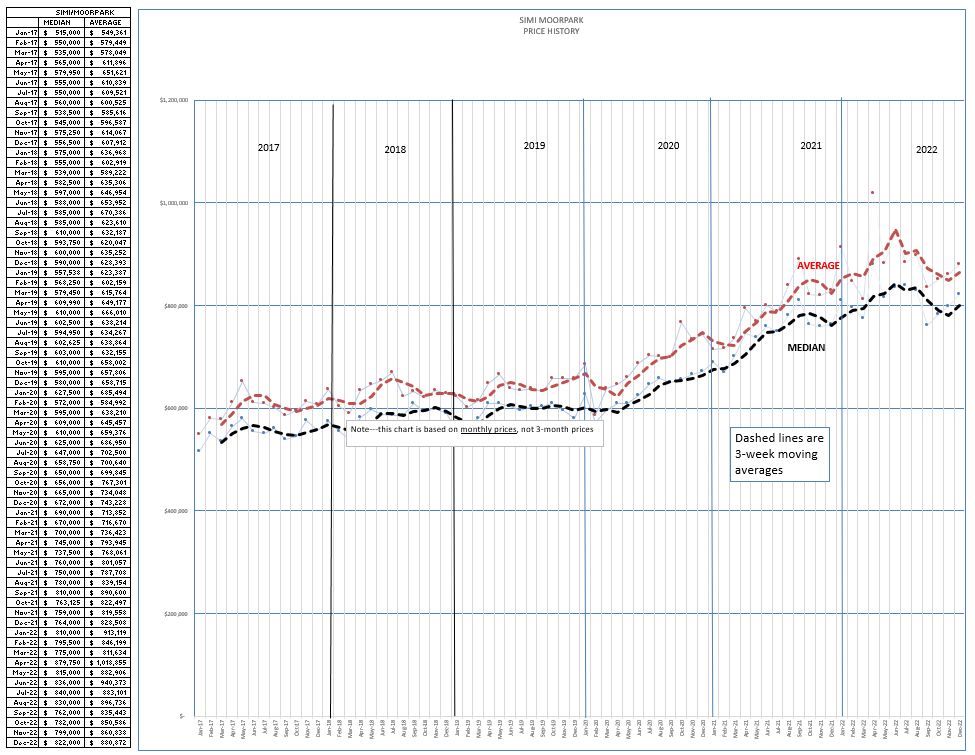

Now let’s view how Simi/Moorpark prices have been doing by looking at the pricing graph below. In particular, look at how pricing changed during 2022. We ended the year a little higher than we began the year. According to this chart, prices rose in the first half of the year and declined in the latter half of the year. However, if we compare the Median December 2021 price of $810,000 to the Median December 2022 price of $822,000, we can say prices increased 1.4%, similar to the numbers in the table.

We need to look at how prices were reacting while 2022 was progressing. The beginning of the year saw prices increase about 5% until May 2022, then began falling back 5% by the end of the year. For 2022, prices at the end of the year were very near prices when the year began. It could lead you to say prices did not rise at all. But they did, especially prior to mid-year. Then they declined.

The pricing peak coincides with the FED rate increases. Although the FED often changes only one rate, the overnight borrowing rate, all rates are eventually affected, including mortgage rates. If all we do is compare December2021 to December 2022, we do not really see what is happening, and what is about to happen. This will be important to understand as this 2023 year progresses. 2023 will probably start off showing year-to-year price declines. Even if 2023 prices remain constant, it will look as if 2023 prices are dropping, because 2022 prices will be rising.

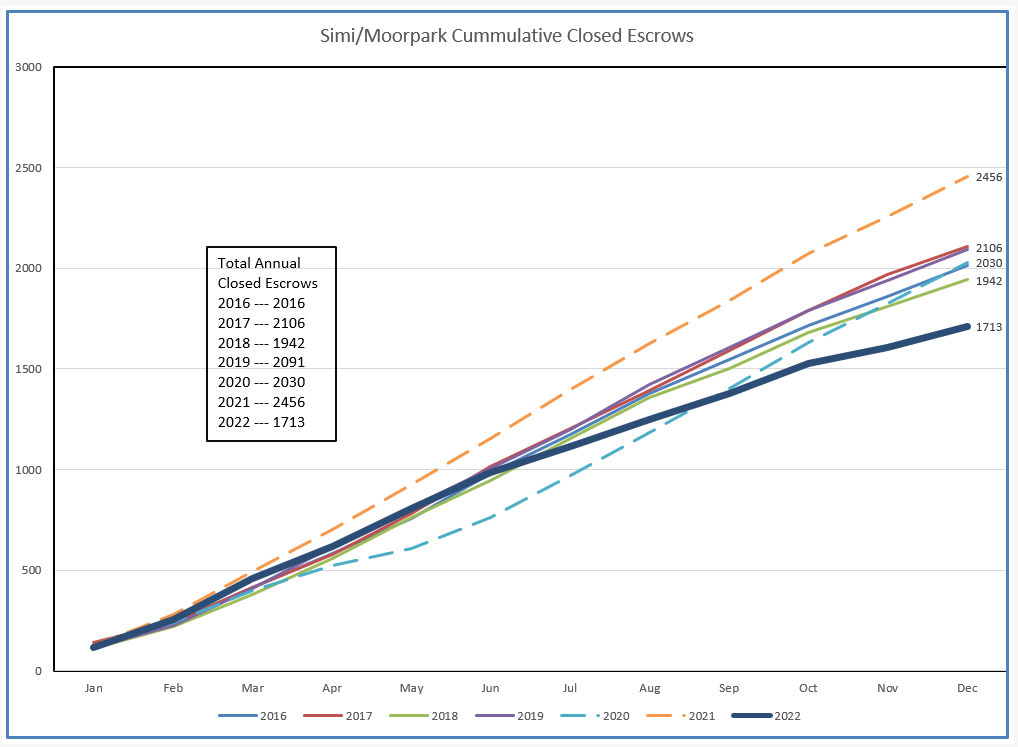

Next, lets look at how the year can be described using the Closed Escrows chart. The dotted lines represent monthly closes for 2020 and 2021. These were anomalies, heavily influenced by and an unexpected benefit of Covid —– the move to the suburbs and working from home. The plot for 2022 more closely follows our historical average graph while reflecting the lower number of closed escrows. A more normal curve.

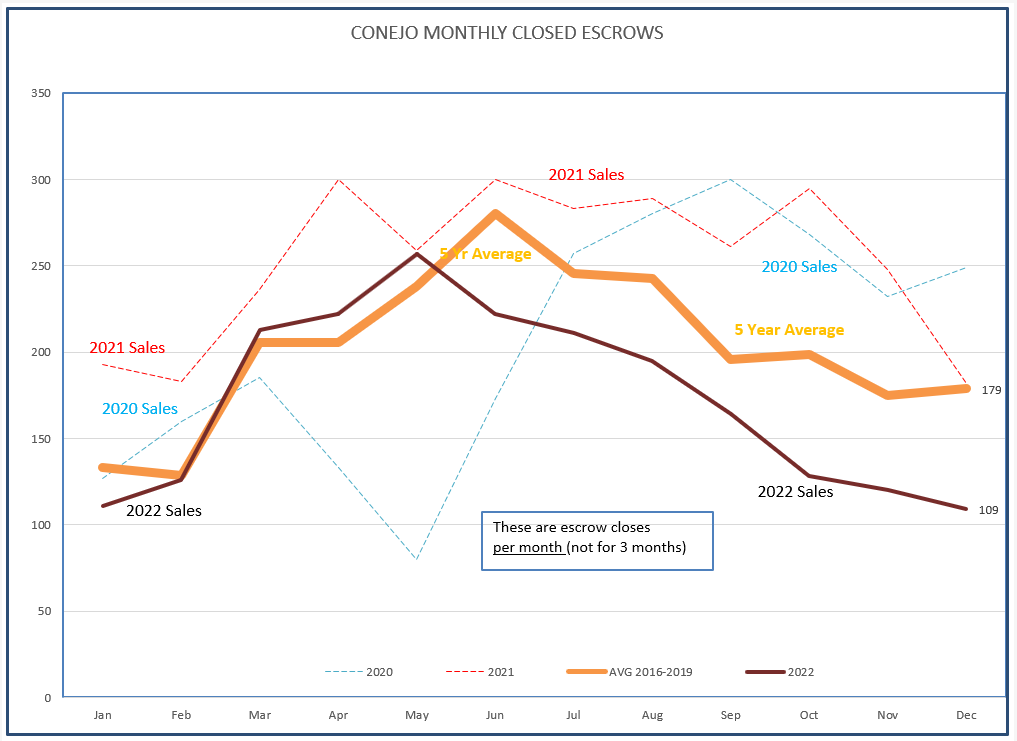

The experience in Conejo was similar. Both graphs seem to follow the historical average plot, although at a lower level, because of fewer closings. Quoting the statistics tables, a 43-45% lower level.

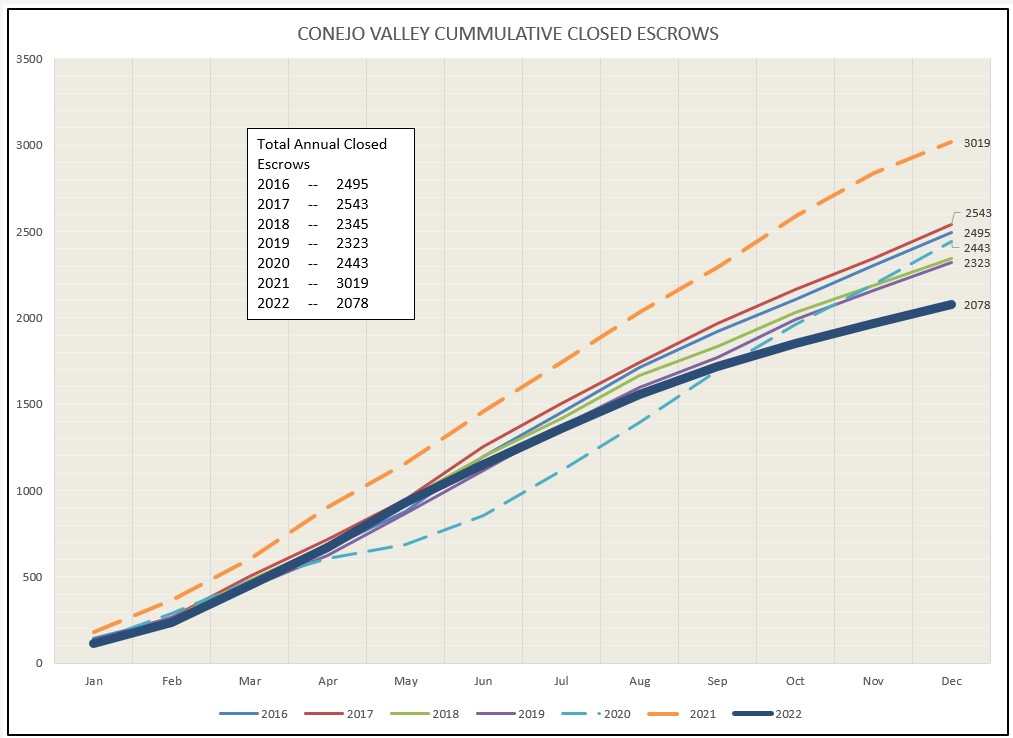

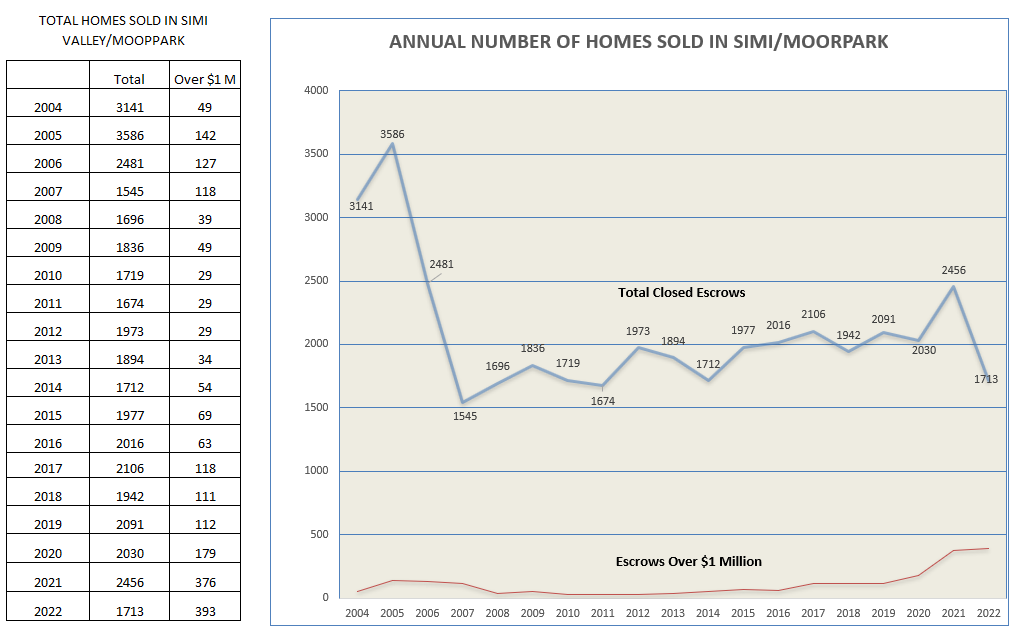

Looking at the same information in a different way, the charts below represent how the total number of closed escrows changed as the years progressed. In 2022, the number of closed escrows was proceeding as expected until May, but ended the year registering the lowest number of closes in the past 10 years.

The chart above shows the statistics for the past 7 years, as each year progressed.

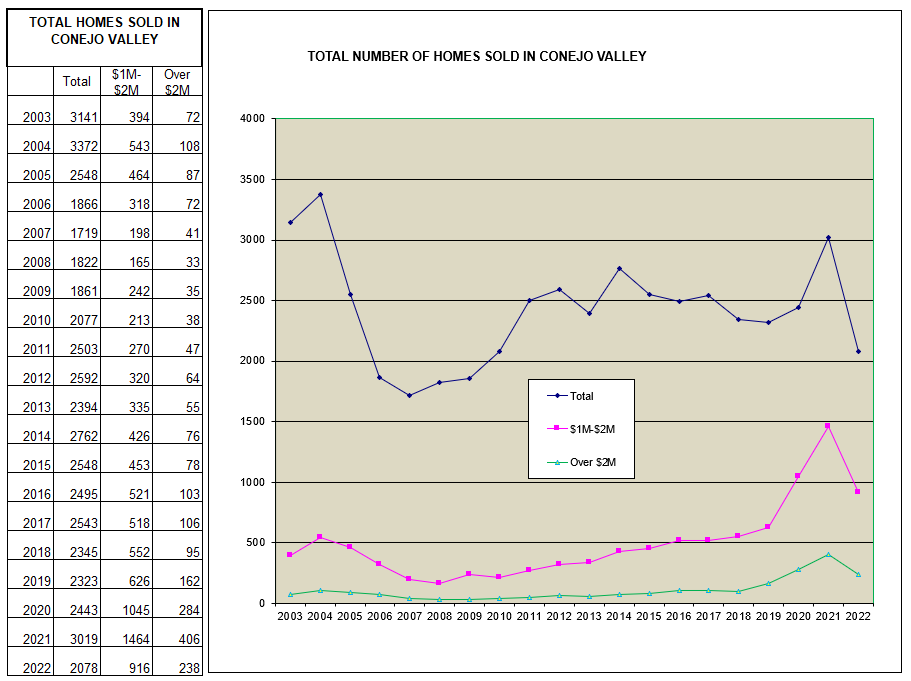

This chart below shows the total number of closed escrows for each of the years. Interesting to point out that the number of homes sold in 2021 was the third highest number of closed escrows this century. Conejo was also highly influenced by the number of very-high-priced homes.

Simi/Moorpark shows the same change in direction beginning in May 2022.

For Simi/Moorpark, the number of homes sold in 2021 was not near the highest number of closed escrows this century. The high point for 2021 was much lower than the record set in 2005. While Conejo was highly influenced by the number of very-high-priced homes, Simi/Moorpark was likely influenced by the increasing number of new homes built. Those homes are not included in these graphics, at least not until they are re-sold.

While I provide these figures and analysis for you to share with your buyers and sellers, it is important to point out one change in the market that is very personal to agents. Home owners may see their homes decline in value for a period of time, but when the market resumes its usual climb, that value will be retrieved.

Real estate agents and brokers are going to be affected both by the volume of homes sold and by the decrease in prices, as both directly influence total commissions. As the market price corrects and sales volume goes down, total commissions will go down by those combined factors. Our real estate business was very profitable during Covid, but the coming year will produce fewer and lower commissions than those Covid years. Like every business in the forecasted recession, our business will be more challenging. You can still do well, but you will have to work harder and smarter. You will need more transactions.

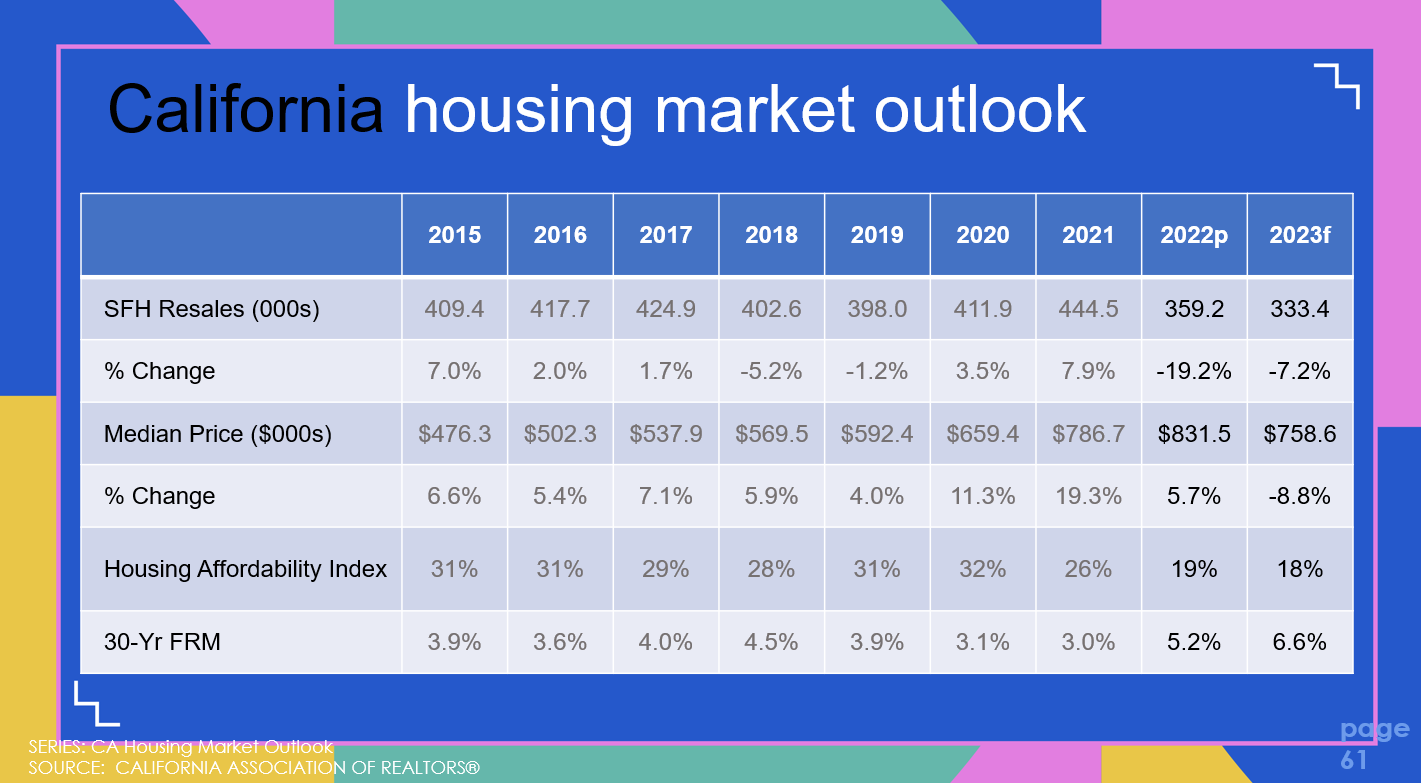

Let’s look at what C.A.R. is forecasting.

For the State of California, the number of Single Family Home resales in 2021 was 444,000. The number forecasted for 2023 is only 333,000, a two-year drop of 25%. In addition, prices are forecast to recede by 8.8%.

One last thing I want to discuss for this year-end report is mortgage rates. I have spoken often about the FED and increasing rates. But there is good news here.

First, inflation appears to be coming under control, and the FED may not have to act so severely. Hopefully the end is in sight.

A second factor. When the FED raises rates, do mortgage rates go up in lockstep?

As the FED was increasing rates 0.75 points four times (April – October) and another 0.5 point in December, the expectation was that mortgage rates would also increase causing affordability to decline. That happened. However, the past few months of 2022 saw some stability in mortgage rates, and then an actual decline even while the FED continued to raise rates.

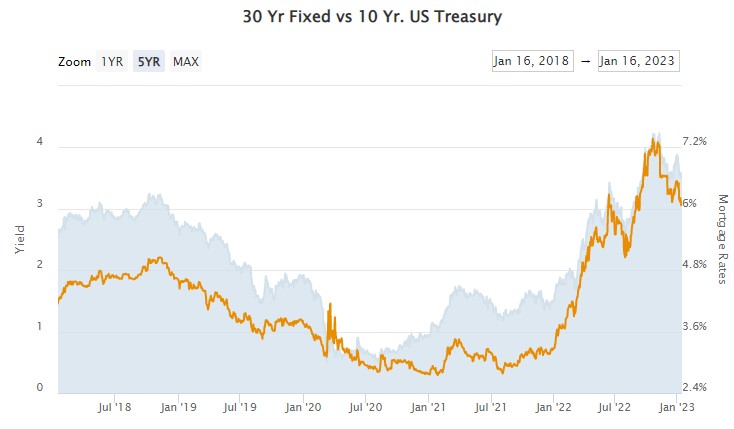

The FED makes rate decisions on very short term rates, actually overnight rates. This also affects other rates, but the longer the term, the less influence short term rates have. Many are forecasting that rates will decline in 2024, if not earlier, by the end of 2023. That expectation in the money marketplace has lessened the effect of these FED rate increases on longer term rates.

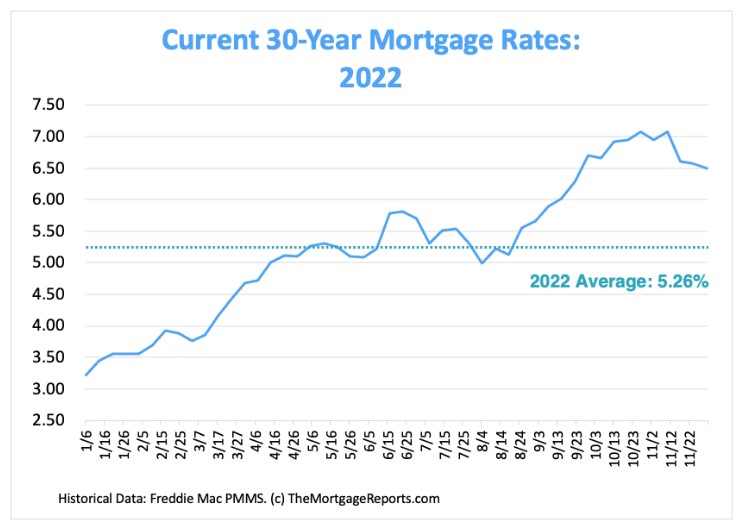

Historically, mortgage rates more closely follow the 10-year Treasury Bill, not the overnight FED rate. In the final months of 2022, the 10 year treasury rate has declined even as the FED continues to raise rates by 0.5% in December. Mortgage rates also declined, from over 7% to currently around 6 %. That decline will begin to create more affordability in home buying. And buyers are now using points to lower mortgage rates to more reasonable levels. There are a lot of buyers who want to be creative, who want to buy a home. Your job is to help them.

Looking at the mortgage rate history in 2022, it is easier to see the decline in rates as the year ended.

I do not see 2023 becoming a banner year for real estate, not another 2020-2021. Home prices will settle as we transition from a sellers market to a more balanced market. A buyers market would be evidenced by high listing inventory, and that is not taking place. We are moving to balanced.

Prices grew too quickly as both sellers and buyers bought into overbidding as the new normal. The market is moving back to balance with negotiation on both sides. The continuing shortage of housing, combined with the law of supply and demand, will keep prices from freefall. In 2023, homes will likely sell for a little lower price than last year, and fewer homes will be sold. I think the C.A.R. market forecast will prove to be accurate. A year of adjustment.

As the market adjusts, you have to adjust how you do your business. It is your job to help your clients understand the market, to help them maneuver through the minefield of bad news and scary percentages that the news loves to publish. Open Houses are back in vogue. We can door-knock again, we can walk our farms. Negotiation is becoming common, as it should be. Home values are determined by an agreement between a willing buyer and a willing seller, with pricing finding a middle ground acceptable to both. We are working in a balanced market.

Stay safe and have a prosperous new year. Both require planning and execution. Plan your work and work your plan.

Chuck