As the Government Affairs Director for Conejo Simi Moorpark Association, I often think of how politics might affect the market.

Buying a home and committing to a 30-year payment plan requires a thoughtful, well-informed decision.

There are numerous factors to consider, some of which are personal, and some of which involve how the potential homeowner and borrower views the stability and the future expectation of the economy.

Sometimes people ask “What is keeping you up at night?” I suggest to you that the current situation is less than stable, and the future at this point uncertain. Most people do not have a positive feeling about the future.

These are a just few of the factors occurring in today’s news:

The Middle East War. The War in Ukraine. Epstein Files. Uptick in Terrorism. ICE deportations. Threats to Democracy. Rising of Authoritarianism. Missing Economic Data. The Upcoming Election Inflation rising. Job creation flatlining. Unemployment rising. Interest Rates increasing. Tariffs. National Debt climbing. Leadership change at the FED. Straits of Hormuz Oil Prices rising. Gas prices rising. US Marines on the move . Homebuyers Cancelling Sales Contracts At The Highest Rate Ever.

Is that enought to worry about? Maybe I should stop watching the Sunday morning TV shows. But I am not the only one watching the news.

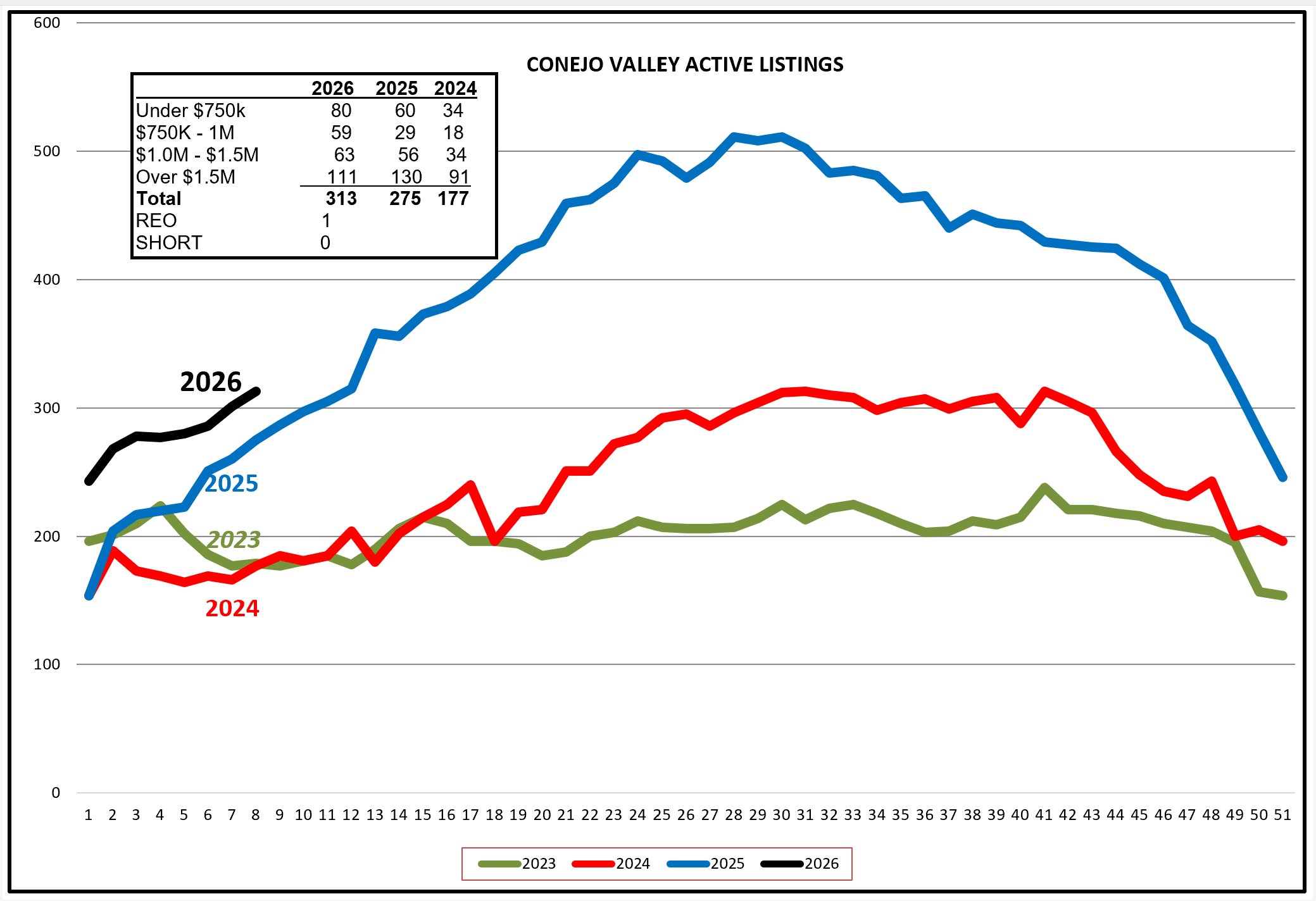

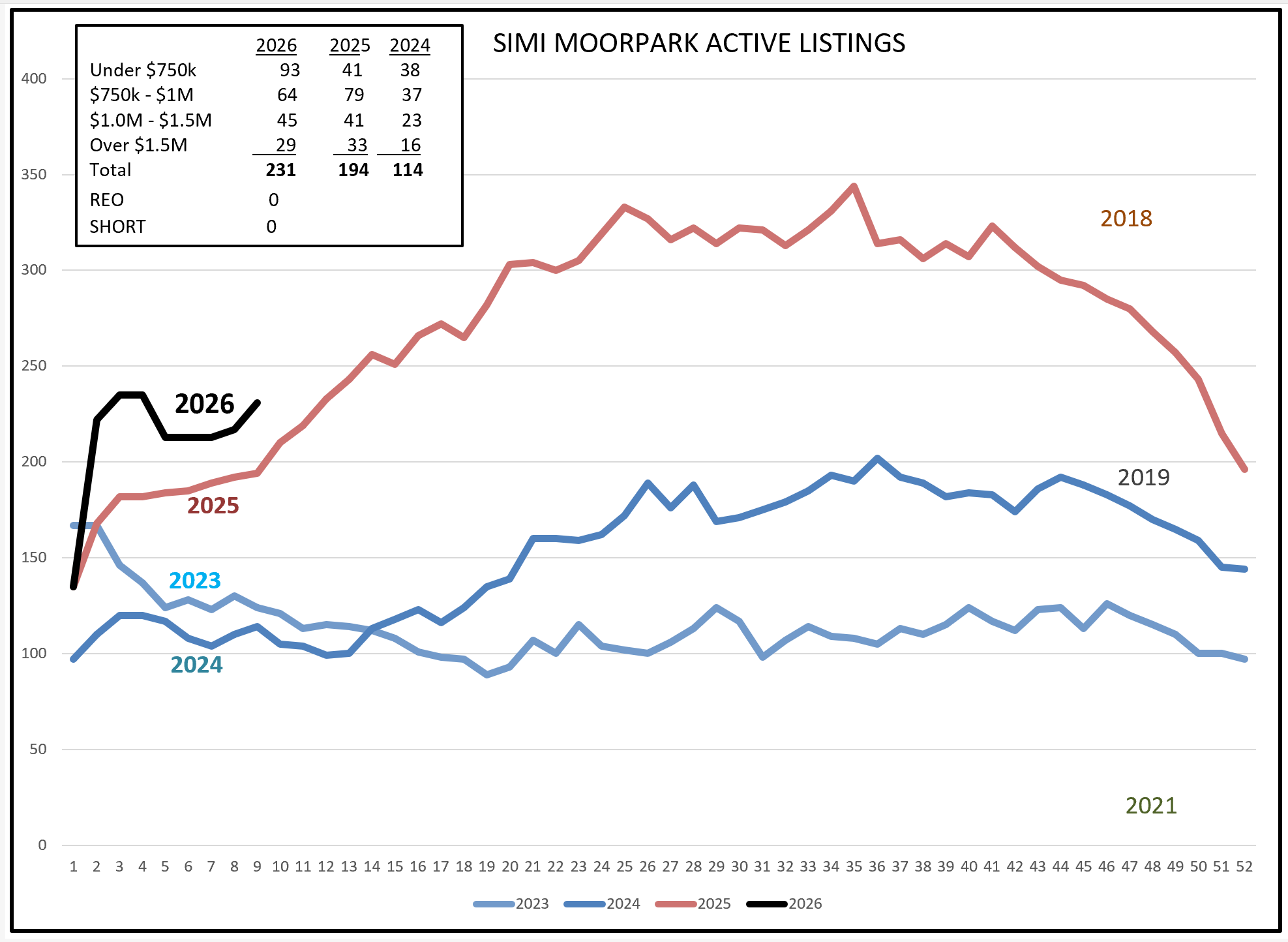

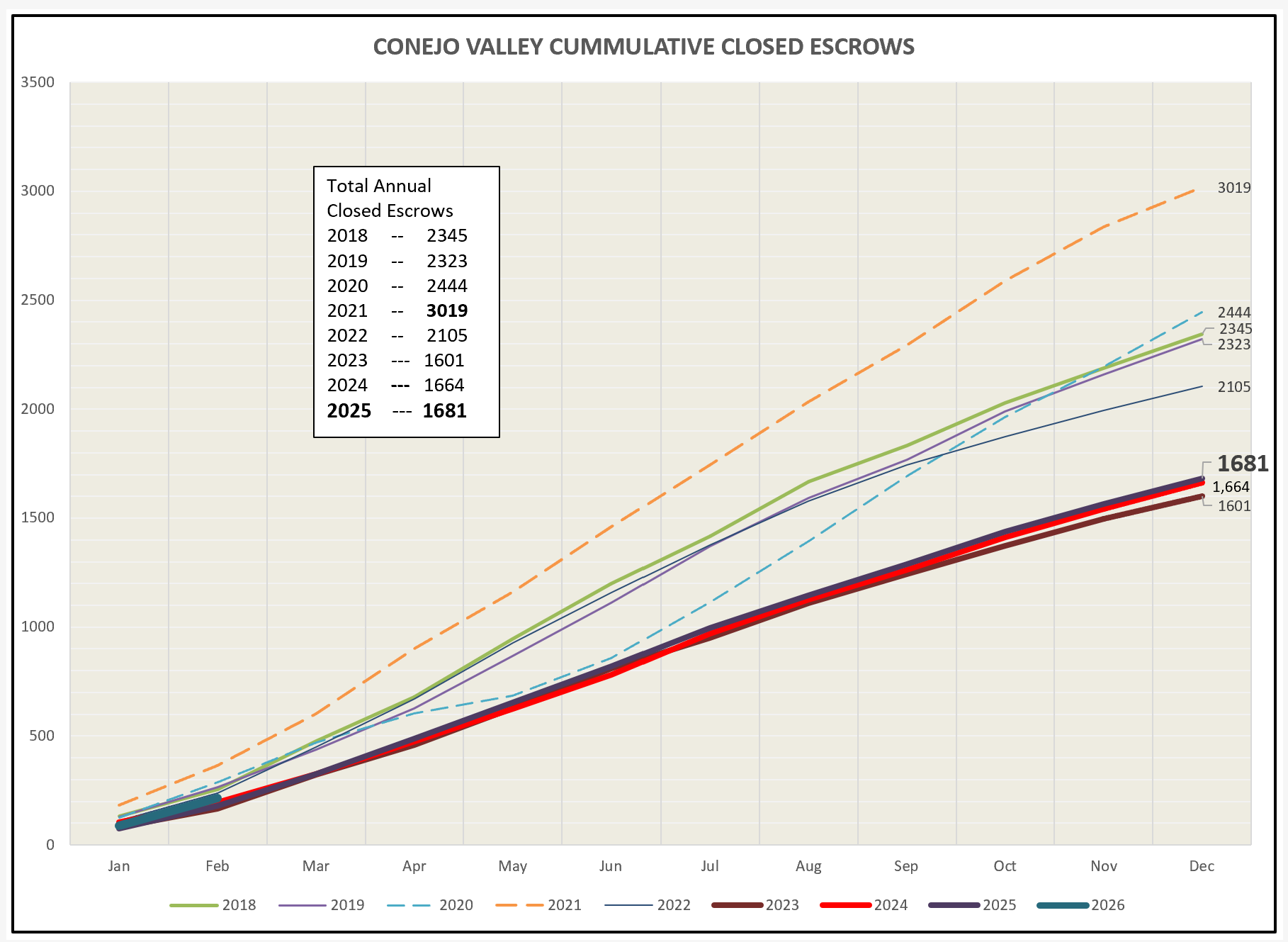

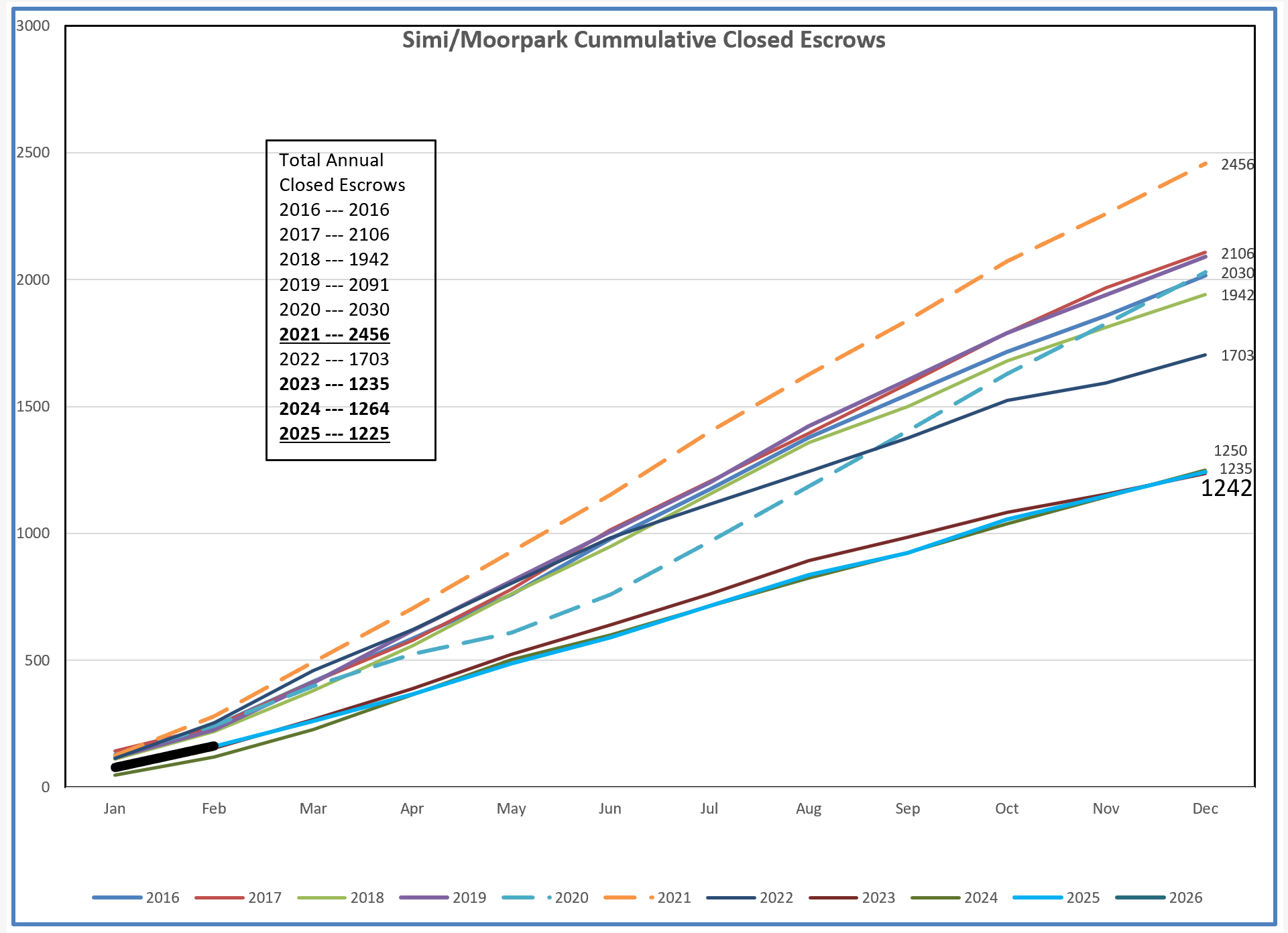

Given that list of worries, let’s look at how our market has begun the new year. I have made these charts more current, going back only 4 years for history. I have data going back to 2005, but that includes a major Recession and Covid. Maybe its time to only look at recent history.

First let’s see how inventory is doing, how many homes are listed and available. Listings are growing. We dealt with a shortage of available inventory particularly during the Covid years. In the Conejo Valley, last year was more like normal, and this year inventory is starting out the same.

For Simi Valley/Moorpark, the same is true. In the Covid years, inventory was as low as 100, and sales were impacted. We now have a decent amount of listing inventory.

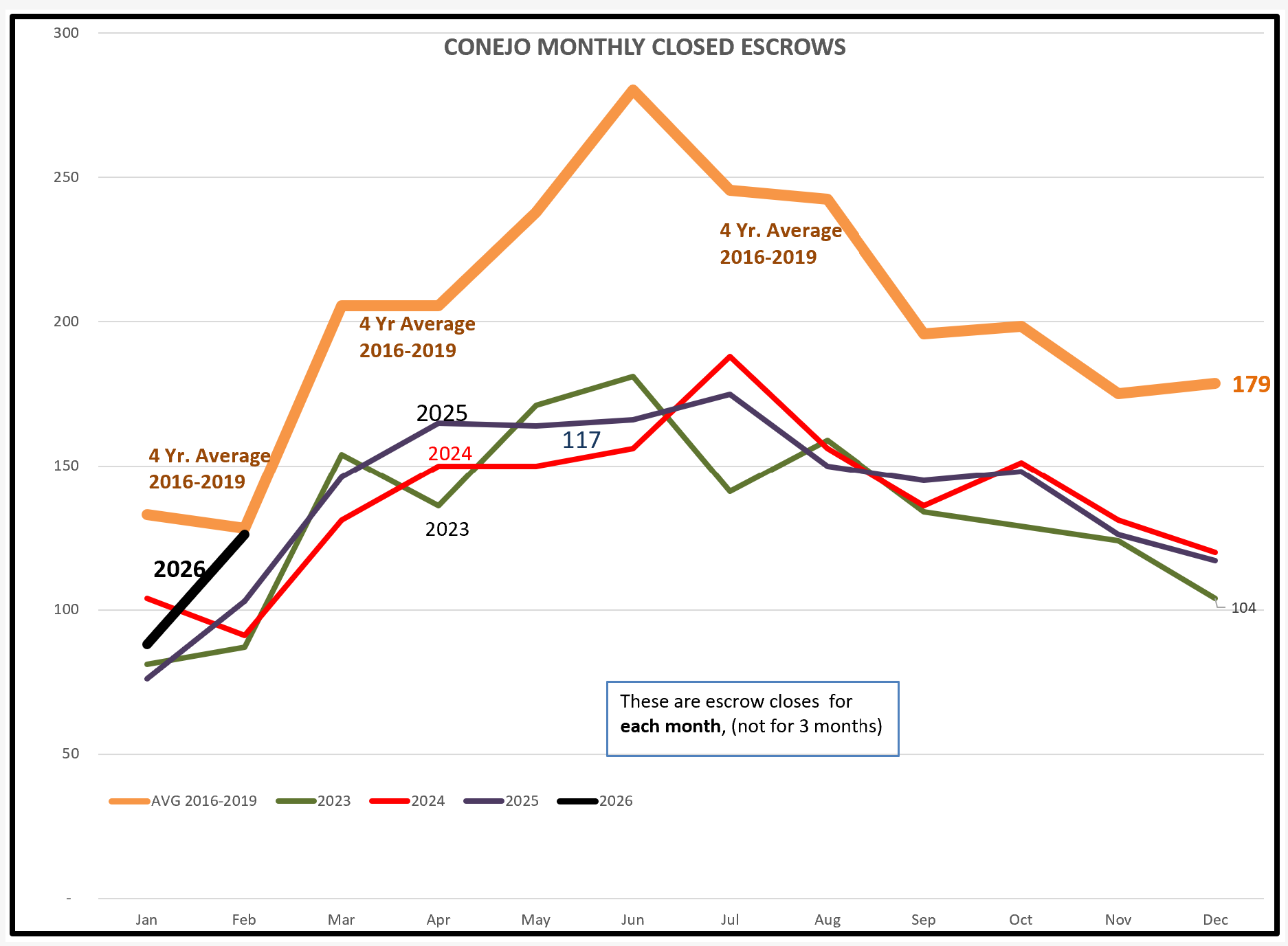

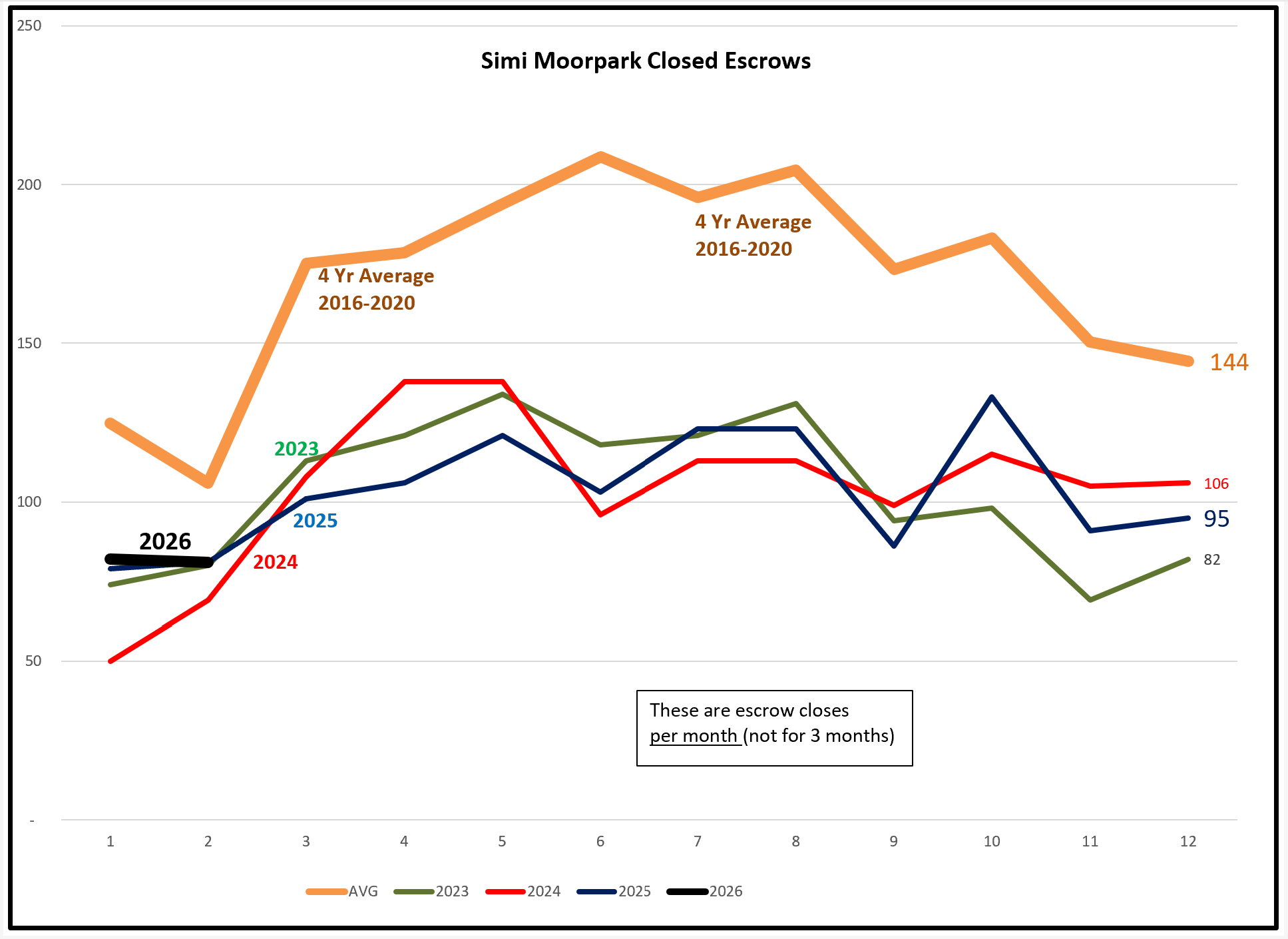

Inventory growing can be good, or can indicate a concern. If inventory grows but sales does not respond by buying up the inventory, we can expect the inventory to grow too much and the price/demand balance then begins to favor buyers and weakening prices. The Closed Escrow charts below include pre-Covid 4-Year Averages to compare against the current level of sales.

For Conejo, sales are starting out comparable to the past three years. We hope this foretells a strong market, but it is too early to tell. 2023 , 2024 , and 2025 compared closely to one another. Next month we will get a better read on how 2026 compares. A sneak peak into the future tells me we are still following the levels of those three years.

For Simi/Moorpark, following the sales levels of the past three years looks consistent.

Maybe the cummulative charts will prove more enlightening. Conejo shows a little improvement, but nothing indicates it will be a year to brag about. More like the past few years.

Simi/Moorpark shows us right on the path of the past couple of years. Unfortunately, the past few years are all quite similar, on the low side.

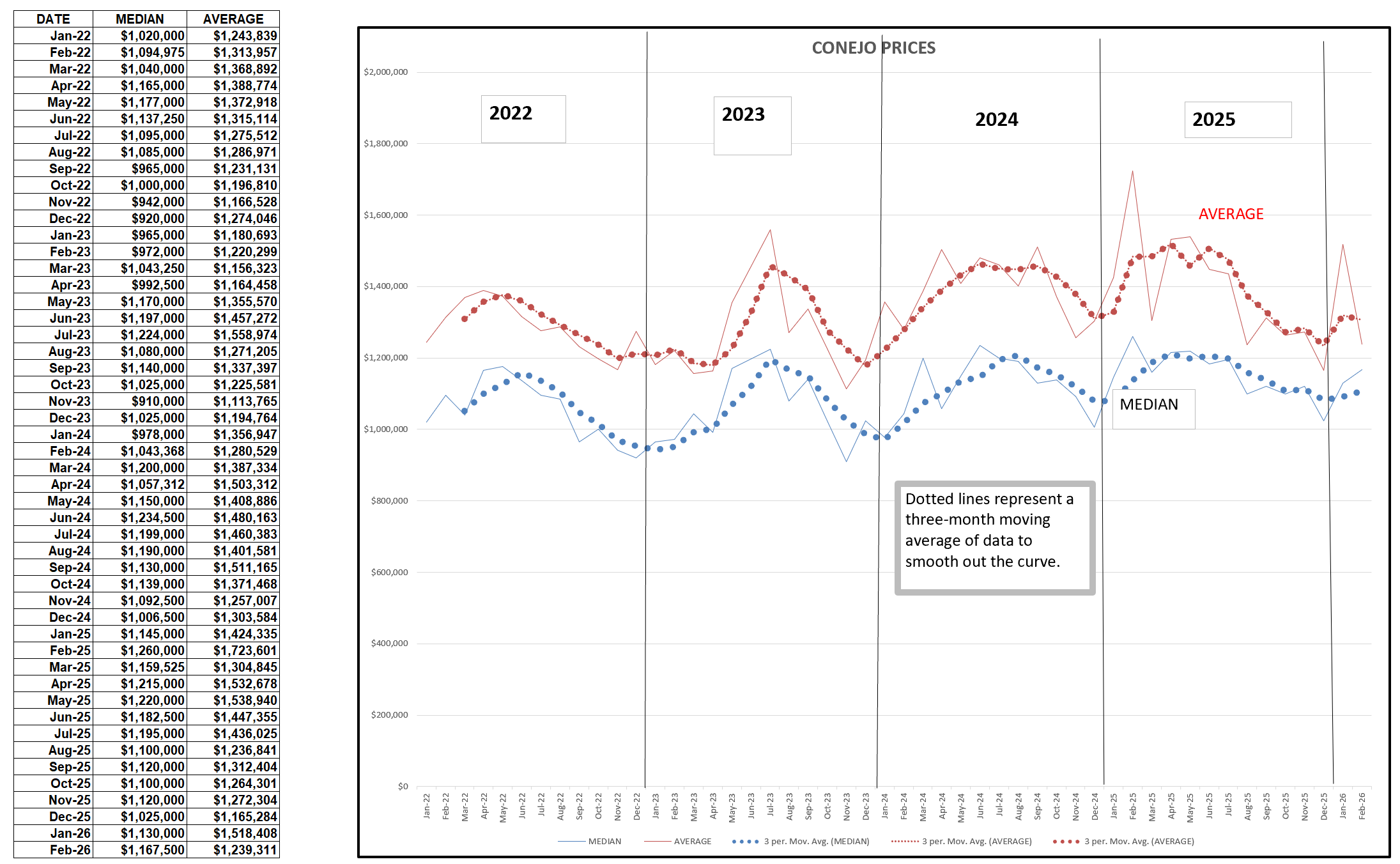

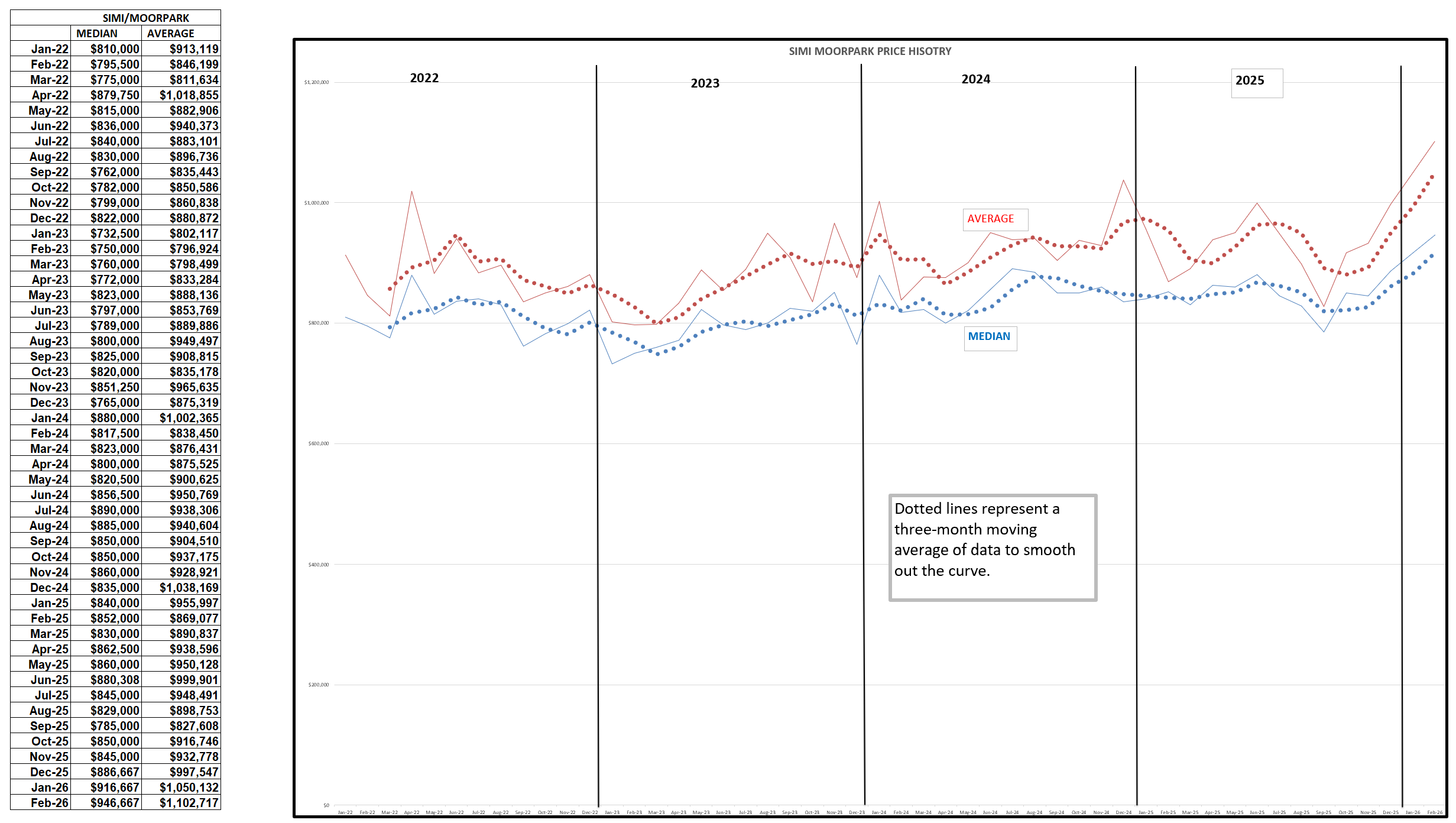

The third part of the supply/demand equation is pricing. Agaim. the charts below are a little more condensed, not going back as many years. The information is still available should you need it, but I feel this gives us a better understanding of what prices have been doing.

Conejo prices can vary month to month, so while the chart below shows those ups and downs, the heavy dotted line is smoothed out by taking 3-month rolling averages. This chart displays the tendancey of prices to follow the same sdeasonal curve as inventory and sales, with both Median and Average prices rising approaching summer and falling toward winter. Perhaps most interesting is to compare the average price at the beginning of 2022 ($1,243,839) to the average price today ($1,387,334), a total increase over four years of about 10%. Prices over that term were rising on average between 2 and 2.5 percent per year. This is a lot lower than most of us thought.

For Simi/Moorpark, the ups and downs are not as regular, and the recent history shows a very large increase in both Median and Average prices. Once interest rates declined to the 6% level, Simi Moorpark prices were much more affordable, and attracted more buying interest. And while sales of the highest end properties have scaled back in Conejo, for Simi/Moorpark their highest end properties have become much more attractive. Truly a tale of two cities, or in this case areas, Conejo somewhat subdued compared to Simi/Moorpark, where prices are strongly on the rise.

So how will 2026 shake out? I refer you to the beginning of this report and the plethora of factors that are causing uncertainty. Without some confidence in the future, sellers will be hesitant to move and buyers will be hesitant to buy. There are always some sellers that have pressure on them, divorces, job moves, loss of jobs, loss of a loved one. But the lower level of sales is missing that group of homeowners who look to take their equity and buy a larger and more expensive home.

With inventory climbing while sales are similar to last year, I look for prices staying stable to weak. There will still be buyers and sellers. But there is a large segment of potential buyers and sellers that have choices based on their feeling about the future, that do not have the pressures of life to make a move. They will be waiting for a calmer time. This year looks to be a lot like last year.

Even if those buyers and sellers are hesitant, they still need a trusted advisor to keep them informed about the market, about their home value and the price of homes in their areas of interest. And mortgage rates. We don’t put up signs like gas stations, but you can be a source of information on mortgage rates by quoting your preferred vendors. Your clients need you to consistently send them informtion.

Stay safe out there. And keep making those contacts, those touches, keeping your clients in the know, ready to help them when they are ready.

Chuck